by Brian Levitt, Global Market Strategist, Invesco

Key takeaways

Thinking about a recovery.While it doesn’t appear that a U.S. equity recovery has started yet, I believe it’s time to start thinking about how to position for one. |

Inflation watch.Inflation has a way to go before reaching the U.S. Federal Reserve’s “comfort zone.” But “better-than-expected” readings may be all the market needs to stage a recovery. |

What I’m thankful for.The U.S. midterm elections went off without much of a hitch. That’s just one of the things I’m grateful for this holiday season. |

Thinking about a recovery.

While it doesn’t appear that a U.S. equity recovery has started yet, I believe it’s time to start thinking about how to position for one.

What I’m thankful for.

The U.S. midterm elections went off without much of a hitch. That’s just one of the things I’m grateful for this holiday season.

A ‘keep it simple’ strategy

1) Where is the U.S. in the cycle?

The market indicators say recession.1 The hard economic data largely disagree.2 When in doubt, I go with the market. To that point, I expect the market to recover before the economy. In fact, stocks were positive during four of the last nine recessions.3

2) What’s the direction of the U.S. economy?

The economy is still in contraction, with leading indicators suggesting that growth is below trend and declining. The duration of the contraction will likely depend on what the Fed does next. A recovery could be forthcoming. Speaking of which…

3) What’s the expected policy response?

Typically, the Fed is easing by the time we are in the contraction phase of the cycle. That’s not yet the case. But, given the likely improvements in inflation, a pause could be forthcoming. The markets are pricing in a 5% terminal fed funds rate by March 2023.4 If that’s the case, then a recovery could be in the offing.

While it doesn’t appear that a recovery has started yet, we nonetheless believe it’s time to start thinking about how to position for a recovery. We would favour allocating toward riskier credit and the more cyclical and value-oriented parts of the equity market.

‘Tis the season

Even in a tough year — or maybe especially so — it’s worth identifying things for which we are thankful. Here’s my top 5 list, U.S. financial market edition.

- The U.S. stock market was up 49% from March 13, 2020 (the day the world essentially shut down for COVID) to Nov. 16, 2022.5 I would have absolutely signed up for that at the start of the pandemic.

- The U.S. 1-year inflation breakeven is well below 2.5%,6 which indicates the U.S. bond market believes inflation is set to decline rapidly.

- There appears to be little excess in the U.S. economy. Businesses do not appear to be over-levered,7 the banking system is well-capitalized,8 and U.S. households are still sitting on excess savings.9

- There is finally income to be had in fixed income.10

- The U.S. midterm elections went off without much of a hitch, as the losing candidates generally conceded. Rumours of American democracy’s demise may be overstated.

Stop me if I’ve told you this

Investors are likely tired of being told that missing the best days and months in the market can meaningfully erode returns. I suppose I’ll stop saying it when investors stop selling at inopportune times.

According to the Investment Company Institute, investors pulled $27 billion out of equity mutual funds and exchange-traded funds in September.11 No surprise then that October (+8.1%) was the 11th best month for the S&P 500 Index in 35 years!12 Not to be outdone, Nov. 10 (+5.5%) was the 15th best day for the index since 1957!13

Allow me to repeat myself: If you invested $100,000 in the S&P 500 Index in 1988 and left it alone, you would currently have over $3.2 million. Missing the top 1, 3, 5, and 10 months would have cut that total to $2.8 million, $2.3 million, $1.9 million, and $1.2 million, respectively.14

