by Tom Warburton, Russell Investments

Key takeaways

- Tariff uncertainty is driving defensive equity shifts

- AI outlooks are evolving amid increased competition

- China sentiment is improving

- U.S. M&A activity has stalled

5 Key Macro Trends

1. Tariffs are driving equity managers’ defensive posture

After entering the year with a cautious outlook, managers have become more defensively postured as the U.S. tariff policy has increased uncertainty. Global managers have been reducing exposure to the U.S. and rotating toward emerging markets. Within the U.S., equity investors are focusing on companies with stable business models and limited exposure to international trade. Managers observe that many companies are delaying spending and investing decisions until there is greater clarity regarding U.S. tariffs.

Outside the U.S., managers in other developed markets are looking to own more domestically focused companies. Most notably, equity investors in Europe and Japan have cited a favorable opportunity for domestic demand-oriented stocks.

2. The AI outlook is shifting

DeepSeek’s announcement of its open-source, lower-cost AI alternative also caused a significant shift in managers’ outlooks. Investors became more cautious regarding their longer-term expectations for Nvidia as the leader in AI semiconductors. Competition has also increased cost pressure among hyperscalers. Investors have increased conviction on the resilience of global foundry leaders that can weather the impacts through better economies of scale.

Investors continue to view AI as a long-term secular growth opportunity, but are shifting their focus to software companies and other downstream applications that will benefit from AI.

3. China sentiment is improving

Several positive trends are developing within China. In addition to the DeepSeek launch underscoring increased competitiveness in AI, a more constructive stance around technology is emerging from the Chinese government.

Managers remain constructive on the Chinese consumer, noting that previous stimulus measures are beginning to take effect and improving the outlook for consumer companies. The improving environment for both the consumer and technology sectors is also reviving interest in China’s EV market, with investors becoming increasingly bullish on Chinese EV manufacturers.

4. U.S. financial regulation has fueled uncertainty

The outlook for a widely anticipated M&A boom in the U.S. has faded before it got started, as credit spreads have widened around economic uncertainty. This has delayed an expected rally in small caps, which benefit from M&A activity. Investors are also reducing exposure to private equity firms and investment banks.

5. Global economic trends are favoring gold miners and copper

In resource-rich markets—including Australia, Canada and South Africa—gold miners were key beneficiaries of increasing inflation concerns and the supportive price environment. Managers continue to be bullish in the near-term as fears of a global slowdown have risen.

In a continuing theme, investors remain optimistic about copper in the long-term, as supply is expected to lag demand for multiple years.

Global Equities

Investors seek to navigate tariff disruption

- Growth managers are reducing exposure to U.S. consumer discretionary companies that depend on global supply chains.

- Given the slide in U.S. dollar strength, some managers have rotated into emerging markets, including domestic Asian and Latin American banks.

Defensive track to help temper cost pressures

- Risks of profit contraction saw some value investors shift toward undervalued, durable companies. These include staples and pharmaceuticals that are relatively resilient with healthy balance sheets and stable growth.

- Both global value and growth managers have increased energy exposure to reduce inflationary tail risks.

DeepSeek raises eyebrows over AI compute spend

- Investors were caught off-guard by DeepSeek’s trained, low-cost alternative as an AI engine. This has resulted in a re-evaluation of chip exposure, since better AI accessibility has led to an increased focus on software and downstream applications being among the next wave of beneficiaries.

- Competition has also pushed up cost pressures among hardware hyperscalers. Investors are doubling down on the resilience of global foundry leaders that can weather the impacts through better economies of scale.

Japanese banks on the cusp of a positive earnings cycle

- In the wake of increasingly persistent inflation, higher anticipated interest rates from the Bank of Japan (BOJ) are expected to boost net interest margins among local Japanese banks.

Cashing in on gold amid market uncertainty

- Real asset investors are taking profits on gold miners that rallied on the back of historic peak gold prices. Reallocations to other precious metals such as platinum and palladium serve as diversifiers and are expected to benefit from structural demand-supply tailwinds.

U.S. Equities

Reverse engines

- Relative to the pervasive bullishness at the start of the year, managers generally repositioned portfolios more defensively through the first quarter, as a pullback in mega cap tech stocks and uncertainty surrounding trade and monetary policies have muddled the outlook for growth and corporate earnings.

Trade policy uncertainty

- Last quarter, managers expected tariffs to be enacted on an industry-by-industry basis to promote reshoring of manufacturing within the U.S. Instead, the Trump administration’s across-the-board ‘reciprocal’ tariff policy and tit-for-tat trade war with China is now expected to upend supply chains, creating significant uncertainty for both corporate management and equity managers.

- With a wider range of potential outcomes in policy, managers are positioning portfolios more domestically and defensively, reducing cyclical exposure and adding to sectors unencumbered by tariffs.

Market uncertainty

- Government policy pronouncements are also creating uncertainty within financial markets, with higher interest rates and credit spreads, and a lack of consensus around margins and valuations undercutting a widely anticipated M&A boom before it started.

