by Nick Haupt, CFA, Russell Investments

Executive summary:

- Today's U.S. equity market is highly concentrated, with seven stocks contributing to an astonishing 96% of the Russell 1000 Index's year-to-date return.

- Periods of high market cap concentration tend to lead to a tougher environment for active management, because many equity managers tend to underweight mega cap companies.

- Because of this tendency, we believe it's crucial to work with managers who can identify idiosyncratic differences between mega cap companies and adjust weightings accordingly.

Who wants Apple in their lives more: My 10-year-old daughter and her peers or an active equity manager?

The answer may surprise you. But before we get to that, a bit of background on both.

My daughter has been recently bugging my wife and me for an Apple iPhone these past several months—primarily because so many of her classmates already have one. This request of hers made me realize just how extensively the Apple brand has penetrated households worldwide over the past few decades. And it's not just Apple—the impact that a handful of U.S. mega cap companies have had on consumers and investors alike during this timeframe is truly remarkable.

Case-in-point: In six of the last eight calendar years, the Russell 1000® Growth Index and the Russell Top 50® Mega Cap Index have outperformed the Russell 1000® Index by an average of 3.15% and 1.34% annualized, respectively. And while we saw a retrenchment in 2022 from this set of mega cap growth stocks—due to multiple contraction from rising interest rates—the group has roared back with a vengeance this year. For instance, through May 31, NVIDIA, Meta, Tesla, Amazon, Alphabet, Microsoft, and Apple are all up over 36%.

How concentrated is today's market in mega cap growth stocks?

It should come as no surprise, then, to learn that the U.S. equity market today is once again highly concentrated with mega cap tech companies. Just how concentrated is it? Consider this jaw-dropping stat: Through the end of May, 96% of the Russell 1000 Index's year-to-date return can be attributed to just SEVEN stocks. Seven—out of 1,000.

Put another way, if these seven stocks were excluded from the index, the actual return contribution from the other 993 stocks in the index would only be a modestly positive 0.34%—rather than the actual index return of 9.30%. Think about that for a second. A return of less than 1% versus a return approaching double digits. Wow.That's some serious market concentration.

Going even further, the Russell 1000 Equal Weighted Index has significantly trailed the market cap-weighted Russell 1000 Index by 10.90% year-to-date through the end of May, underscoring the massive impact that these mega cap growth companies have had on total returns. As the chart below shows, Apple's 2023 run has caused its current market capitalization to swell to $2.7 trillion—an amount now larger than the combined market cap of the Russell 2000.

How does active management typically fare in times of high market cap concentration?

It's undeniably clear that today's U.S. equity markets are highly concentrated. But how does this typically impact active manager performance? And is it in good ways or bad ways?

Digging into this more deeply, we found that periods of high market cap concentration tend to lead to a tougher environment for active management—and vice versa. For instance, when the top 10% of stocks in the Russell 1000 Index make up a greater weighting, active management tends to struggle on a trailing basis—and as this level of market concentration peaks, active management tends to have much stronger results on a go-forward basis as market concentration levels recede.

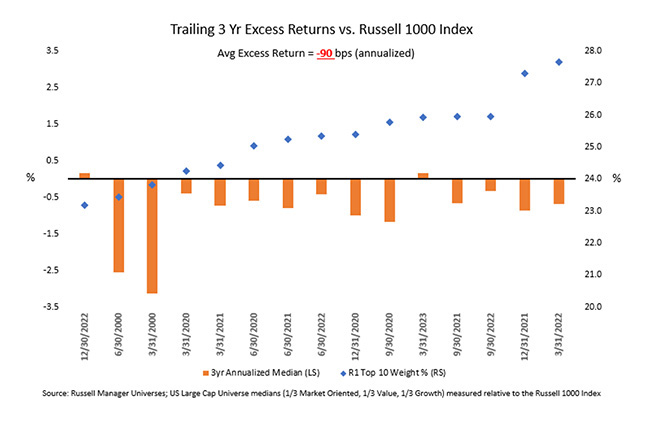

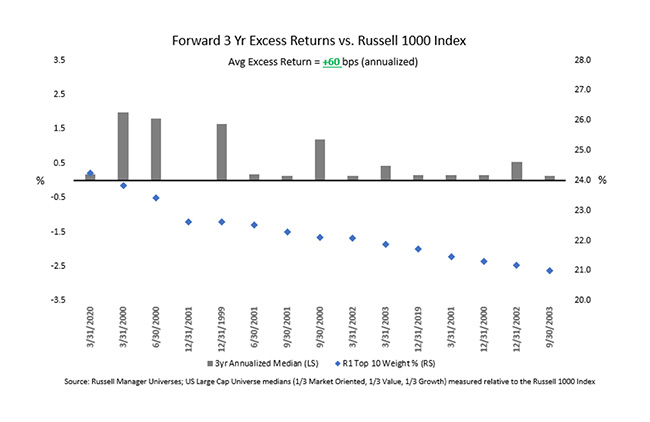

An example of this relationship can be seen in the charts below, which show how the trailing and forward performance of the U.S. large cap market-oriented, value and growth Russell universes is impacted by peak levels of index concentration.

