by Vaibhav Tandon, Senior Economist, Northern Trust

I still like playing board games with friends and family for amusement during my leisure time. Recently, I have been enjoying the game ‘Catan,’ a settlement-building activity in which up to four players compete to earn resources and construct buildings across a small island. It involves trading with others to grab the resources you most need, enabling the creation of new settlements that earn victory points.

Roads do not provide victory points, but they are crucial for establishing new developments. The same is true outside the fictional island of Catan: Roads are central to economic development. Sound infrastructure is crucial for an economy to realize its full potential. This is especially so for a nation like India, where infrastructure has been the missing piece in the country’s growth story.

India has been one of the fastest-growing major economies for the past decade, with an average annual growth rate of real gross domestic product (GDP) of 5.7%. It has stood out for its economic resilience during a time of global macroeconomic uncertainty and volatility. This year, India is clocking an impressive 7% real growth rate at a time when its peers are slowing down. It has managed a transition from being a “Fragile Five” member a few years ago to the world’s fifth largest economy today.

That track record and a series of recent pro-business measures have positioned India towards the top of the list of promising emerging markets. The appeal to potential investors goes deeper than just the push to make the business environment more friendly. India enjoys a demographic dividend with a young and growing population (a median age of just under 29 years), a large middle class underpinning its domestic consumer market and a rapidly expanding skilled labor force.

Over the next two decades, India’s old-age dependency ratio will be one of the lowest among regional peers. India also has the largest English-speaking population after the U.S., making it a favored destination for service industries.

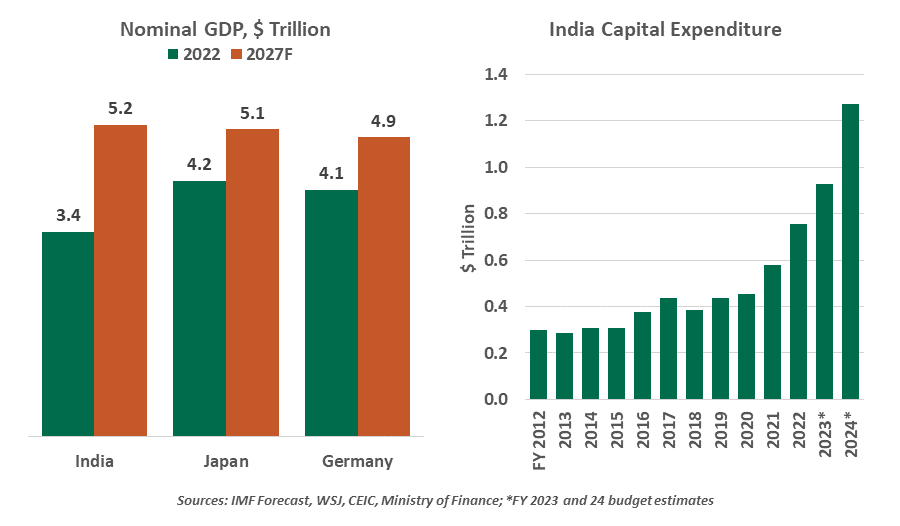

India enjoys reasonably good economic and political relations with major economies, an important consideration for businesses in today’s fragmented world. Rapid progress in technology, innovation and digitization are setting the stage for robust growth in the years ahead. While India is on track to overtake both Japan and Germany to become the third-largest economy by 2027, sustaining high long-term growth will depend on several factors.

India for decades has been plagued with an aging infrastructure, incapable of meeting the needs of a modern and growing economy. Weak road and rail networks are one of the main reasons why India has struggled in expanding its manufacturing base and failed to compete with likes of China in attracting factories. Lower labor costs alone will not be enough to make India truly a global manufacturing hub.

However, in recent years, the government appears to have its focus on addressing infrastructure gaps. Capital expenditure has surged: projects worth $1.3 trillion covering sectors like roads, railways, energy and irrigation are underway. More than $120 billion has been budgeted for capital expenditure in the current fiscal year, a 37% increase over the previous year and more than double the amount spent in 2019. India’s National Logistics Policy seeks to improve the country’s ranking in the World Bank’s Logistics Performance Index from 38 to 25 while reducing logistics costs from 14% to 8% of GDP within the next five years.

