by Carl Tannenbaum, Vaibhav Tandon, Ryan Boyle, Northern Trust

President Trump has been a vocal admirer of China’s Great Wall, built by the country’s emperors to protect their territory from outside aggression. In his first term, he compared his plan to build a border wall with that historic structure. Now in his second term, the President is attempting to erect even a bigger wall of tariffs to halt goods flowing in from all over the world.

Under pressure from a recent sell-off in financial markets, the president has decided to keep his tariff wall somewhat lower for now. But U.S.-China trade tensions that are swiftly escalating to a point of breakdown will have consequences for every participant along supply chains between the two nations.

Reciprocal tariffs may never come to full fruition, but the 10% universal levy and sectoral duties are here to stay. These will be enough to impair growth, pushing major markets closer to economic stagnation. The degree of stress will depend on reactions and retaliations.

The reciprocal tariff delay has raised hopes of the U.S. administration’s willingness to strike deals. But if the ultimate objective is to reindustrialize the American economy, then a lengthy and costly global trade war will end in losses for all participants.

Following are our thoughts on how top markets are faring.

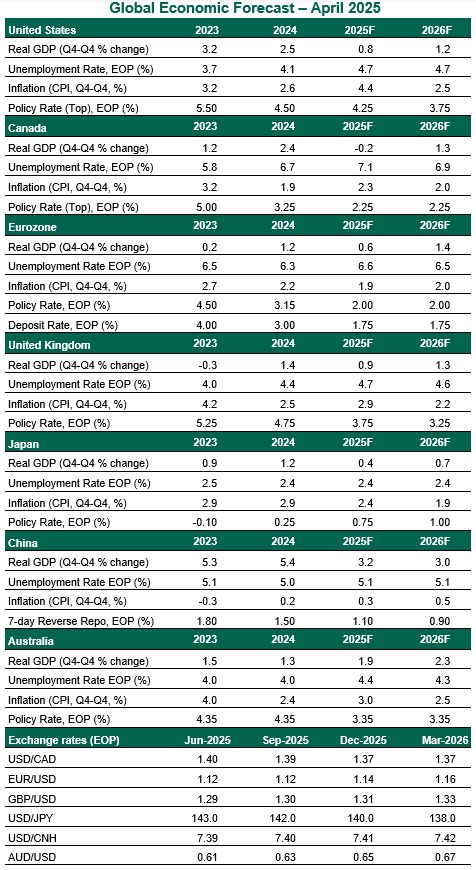

United States

- The foundation of the soft landing has been the resilient labor market. But the uncertainty created by the trade war may lead firms to trim headcount. Rising unemployment will be the greatest risk to growth. Inflation is likely to rise this year as tariff costs flow to final prices, with conditions settling somewhat during the balance of 2026. We see the U.S. economy growing at its slowest pace in several years. A downturn is not our base case but is very much possible.

- The Federal Reserve’s job is complicated. They have focused on their mandate to contain inflation and will be hesitant to risk a resurgence by cutting too soon. Softening labor market conditions may compel them to resume easing in September, and gradually thereafter.

Canada

- The tariff carveouts for Canada are not materially different from our initial expectation. Metal and auto duties are likely to remain in place at least until the renegotiation of the United States-Mexico-Canada Agreement next year. Given Canada’s close linkages with the United States, the economy is at risk of cracking under protectionism. Rising trade tensions with the U.S. are a powerful tailwind for the Liberal Party in the run-up to April 28 election; the results will help to shape Canada’s negotiating stance with the U.S.

- The first impact of heightened trade tensions was seen in the labor market. March marked the first drop in Canadian employment in three years; uncertainty appears to have weighed on business confidence and slowed hiring. Despite an economy staring at a recession, the Bank of Canada (BoC) appears to be more focused on upside risks to inflation, as it kept the policy rate unchanged in April. While the BoC is holding rates steady for now, weakening activity will drive the central bank to resume easing this summer. We expect the BoC to take policy rates down to 2.25%, the low end of their neutral range.