Click image to enlarge

Click image to enlarge

As the first chart shows, the 3-year trailing periods leading up to extended levels of market concentration (shown are the top 15 such quarterly periods since 1999) have had a notable drag on active managers. For instance, the median U.S. large cap active manager trailed the Russell 1000 Index by an average of 90 basis points (bps), annualized, over the associated trailing 3-year periods where the index had its highest 15 concentration levels since 1999.

Now, let's look at the next chart, which shows 3-year forward periods directly following extended levels of high market concentration. This chart, which takes the top 15 periods since 1999 where forward 3-year data is available, shows that these time periods have been positive for active managers. As the chart shows, the median U.S. large cap equity manager outpaced the Russell 1000 Index by an average of 60 bps, annualized, over the associated forward 3-year periods where the index had its highest 15 levels of concentration since 1999 (where there was enough data to show the forward 3-year return).

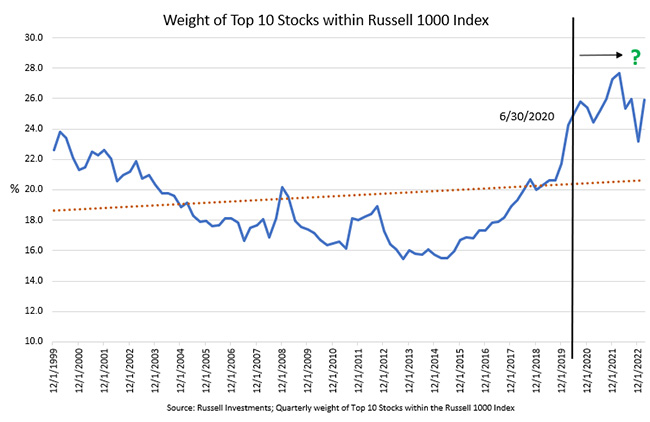

Additionally, the below chart shows the cutoff line where there is not enough data available to present the forward 3-year returns yet—in this case, it's June 2020—and the associated quarterly weight of the top 10 stocks within the Russell 1000 Index. Given the current extended levels of market concentration and the historical 3-year forward relationship shown above, perhaps the question we should all be asking ourselves is, could active management be primed for a strong comeback over the coming years?

Click image to enlarge

Why do some active managers underweight mega cap stocks?

This leads to the ultimate question: why does active management tend to perform better when market concentration is lower? Oddly enough, the answer to this may also be the answer to the question I kicked off this article with—whether 10-year-olds or typical active equity managers crave exposure to Apple more. In simple terms, the answer is that active managers tend to underweight mega cap companies. In other words, it's fair to say that my daughter and her peers probably want Apple in their lives more than your median active manager does. But why is this the case? Why do so many active managers tend to underweight these high-performing growth companies?

One key reason is that the number of analysts covering mega cap companies is significantly greater than the number of analysts covering mid-cap companies. This can lead many active managers to believe, for instance, that establishing a differentiated market view on a mid-cap company is more exploitable than establishing a differentiated view on how Amazon will continue to hit its lofty growth targets. But it doesn't have to be this way because not all managers see it this way. We believe that the best managers are those that understand the idiosyncratic differences among mega cap companies—and overweight or underweight each company according to their specific investment philosophy and criteria.

The value of utilizing an active, multi-manager approach

As the largest market capitalization stocks within the U.S. equity market continue to climb, so too, in our opinion, does the importance of hiring best-in-breed managers who can identify key differences among mega cap companies. We believe that working with an investment solutions provider that utilizes a multi-manager approach is critical during times like these, as the right provider will be able to utilize multiple styles of active managers and combine them with robust internal capabilities. This makes for a more precisely managed exposure to mega cap companies. Importantly, this allows the provider to take overweight positions with companies that fit its sub-advisor investment criteria. Instead of simply avoiding mega cap companies altogether, like so many active managers tend to do.

So, to circle back to where we started, yes, my daughter and her peers would love Apple in their lives. But so, too, might some active managers. It all depends on who you hire.

Copyright © Russell Investments