New airports and expansion of existing terminals are underway. New roads are being added every month. An increasing number of cities are adopting mass transit systems. The state-owned Indian Railways, the main artery for inland transportation, continues to expand and modernize with an enhanced focus on safety. According to the Organization for Economic Cooperation and Development, India now has more miles of electrified railway than the U.K. or France.

Development of infrastructure is vital for sustaining high growth as it will have a multiplier effect on demand and create more commercial opportunities. The massive outlays are already helping attract more interest from overseas. Foreign direct investments into India have doubled in less than a decade, averaging $42 billion annually in the last three years. This will also make the economy better equipped to manage growing volumes of international trade, to cash in on the ‘China Plus One’ opportunity.

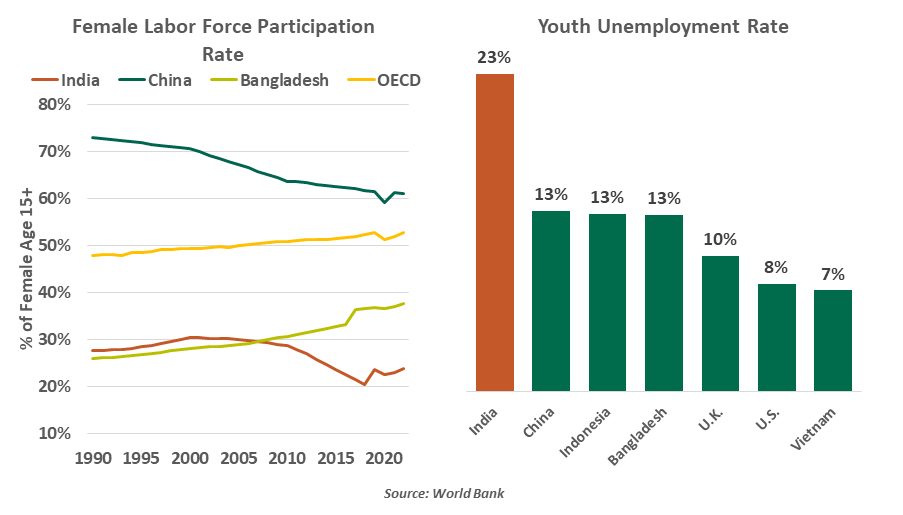

India will need to think beyond physical assets to continue its growth; it must become more inclusive of all human capital. According to the Centre for Monitoring Indian Economy, only 38 million women were in paid employment in India in 2022, compared with 368 million men. With a female labor force participation rate of 23%, India lags behind other economies, including countries like Bangladesh. The majority of Indian women work in the informal sector, leaving them without any social security or bargaining power. Women were instrumental in China’s economic rise and will do the same in the world’s most populous country, according to the McKinsey Global Institute.

Strong economic growth has helped lift millions of people in India out of poverty. But per capita income is only $2,400, which is less than one-fifth of China’s and even lower than Bangladesh’s. The country is at risk of stalling into a middle-income trap. Growing income inequality will not only be a recipe for social unrest, but will also weigh on growth. India’s economy also suffers from what many call ‘jobless growth,’ in which a growing workforce struggles to secure employment even as GDP increases. The unemployment rate has consistently increased from 2% in 2010, to 5% in 2015, to a record high of 8% in July 2023. India’s youth unemployment rate of 23% is the highest among advanced and emerging economies. India is trying to climb out of a giant pothole, but in the process is also leaving a sizeable chunk of its population behind.

In Catan, victory is gained by building settlements. This requires resources like bricks, lumber and ore. If India is to achieve victory in the game of economic development, it needs resources like physical and human capital in greater quantity. If these can be amassed in sufficient amounts, India will indeed become a champion.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions. © 2023 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.

Vaibhav Tandon, Vice President, Economist

Vaibhav Tandon, Vice President, Economist

Vaibhav Tandon is an Economist within the Global Risk Management division of Northern Trust. In this role, Vaibhav briefs clients and colleagues on the economy and business conditions, supports internal stress testing and capital allocation processes, and publishes the bank's formal economic viewpoint. He publishes weekly economic commentaries and monthly global outlooks.