It may be confirmation bias, but …

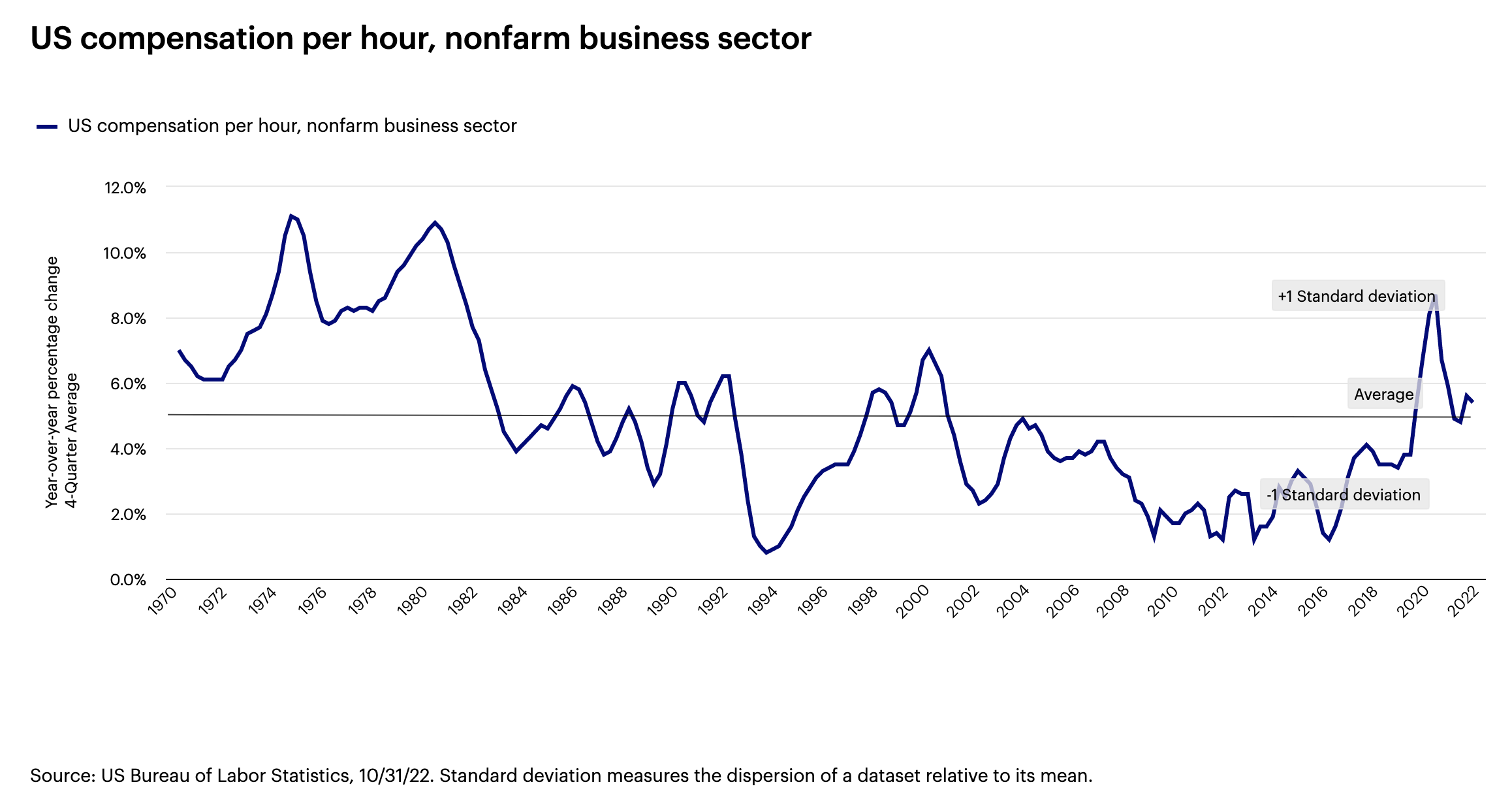

… we’re not experiencing the wage-price spirals of the 1970s. In fact, current compensation growth in the U.S. is now close to its long-term average.15

Since you asked

In short, it likely means that the Fed is tightening policy by too much. Short rates have been pushed higher, while the 10-year U.S. Treasury appears to be crying uncle, or more specifically signaling lower future nominal growth. The last time the yield curve was this inverted was in 1981. Yes, it portended a recession but also turned out to be a very attractive buying opportunity for equity and credit investors.

Song of the month

In response to October’s better-than-expected U.S. inflation reading, let’s go with Timber by Pitbull.

U.S. economic history suggests that high inflation tends to come down rapidly, which explains why “Timber!” has been on repeat in my mind this month. As the saying goes: “The bigger they are, the harder they fall.” Remember, markets likely won’t wait to recover until inflation is back in the perceived “comfort zone.” “Better-than-expected” may be all the market needs.

Phone a friend

I once again dialed Ashley Oerth, an investment strategist and Invesco’s resident crypto expert to help me to understand what is transpiring with the crypto exchanges and what the implications, if any, could be for the global financial system. Here’s what Ashley had to say:

Following the implosion of the FTX crypto exchange and its related businesses, questions are swirling over what contagion we may see in decentralized and traditional markets. In crypto, Bitcoin and Ethereum fell sharply along with other big-name cryptos, and crypto-linked trading firms and services are facing serious hardship; Alameda Research, a quantitative crypto-trading firm (also run by Sam Bankman-Fried) was wound down, and lending services BlockFi and Genesis have halted withdrawals, with possible bankruptcy in the cards. Complicating the situation is that there are currently more rumours than facts, which has only helped stoke concerns. Despite all this, this crisis appears so far to be contained within the crypto sphere, which remains largely unregulated, leveraged, and without any institutional backstops (such as a central bank) — all factors that help enable crises like we’ve seen with FTX and Terra Luna.