- Managers are reducing exposure to capital-markets holdings like private equity firms and investment banks previously expected to benefit—and to financials more broadly—as credit risk increases.

Another false dawn for small caps

- Small-cap stocks were expected to benefit from the reorientation of production domestically, lowered levels of regulation and increased M&A activity. With those trends in reverse, small cap stocks have again underperformed their large cap peers.

- While acknowledging the historical cheapness of small caps—both in absolute terms and relative to large caps—managers nonetheless do not expect small caps to outperform until there is more certainty on trade policy and the trajectory of interest rates.

Emerging Markets Equities

China: Positive sentiment despite tariff concerns

- Tech and innovation: A more constructive stance around technology is emerging from the Chinese government. The launch of DeepSeek underscored China’s competitiveness in the AI landscape and has reignited interest in the tech sector. Cheaper models could further lower costs and allow Chinese companies, particularly those closer to AI monetization—such as internet platforms—to benefit.

- Consumer rebound: Managers remain constructive on consumer stocks, noting that previous stimulus measures are beginning to filter through, as consumer confidence improves.

- EV sector interest: Positive momentum in the technology and consumer sectors has also sparked renewed interest in China’s EV market, with some managers increasingly viewing Chinese EV manufacturers as leaders in the industry.

Valuation opportunities in Brazil

- Brazil has faced significant capital outflows driven by fiscal spending, interest rate policy and political concerns. However, a combination of weak valuations and a potential change in leadership after the 2026 presidential election has renewed investor interest, although uncertainty around timing remains.

Early signs of easing inflation in India

- The continued underperformance of the Indian market, combined with positive economic signs such as moderating inflation, is starting to attract investors toward domestic opportunities—specifically within the financial sector.

South Africa continues to be a bright spot

- Managers maintain a positive outlook on South Africa, with investors believing the country could further benefit from a supportive gold and precious metals price environment.

Commodities: Positive views on copper and lithium

- Many investors remain positive on commodities—particularly copper and lithium due to their structural growth tailwinds, which are supported by anticipated supply-demand imbalances.

Long/Short Equity

Reduced gross and net exposure

- Global long-short ratios reached five-year lows, reflecting a strong preference for capital preservation and decreased cyclical exposure in consumer and software sectors.

Momentum exposure reduced

- Hedge funds significantly reduced exposure to high momentum stocks, marking the largest monthly reduction since 2010.

Selective Asian market adjustments

- Funds notably reduced exposure to Chinese technology stocks amid renewed regulatory and market volatility concerns, reversing prior bullish sentiment.

Europe and UK Equities

Improving cyclical picture and a German fiscal bazooka

- Cyclical indicators (PMI, loan growth and unemployment) are improving, and ongoing European Central Bank (ECB) rate cuts should provide further support for growth in Europe. Additionally, the recent German election yielded a positive surprise, as the new centrist coalition agreed on a relaxation of fiscal rules and on a major (EUR 500 billion) fiscal package. Managers expect that this environment will benefit cyclical industries (industrials, materials, banks and utilities, etc.), which remain very cheap relative to history.

Could small caps be the winners?

- Larger companies have been the primary winners from globalization. However, equity investors see a return to an era of higher trade barriers, or even protectionism, as a tailwind for smaller domestically oriented companies. These companies will be less impacted by uncertainty around global trade or economic slowdowns in the U.S. and China.

“High quality + low price” is the sweet spot for UK investors

- The underperformance of UK domestics and mid/small caps are providing stock selection opportunities in market leaders that sold off with their lower quality peers. Consumer-exposed names in particular have been hit hard on inflation and growth concerns, but the belief is that these environments ultimately lead to the strong getting stronger. Investors are finding opportunities in best-in-class companies that are also the lowest cost operators and well-positioned to defend margins and volumes—particularly in areas such as food & beverages and clothing retail. Heightened market volatility can offer opportunities to access such names at attractive valuation levels on a medium-to-long-term outlook.

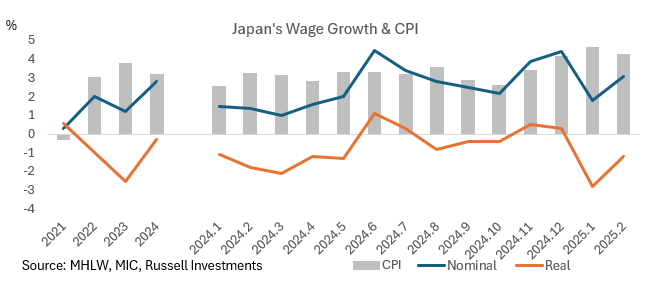

Japan Equities

Significant increase in uncertainty due to Trump’s tariffs

- While many managers remain relatively optimistic about the long-term outlook for banks, some are reducing their exposure in anticipation of a slower pace of policy normalization from the BOJ.

