by Russ Koesterich, CFA, JD, Portfolio Manager, BlackRock

In this article, Russ Koesterich discusses why the next bout of market volatility may last a bit longer than previous downturns and how to best position your portfolio against this backdrop.

Key takeaways

- While fall has historically been a weaker period for equities, this year may be compounded by extended seasonal weakness.

- In this environment, investors should consider hedging strategies to help protect gains in their portfolio.

- One solution is to purchase put options which are currently pricing at historically cheap levels.

In early August investors experienced a violent, albeit brief spike in market volatility. If seasonal patterns are any guide, the next spike may last a bit longer. As we enter fall, historically one of the weaker periods of the year, investors should consider hedging strategies to protect this year’s substantial gains.

I last discussed seasonality back in the spring. I highlighted that while there is some truth to the adage, ‘Sell in May and go away’, election years tend to have somewhat different seasonal patterns. Rather than summer weakness, markets are more likely to stumble in the fall. Year-to-date this pattern has held. Even after suffering a near 10% drawdown in early August, as of late August the S&P 500 is 10% higher than it was in late April.

But while stocks have remained resilient, and solid year-to-date momentum suggests more gains into year’s end, seasonal patterns are now turning less favorable. This suggests not only weaker returns but also higher volatility. With current implied volatility below average, as derived from options pricing, investors have an opportunity to hedge their equity exposure with relatively cheap options.

Investing involves risks: Options involve risk and are not suitable for all investors. Prior to buying or selling an option, a person must receive a copy of “Characteristics and Risks of Standardized Options.” Copies of this document may be obtained from your broker, from any exchange on which options are traded or by contracting The Options Clearing Corporation, (1-888-678-4667).

During election years going back to 1990, the CBOE Volatility Index (commonly referred to as the VIX index), which tracks implied volatility on the S&P 500 Index, has typical risen around 10% in September and another 25% in October. This equates to an average VIX level of 25 in the October preceding a U.S. Presidential election.

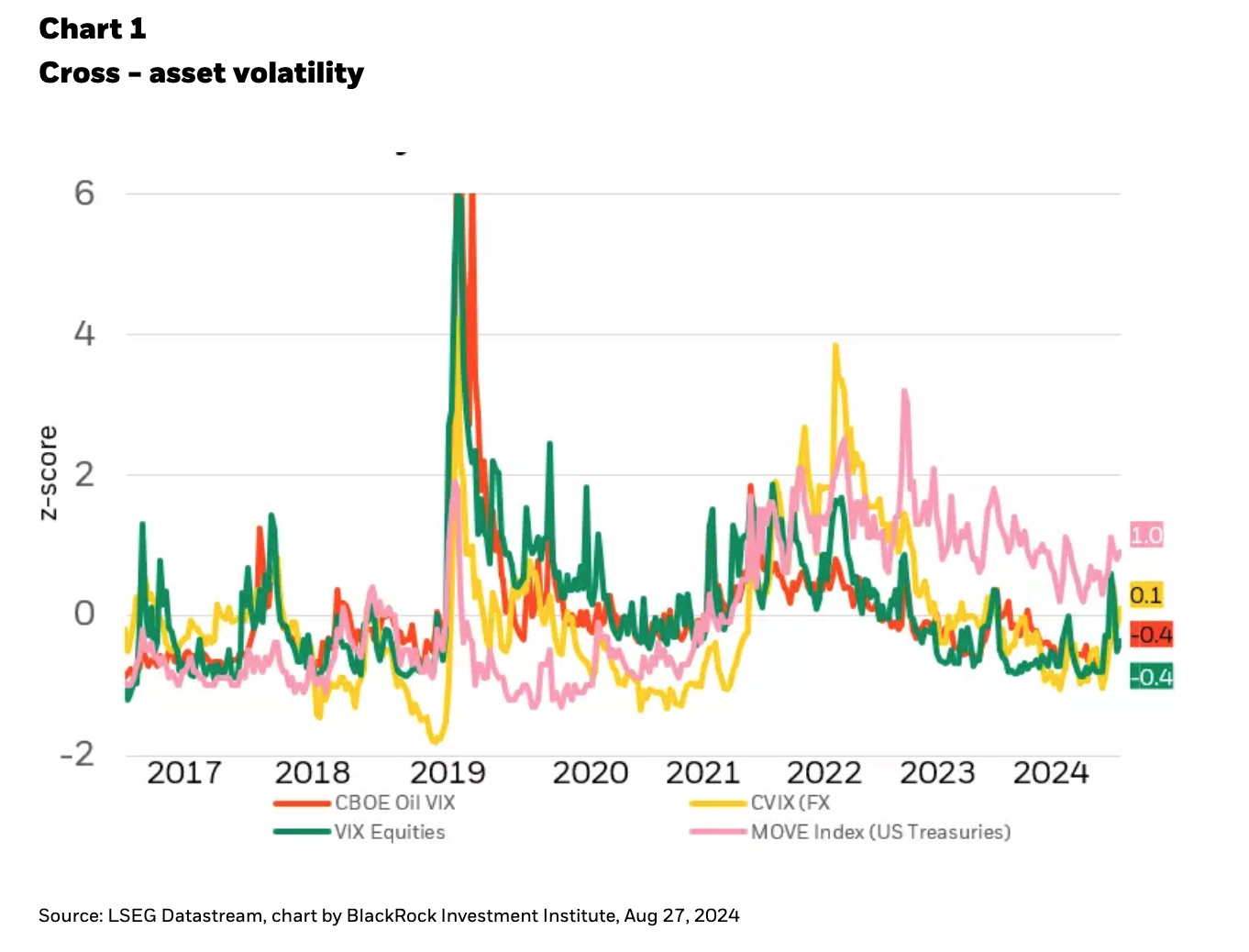

As of late August, markets did not appear to be discounting the traditional rise in volatility. While equity volatility spiked in early August, the rise, while historic, was remarkably short lived. By the end of the month, implied volatility had faded, back near the long-term average across multiple asset classes (see Chart 1).

Not only is current volatility modest, but looking at future contracts on the VIX Index, investors are not expecting a significant rise any time soon. The October contract suggests only a small rise in volatility in October, to approximately 18, versus the average level of 25 in prior election years.

While recent economic data, particularly strong July retail sales report, has allowed investors to breathe a sigh of relief, there are some legitimate sources of volatility lurking in the background. In the coming months, investors will need to balance the risks of a slowing economy, aggressively priced expectations for Fed rate cuts, lingering geopolitical risk and what is likely to prove a close election. All of which suggests that equity volatility has the potential to rise significantly from current levels.

Use cheap option volatility as a hedge

Last month I advocated trimming equity exposure and emphasizing consistency in portfolios. A third strategy for investors to consider is to use cheap volatility to buy protection, i.e. put options and structures that rise in value in the event of a decline in price and/or a rise in volatility. Currently, these options are unusually cheap, providing an opportunity to protect gains as the traditional summer lull comes to an end.

Copyright © BlackRock