In the longer term, I suspect that these events may help further the distinction between cryptocurrencies, as embodied by coins and tokens, and the underlying use cases that are found in decentralized ledger technology, which is ultimately a new spin on database technology. Without meaningful, international, cooperative regulation, the crypto world will probably continue to be something of a wild west.

On the road again

My travels in early November took me to the City of Brotherly Love, a city electrified by their professional sports franchises. At the time, the Philadelphia Phillies were leading the World Series by two games to one. More than a few optimistic fans prepared me for what victory might mean — each time Philadelphia had won a World Series, the economy had fallen into recession (1929, 1930, 1980, 2008). Does their loss mean we’re now in the clear?

I was in Philly to speak at a conference for investment professionals, where I was on an agenda with Mike Quick, the former Philadelphia Eagles wide receiver. Quick told his story of what it took to rise from a small town in North Carolina to the heights of the National Football League. He also was sure to note that he is currently the radio announcer for the (then) undefeated Eagles. Quick was asked, “Who hit you the hardest?”

Me (thinking): I bet he gets asked this all the time.

Quick: “I get that question all the time.”

Me (thinking): I bet he’s going to say Lawrence Taylor.

Quick: “You all think I’m going to say LT. Well, it was my sister Linda.”

Me (thinking): That’s hilarious. I may be a lifelong Giants fan, but this guy is ok.

See you in December. I think most of us are ready to put 2022 to rest. Here’s to a less volatile and more fruitful 2023!

Footnotes

1 Source: Bloomberg, 11/18/22. Based on the shape of the U.S. Treasury yield curve (the difference between the 10-year U.S. Treasury rate and the 2-year U.S. Treasury rate) and the strength of the U.S. dollar versus a trade-weighted basket of currencies. The U.S. Dollar Index (USDX) indicates the general international value of the U.S. dollar by averaging the exchange rates between the U.S. dollar and major world currencies.

2 Sources: Bureau of Labor Statistics and U.S. Census Bureau, 10/31/22. Based on U.S. jobless claims and U.S. retail sales.

3 Source: Bloomberg, 9/22. Based on the S&P 500 Index and on recession dates defined by the National Bureau of Economic Research: Aug. 1957 – Apr. 1958, Apr. 1960 – Feb. 1961, Dec. 1969 – Nov. 1970, Nov. 1973 – Mar. 1975, Jan. 1980 – Jul. 1980, Jul. 1981 – Nov. 1982, Jul. 1990 – Mar. 1991, Mar. 2001 – Nov. 2001, Dec. 2007 – Jun. 2009 and Feb. 2020 – Apr. 2020.

4 Source: Bloomberg, 11/18/22. Based on Fed Funds Implied Futures. The terminal rate is the anticipated level that the federal funds rate will reach before the U.S. Federal Reserve stops its tightening policy. The federal funds rate (or fed funds rate) is the rate at which banks lend balances to each other overnight.

5 Source: Bloomberg, 11/16/22. As represented by the S&P 500 Index.

6 Source: Bloomberg, 11/18/22. The breakeven inflation rate is calculated by subtracting the yield of an inflation-protected bond from the yield of a nominal bond during the same period.

7 Source: U.S. Federal Reserve. Based on Nonfinancial corporate business: Debt to profits after tax

8 Source: U.S. Federal Reserve, 10/31/22. Based on the Tier 1 capital ratios of the nation’s banks. Tier 1 capital ratios compare a bank's equity capital with its total risk-weighted assets

9 Source: U.S. Federal Reserve, 10/31/22.

10 Source: Bloomberg, 11/18/22. Based on the yield to worst of the Bloomberg U.S. Corporate Bond Index. The Bloomberg U.S. Corporate Bond Index measures the investment grade, fixed-rate, taxable corporate bond market. It includes USD denominated securities publicly issued by U.S. and non-U.S. industrial, utility, and financial issuers. Yield to worst is the lowest potential yield an investor can receive on a bond without the issuer actually defaulting.

11 Source: Investment Company Institute, 10/31/22.

12 Source: Bloomberg, 11/16/22. As represented by the S&P 500 Index.

13 Source: Bloomberg, 11/16/22. As represented by the S&P 500 Index.

14 Source: Bloomberg, 11/16/22. The analysis is based on a hypothetical and is for illustrative purposes only. As represented by the S&P 500 Index.

15 Source: U.S. Bureau of Labor Statistics, 10/31/22.

Copyright © Invesco