by Carl R. Tannenbaum, Chief Economist, Vaibhav Tandon, & Ryan Boyle, Northern Trust

The Northern Trust Economics team shares its outlook for growth, inflation and interest rates in major markets.

Fall is the time for change. The days grow short, the air turns cooler, and trees shed their foliage. This autumn, flocks of birds aren’t the only things moving south, as central banks are trying to gently push interest rates downward.

Policymakers are able to ease their stances because inflation is under better control. The drive to achieve soft landings is now focused on preserving growth and employment. The pace of interest rate reductions will be determined by regional circumstances.

Geopolitics are still top of mind. Escalating tensions in the Middle East and on the eastern borders of Europe have the potential to disrupt. The U.S. presidential election, just weeks away, could also make a mark on the global outlook.

Following are our thoughts on how major economies are faring.

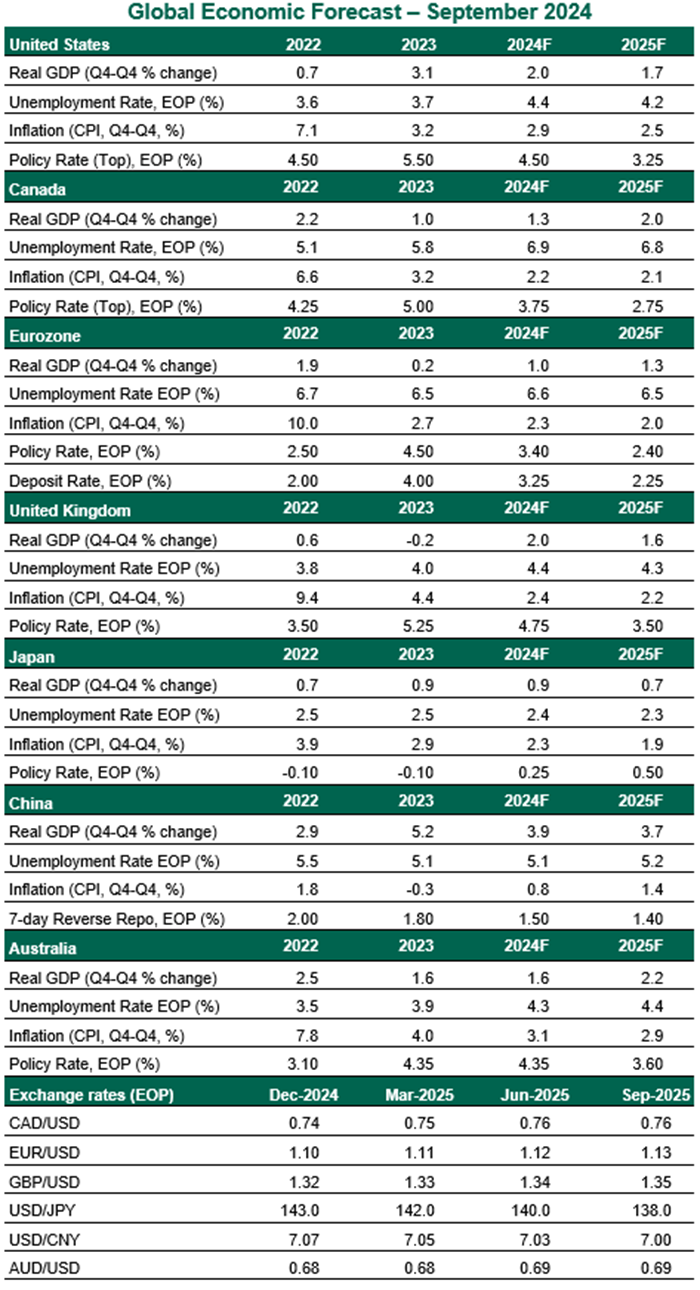

United States

- The Federal Reserve commenced its easing cycle with a 50 basis point cut, the first reduction in four years. Despite a larger than expected cut, Chair Powell stressed that this was not a distress signal, but a “commitment to not fall behind the curve.” The Fed’s Summary of Economic Projections showed 50 basis points of additional cuts in 2024 and 100 basis points in 2025, progressing toward a neutral rate just over 3%. We expect a string of 25 basis point reductions through mid-2025.

- The FOMC’s decision was supported by further progress on disinflation. Both headline and core PCE inflation remained steady at 2.5% and 2.6% year over year in August, in contrast to expectations of a small increase. Though sticky, readings of this magnitude are soft enough to justify rate cuts. A cooler labor market, reflected in lower payroll gains, a higher unemployment rate and slower turnover, also warrants easier monetary policy. That said, a soft landing is coming into view.

Canada

- The annualized pace of real growth improved slightly to 2.1% in the second quarter, but the Canadian economy continues to perform below its potential. Consumer spending slowed as households struggle with rising mortgage payments. The housing market remains in the doldrums. The unemployment rate has jumped almost 2 percentage points in the past two years to 6.6%, and is likely to increase further. The government is focused on containing immigration, but this could cut into growth.

