by Carl Tannenbaum, Chief Economist, Northern Trust

Can the U.S. economy weather the shock of tariffs?

The theme of the past five years has been resilience. Businesses and consumers adapted to pandemic disruptions; first shutdowns, and then reopenings. The ensuing inflation created widespread expectations of recession, but economic momentum carried the day. The pandemic cycle is now history, but the challenge of a trade war is on the horizon. We see a path for the U.S. economy to forge ahead, but a downturn is very much possible.

The deferral of “reciprocal” tariffs on most U.S. trading partners suggests that the peak of tariff uncertainty may have passed. However, the new 10% ad valorem base tariff and stringent levies on metals and autos remain in force. China has not escaped the Administration’s ire, and has retaliated in kind. The new global landscape will weigh heavily on an economy that was already cooling.

A decline is not yet evident in economic data. This publication will focus less on current results and more on what we will watch to calibrate the economy’s fate.

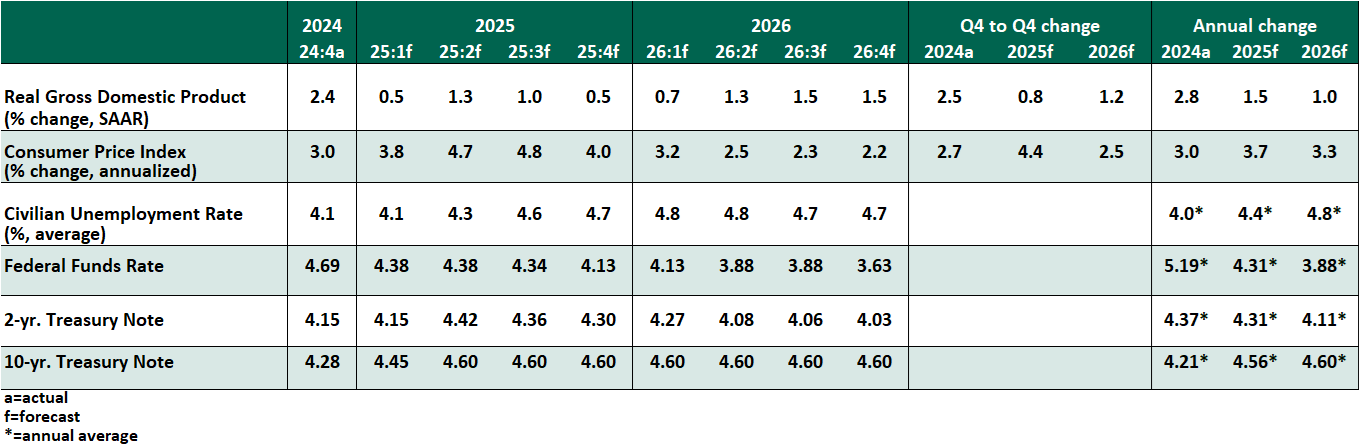

KEY ECONOMIC INDICATORS

INFLUENCES ON THE FORECAST

- The foundation of the soft landing has been the labor market. Consumers were able to work through widespread uncertainty because employment prospects were strong. Job openings were ample, and wage gains caught up with inflation. But in the past year, turnover has stagnated: layoffs have been minimal, but hiring and quitting have been diminished. The uncertainty created by the trade war could lead firms to manage headcount more conservatively.

We will closely watch trade-exposed sectors like transportation, wholesaling and retailing. Tourism is already feeling U.S. boycotts, as foreign visitors reconsider their plans. These sectors alone represent over 43 million workers, or 27% of employment.

We see few prospects for any sector to pick up any slack that might be created in the labor supply. Hiring by the federal government has flatlined, and cuts are looming for sectors reliant on government funding, like healthcare and higher education. Unemployment is poised to rise this year, the greatest risk to the growth outlook.

- The extent of inflation will be difficult to judge. Tariffs are a tax on imports; the cost will weigh on margins and flow through to final prices. Rising price levels will create a surge of inflation this year, with conditions settling during the balance of 2026.

- Consumer spending is the largest component of U.S. gross domestic product (GDP). Even in this volatile cycle, consumption never stopped rising. The current quarter may even see some gains in retail sales as consumers pull forward major purchases ahead of the risk of tariff-driven price adjustments. Past that, however, the outlook is not robust: stimulus programs and pent-up savings are long depleted, and the labor market has cooled. Inflation will reduce real purchasing power. Consumers will almost certainly adjust their spending intentions, which will limit growth over the balance of the year.

- More tariff escalations may be in store, but we do not expect tariffs to return to the maximal rates touched at the start of April. Reciprocal tariffs may gradually be lifted, though not at a rapid or predictable cadence. However, the 10% ad valorem tariff, as well as product tariffs on autos and metals, are likely to endure.

- The Federal Reserve’s job is complicated. To date, they have prioritized taming inflation and will be hesitant to risk a resurgence by easing too soon. However, we expect rising risks to employment will compel them to cut starting in September, continuing cautiously thereafter.

The walk-back of the reciprocal tariff plan suggests the White House is watching the bond market as a measure of success. We expect policy uncertainty and fiscal imbalances to keep 10-year Treasury yields elevated, a tighter financial condition that will also serve as a check on growth.

- Slowing growth and rising unemployment can easily push an economy into a recession. The odds of this outcome are elevated. While the two most recent U.S. recessions were especially severe, most downturns are shallower. If the expansion ends, we would brace for a shorter, more mild contraction.

- Tariffs have potential upsides. They produce revenue can be used to reduce the federal deficit. We expect they will be counted as an offset to lower taxes in the pending reconciliation package, though few details have been released. They could also bring about more jobs and more resilient supply chains, but these may take a long time to manifest.

Copyright © Northern Trust