- In addition, more managers are forecasting a strengthening of the yen against the U.S. dollar, driven by declining confidence in the dollar or a potential narrowing of interest rate differentials. This has led to a shift toward domestic demand-oriented stocks, underpinned by expectations of a recovery in real wage growth.

- Amid this heightened uncertainty and difficulty in predicting macroeconomic trends, managers are increasingly focusing on stock-specific opportunities.

Rising concern over competition from Chinese manufacturers

Rising concern over competition from Chinese manufacturers

- Japanese manufacturers, especially in the tech and auto sectors, are facing pressure as China intensifies its focus on domestic production. This shift threatens market share and pricing power of foreign firms operating in China’s manufacturing industry.

- While many investors are scaling back their tech exposure, some value-focused managers are selectively adding to stocks they believe are resilient amid rising competition from Chinese firms, driven by attractive valuations.

Canadian Equities

Reducing cyclicality

- Investors are favoring more defensive companies with stable demand profiles, such as consumer staples and utilities.

- At the margin, they are using market volatility and price weakness as an opportunity to rotate from more cyclical sectors—like consumer discretionary and energy—into comparable stocks that offer lower leverage and stronger balance sheets (and, in the case of energy stocks, higher dividends).

Positive outlook for gold and metals

- Materials was the strongest-performing sector in Q1, driven by a surge in gold prices as volatility linked to tariff uncertainty persisted. Managers are increasing their exposure to gold and precious metals mining royalty companies due to their defensive nature, expecting continued uncertainty around tariffs and inflation in the near term.

- While gold miners are favored as an inflationary hedge, investors continue to be bullish about the multi-year growth opportunity for copper mining companies.

Opportunities and rotations within financials

- Managers are using the volatility to add to long-term secular growth names within financials, specifically in wealth management and alternative asset managers.

Opportunities in information technology

- Although the broader investor outlook for information technology remains cautious, managers are monitoring the sector for potential buying opportunities as valuations become more attractive.

Idiosyncratic defensive stories

- Against a backdrop of heightened volatility and concerns around stagflation, investors are seeking defensive, idiosyncratic stories—particularly within industrials—that can grow independently of the broader economic environment.

Australian Equities

Attractive defensive stocks

- Managers are holding companies that they expect will perform better in an economic slowdown. However, what is considered defensive varies. Gold mining stocks are broadly accepted as defensive as prices move in sync with the gold price.

- While historically defensive, some managers are concerned with consumer staples, noting increased competition and potential for decline in demand. Meanwhile, consumer discretionary and industrial companies with low leverage, an ability to maintain margins and quality products are considered attractive.

Assessing tariff impacts

- Managers are considering the impact that U.S. tariffs will have on companies, including both direct impact as well as secondary impacts of a U.S. economic recession. There are few companies which are expected to be directly impacted, as the majority of Australian equities are either domestically focused or have U.S. exports as a minor portion of revenue. Some companies are expected to benefit—either due to a lower Australian dollar making products cheaper or increased demand from other countries with reciprocal tariffs on U.S. goods. Managers are not actively trading, however, due to uncertainty regarding the tariff endgame.

Preparing for China stimulus

- Holdings in industrial metals and mining companies, particularly iron ore and copper producers, are being maintained. Managers view the companies as attractive on bottom-up fundamentals and observe that a significant new supply of iron ore will not come online until 2026, supporting current-year iron ore prices. Investors expect upside if the Chinese government stimulates to support their economy.

Real Assets

Listed vs. non-listed – Tactical opportunities in listed REITs

- Daily trading in listed REITs reflects real-time risk and volatility, which currently offers an opportunistic landscape for active REIT managers relative to more stable private asset values.

- Valuations continue to favor listed REITs.

- Investors expect transaction volume in private real estate to remain low in 2025, as market participants delay decision-making due to geopolitical and market uncertainty.

- Managers expect sector performance dispersion to widen.

Listed real estate – Optimistic uncertainty

- The direct impact of tariffs on REITs is expected to be minimal due to the domestic focus of REITs, but a trade war has potential to restrain capital investment, particularly in the industrial and logistics sectors.

- Despite macroeconomic uncertainty, rate cuts are expected later in 2025, which should serve as a tailwind to REITs.

- Managers are most optimistic on senior housing, where an aging population is expected to outpace supply for the next decade.

- Real estate investors are modestly rotating out of the U.S. and into Europe and the UK, where they’ve found attractive valuations.

Infrastructure – UK turns on the taps

- Managers have been overweight select UK water utilities due to the expectation that the regulator would allow increased returns to encourage necessary capital expenditure to improve the operation and resilience of the water supply and sewerage networks. This proved correct, with British water regulator Ofwat increasing the allowed returns for the sector in late December 2024. Managers are retaining their holdings due to the defensive nature of the water utilities.

- Across regions, managers expect the direct impact of increased tariffs imposed by the U.S. to be low, given the domestic and monopolistic focus of most infrastructure sectors.

Copyright © Russell Investments