- Inflation dropped to the Bank of Canada (BoC)’s 2% target in August for the first time since early 2021. In light of this progress, the central bank delivered a third consecutive 25 basis point cut this month, lowering the policy rate to 4.25%. With inflation back at target and economic momentum slowing, we expect the BoC to push ahead with 25bp rate reductions until the interest rate settles at a neutral level of 2.75% in mid-2025.

Eurozone

- The eurozone economy lacks momentum. Second quarter real growth was revised down one-tenth to 0.2% quarter over quarter, and underlying momentum in the region remains soft. Net trade was the main driver of growth, while private consumption was flat, and investment dropped at a faster pace. The industrial sector is struggling, and services are unable to make up for the shortfall. While the bounce from the Paris Olympics will aid the French economy in the current quarter, lasting weakness in German industry is a cause of concern. Soft growth remains our base case for the second half of the year as employment and incomes are still increasing, but the risks to the near-term outlook are tilted to the downside.

- As expected, the European Central Bank (ECB) lowered its policy rates by 25 basis points at the September meeting. While the ECB revised its growth forecasts down, it reaffirmed its “data-dependent and meeting-by-meeting approach.” The Governing Council is likely to stick to a quarterly pace of reductions in 2024, implying the next move awaits in December. Further deceleration in core inflation alongside a drag from fiscal policy will allow the central bank to speed up the pace of easing to sequential steps early next year.

United Kingdom

- The U.K. economy enjoyed a strong first half of the year, and is carrying healthy momentum into the second half. The Purchasing Managers’ Index is still expanding, and retail sales have increased for two successive months. However, the current pace of economic growth is unlikely to be sustained as weaker wage growth, elevated interest rates and persistent supply constraints limit output. Given the stretched position of British public finances, the Autumn Budget on October 30 will likely deliver tax increases and tweaks to fiscal rules to allow more capital spending.

- Labor market conditions remain strong in the U.K. The unemployment rate dropped further to 4.1% in the three months ending in July. Private sector pay is still growing at a strong pace of 4.9% year over year. The Bank of England (BoE) held its overnight rate steady at 5.0% this month, signaling a cautious easing cycle. British labor market dynamics remain consistent with a quarterly pace of rate cuts. However, the BoE could accelerate the pace of easing in 2025, to prevent undue damage to the economy.

Japan

- Japan’s economy rebounded in the second quarter with real growth of 2.9% annualized, following a 2.4% contraction in the first three months of the year. Signs of passthrough from strong wage negotiation to consumer spending are starting to appear, as private consumption turned up for the first time in five quarters. Business investment increased, led by normalization of auto production. Exports moderated last month, but are likely to remain healthy. A modest expansion led by higher incomes and consumption is our base case for the Japanese economy.

- The Bank of Japan (BoJ) maintained its policy rate at 0.25%, signaling it was in no rush to hike following the financial market turmoil after its hawkish tilt in July. Governor Kazuo Ueda stated that the recent strengthening of the yen has reduced upside risks to the price outlook. We think the BoJ will be in a wait-and-see approach with the yen regaining some strength and the country facing an increasing likelihood of an early autumn election. Another rate hike looks unlikely in 2024.

China

- The Chinese economy is stumbling amid further loss of momentum. Growth in consumer spending remained flat in August, and confidence is low. Several categories of retail sales are contracting. The rate of expansion in infrastructure and manufacturing investment softened further. The property sector remains depressed. A slowing economy will deepen a deflationary loop: Headline inflation edged up to 0.6% year over year on higher food prices, but core inflation moderated further in August. Deflation at the producer level persists.

- The string of weak data pushed policymakers to announce a raft of policy measures this week, which included one-off cash handouts to the poor, relatively large cuts to the key policy rate, reserve requirement ratio and mortgage rates. Calls for big fiscal stimulus are growing, but it may not be enough to put the economy back on a sustainably stronger path. China is witnessing a structural slowdown, not just a cyclical weakness that can be countered through demand-side programs or other confidence-lifting measures. The U.S. election could also prove to be consequential for the economy as new tariffs and barriers will likely be erected after November.

Australia

- Australia's economic growth improved, but was still weak at 0.9% annualized in the second quarter. The economy lacks a driver of growth, as households tighten their belts and real incomes are squeezed. Public demand propped up growth, but likely at the cost of exacerbating inflationary pressures. Labor market dynamics will continue to underpin activity, but the economy will continue to perform below its potential.

- The Reserve Bank of Australia (RBA) continues to defy the global trend of easing. The central bank held rates steady at its September meeting, emphasizing that the Board “is not ruling anything in or out” and that “policy will need to be sufficiently restrictive until the Board is confident that inflation is moving sustainably towards the target range.” We expect inflation to cool, but not enough for the RBA to pivot as other central banks have done this year. A short easing cycle is our base case, but not before the new year.

Copyright © Northern Trust