Eurozone

- Amid heightened trade uncertainty, the optimism from the recently announced German fiscal stimulus has faded. 10% across-the-board and 25% sectoral levies on exports to the U.S. will depress growth in 2025, offsetting any limited positive impulse from fiscal expansion. The scope for an escalation has diminished for now: 34% reciprocal tariffs are on a 90-day pause, and the bloc postponed its first set of retaliatory tariffs targeting €21 billion of American goods. But the United States’ insistence on involving Europe’s value-added tax in negotiations could seal the fate of talks. A full blown-trade war with the U.S. will push the bloc into recession.

- As expected, the European Central Bank (ECB) lowered its policy rates by 25 basis points at the April meeting. While the central bank was starting to sound more cautious on further rate cuts, greater concerns around growth have led to officials dropping the reference to monetary policy becoming “restrictive” from their statement. A stronger euro, if sustained, will support disinflation. We continue to expect the ECB to reach a terminal deposit rate of 1.75%.

United Kingdom

- GDP rebounded sharply in February, following a contraction at the start of the year. But the positive outcome overstates the underlying strength of the economy. Business surveys have been softer, owing to uncertainty around trade and the hike in employers’ national insurance (NI) contributions. The U.K. is not facing reciprocal duties from the United States, but knock-on effects of a global trade war will have a bearing on growth.

- The British labor market remains tight, and wage growth is still above the rate consistent with the Bank of England’s (BoE) 2% inflation target. The central bank will be closely monitoring the impact of U.S. tariffs, the increases in the National Living Wage and NI contributions on consumer prices and labor markets. Elevated uncertainty around the path of disinflation will lead the BoE to reduce rates gradually in 2025. But the threat of tax increases in the Autumn budget could force the central bank to accelerate the pace of easing.

Japan

- The combination of higher U.S. auto levies and weaker demand from major centers is casting a long shadow on Japan’s growth outlook. To enhance prospects of a trade deal with the U.S., the Japanese government is not willing to impose any counter measures. Another year of strong wage increases will provide some support to domestic demand, thereby preventing an outright contraction.

- With wages and price developments still playing out largely in line with the Bank of Japan’s expectations, we continue to expect the central bank to hike again later this year. That said, continued market volatility, a stronger yen, and the hit from America’s trade tensions could push monetary policy normalization further into the future.

China

- Not long ago, the sky was the limit for trade between the world’s two largest economies. Today, only the tariffs are heading in that direction. China is the primary target of the president’s trade offensive as U.S. levies on China surged to 145% in a matter of days. Beijing has struck back with 125% taxes on American imports, but has indicated it won’t go further.Downward pressures on growth are mounting. At present, front-loading of export orders and the incentive to continue rerouting and white labeling through other nations has maintained a baseline level of output. But China will struggle in fending off deflationary forces as falling external demand will add to excess capacity. Depressed or negative returns from assets like property and equities will make consumers even more cautious.

- The Chinese government will use all available policy tools to provide a cushion to the economy. We expect more substantial fiscal stimulus, along with monetary easing and continued gradual depreciation of the renminbi (RMB). The RMB weakened to its lowest level since 2007 in the latest sign that Beijing is willing to use a weaker currency to combat U.S. tariffs. A sharp depreciation will further draw the ire of the U.S administration and would go against the country’s desire of having the currency play a bigger role in international trade and settlements. Capital flight would also be a risk under this scenario.

Australia

- Australia has escaped “lightly” with the minimum tariff of 10%, thanks to its trade deficit with the United States. The U.S is also not one of the top destinations for Australian goods. Therefore, the direct impact of duties will be negligible. But the knock-on effects from further escalation in trade frictions are poised to be far greater. China is Australia’s largest trading partner; the health of China’s economy will also be crucial to this commodity-dependent economy. On the domestic front, the economy will be underpinned by a still-strong labor market, moderating inflation, and cost-of-living rebates. Australia will go to the polls on May 3 in what could be a tight race, with cost-of-living concerns at the top of voters’ minds.

- The Reserve Bank of Australia (RBA) kept the cash rate steady at its April meeting, which predated the U.S tariff-driven market swing. With monetary policy still in restrictive territory and progress on disinflation broadly in line with expectations, we think the RBA will resume its easing cycle next month.

Copyright © Northern Trust