by US Equities, AllianceBernstein

US equity market returns have been disproportionately driven by the so-called Magnificent Seven (Mag 7) stocks this year. Their dominance has created style imbalances within large-cap benchmarks that deserve closer attention from investors.

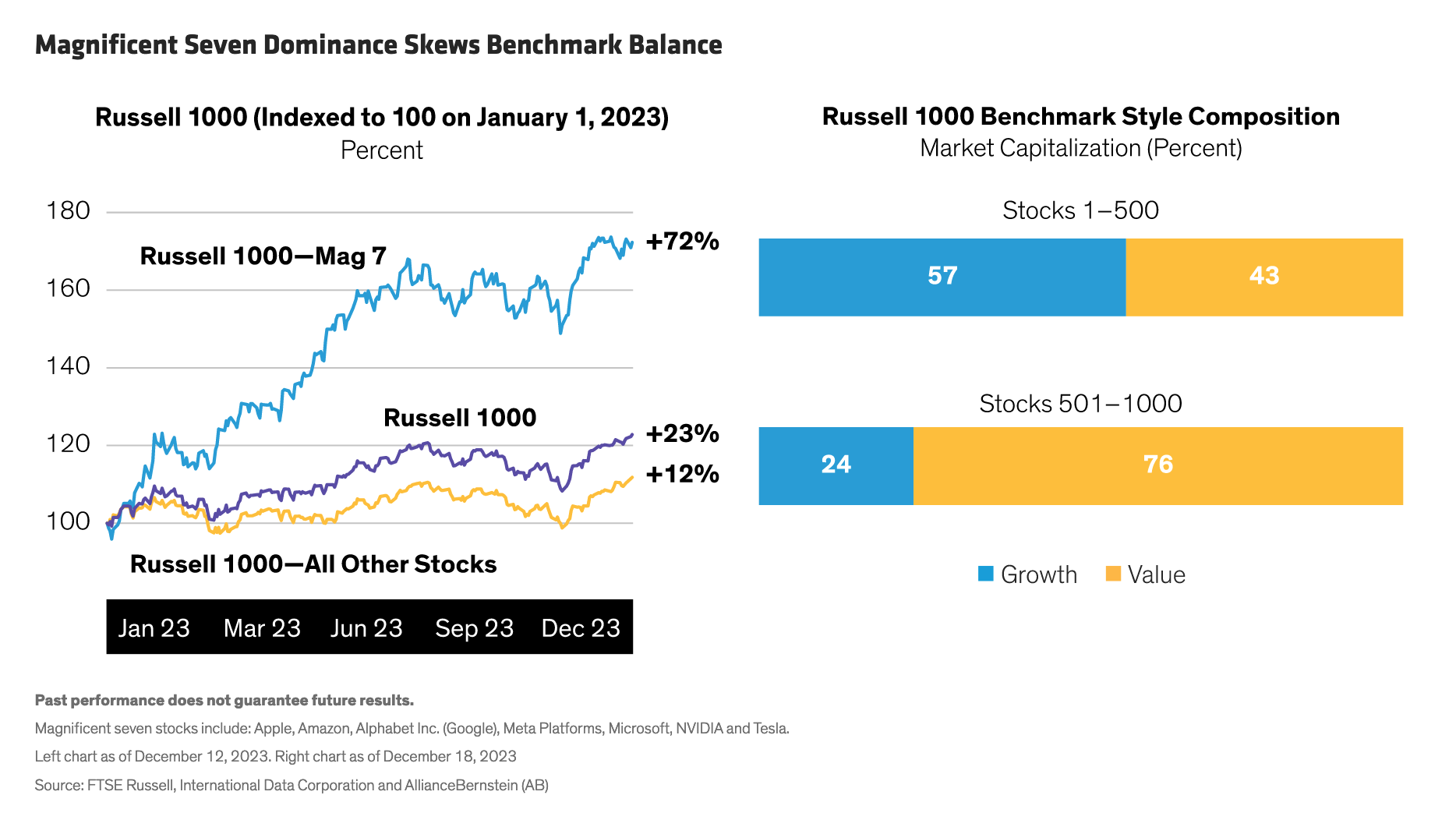

In a dramatic year for equity markets, the biggest actors on the US market stage hogged the limelight. The seven largest stocks in the Russell 1000 Index, which account for about 28% of the large-cap benchmark, surged by 72% through December 12—eclipsing returns for the rest of the market (Display). Similar trends were seen in global markets, such as the MSCI World, where the US Mag 7 stocks account for 19% of the benchmark.

The heavy market concentration in the Mag 7, which are seen as the big winners from the artificial intelligence revolution, profoundly affected investor outcomes. Portfolios that held all seven—Apple, Amazon, Alphabet Inc. (Google), Meta Platforms, Microsoft, NVIDIA and Tesla—enjoyed supercharged returns. Actively managed portfolios that didn’t own some of these stocks were saddled with big underweight positions, making it almost impossible to beat the benchmark—especially since the rest of the market underperformed.

Backstage at the Benchmark

Extreme market concentration has had other, less visible effects on the market. In particular, the style composition of key equity benchmarks has been skewed in surprising ways.

Index providers typically target a balanced style split between growth and value stocks in broad market benchmarks. Since the Mag 7 are mostly growth companies, their weight in the Russell 1000 creates a skew across the market-capitalization spectrum. The largest 500 companies in the Russell 1000 are somewhat tilted toward growth stocks. And as a result, the next 500 companies are heavily skewed toward value stocks—accounting for 73% of the weight in this segment of the market.

Heavy Concentration Adds Risks

Why does this matter to investors?

First, the heavy concentration of larger weights in growth stocks adds benchmark risk. Passive investors enjoyed the Mag 7 rally but are also exposed to a potential turn in sentiment because of a lack of diversification in the index and the increasingly correlated trading patterns of these names. To be sure, the mega-caps include attractive companies, but we believe they should be held in accordance with a portfolio’s investing philosophy at appropriate weights after a comprehensive evaluation of each stock’s business potential and valuation.

Second, investors in mid-cap stocks, the 800 smaller companies in the Russell 1000, must be aware of the unusually high concentration of value stocks relative to history. Value stocks require a different type of analysis than growth stocks for investors to identify the best long-term opportunities.

Finally, unseen style biases warrant strategic consideration, in our view. Investors should proactively verify that their passive and active portfolios across an equity allocation are positioned with appropriate style exposures for their long-term objectives.