by Christopher Hogbin, AllianceBernstein

Global stocks rose in the first quarter, but volatile trading patterns reminded investors that the road to normal will be bumpy. By carefully considering the risks that lie ahead, equity investors can prepare for the next phase of recovery from the pandemic.

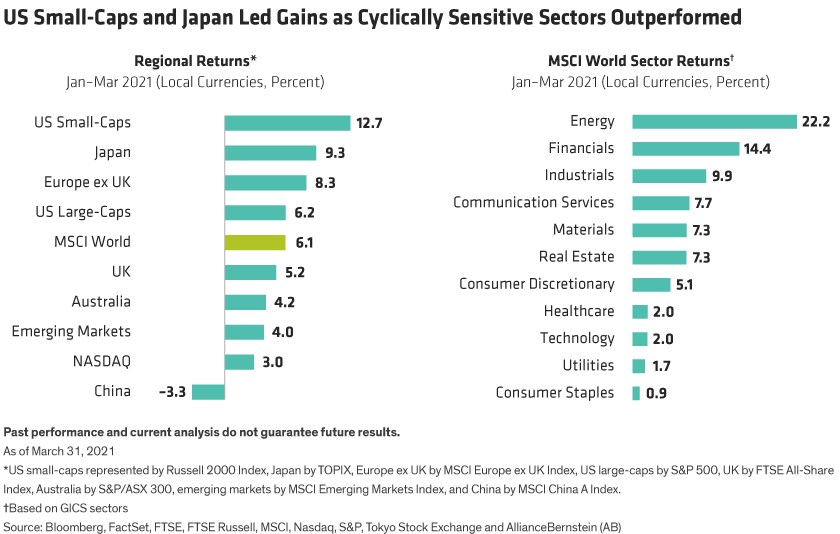

Investors are optimistic that the pandemic has passed a tipping point. During the first quarter, vaccine campaigns accelerated, deaths and infection rates receded from peaks in many countries and some economies began to reopen. Despite some setbacks, particularly in Europe, the MSCI World Index advanced by 6.1% in local currency terms (Display). Regions and sectors that tend to benefit from a cyclical recovery outperformed, including smaller-cap US equities, Japanese stocks, energy and financials. Defensive sectors such as utilities and consumer staples lagged.

Bumpy Underlying Trading Patterns

Solid market gains masked rapidly changing market conditions. While official interest rates remained at historic lows, the yield on the 10-Year US Treasury jumped by 89% to 1.74% by quarter-end amid increasing concerns of an inflationary outbreak fueled by massive fiscal stimulus and pent-up consumer demand. Value stocks, which are widely seen as more immediate beneficiaries of a stronger economic recovery, outperformed growth stocks by a wide margin, continuing a rebound that began last November (Display, left). Yet the equity style rotation wasn’t smooth, as investors gyrated daily between growth and value stocks (Display, right).

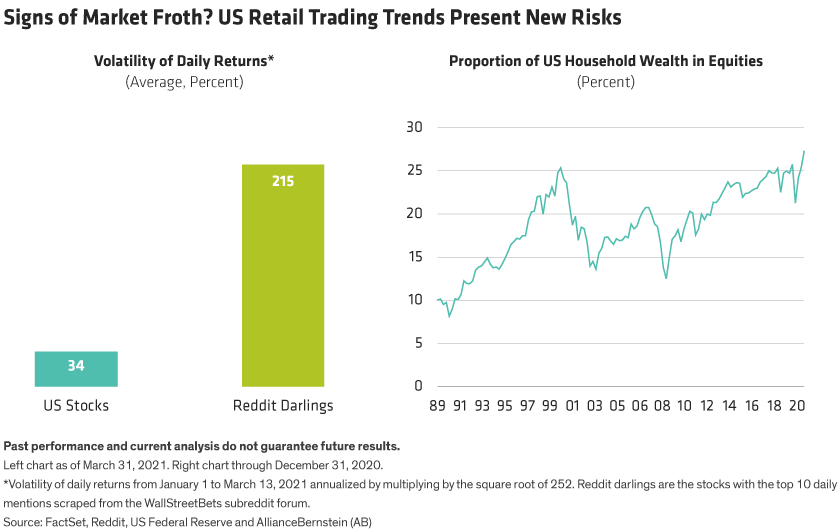

Volatility was also fueled by the growing role of retail investors, driven in part by massive fiscal stimulus. Reddit trading boards triggered wild trading in a group of stocks including GameStop and AMC Networks (Display, left). In the US, retail investors account for 20% of trading volume, up from 10% in 2016, according to Goldman Sachs trading data. At the start of the first quarter, US households held more than 27% of their wealth in equities—exceeding the peak of 25% during the 2000 technology bubble (Display, right).

Meanwhile, special purpose acquisition companies (SPACs)—or “blank check” companies—used to hasten the path to market for early-stage private companies, raised more money in the first quarter than in all of 2020. While SPACs aren’t necessarily unstable investment vehicles, their popularity further highlights speculative trends in the market today.

Three-Phase Recovery Still on Track

Does recent volatility threaten the recovery? We don’t think so. Our outlook still projects a three-phased recovery, each phase presenting distinct investment challenges. In early 2021, phase 1 began to unfold, with COVID-19 vaccinations picking up and governments cautiously weighing reopening efforts.

Phase 2 began in late February, amid the first successful efforts to contain the pandemic. Israel, the global leader in vaccines per capita, showed that immunized populations could allow economies to rapidly reopen without a coronavirus relapse. As this prospect becomes more likely worldwide, we expect companies to report strong earnings growth, especially given low comparable profits in 2020.

Such rapid growth will be hard to repeat next year. In phase 3, as the world begins to normalize, economic growth will probably face many of the same challenges that prevailed before the pandemic.

This recovery trajectory provides plenty of room for stocks to advance, in our view. However, first-quarter trading patterns reinforce the need to review the risks that will surface along the way.

Risk 1: Interest Rates and Inflation

For many investors, interest rates and inflation are major concerns. Rising Treasury yields have prompted questions about the potential of rising rates to derail stock market gains, particularly in the US. While the $1.9 trillion US stimulus package passed by President Biden’s administration in March—and a proposed $2 trillion infrastructure plan—provide crucial support for the economy, they could also revive inflation.

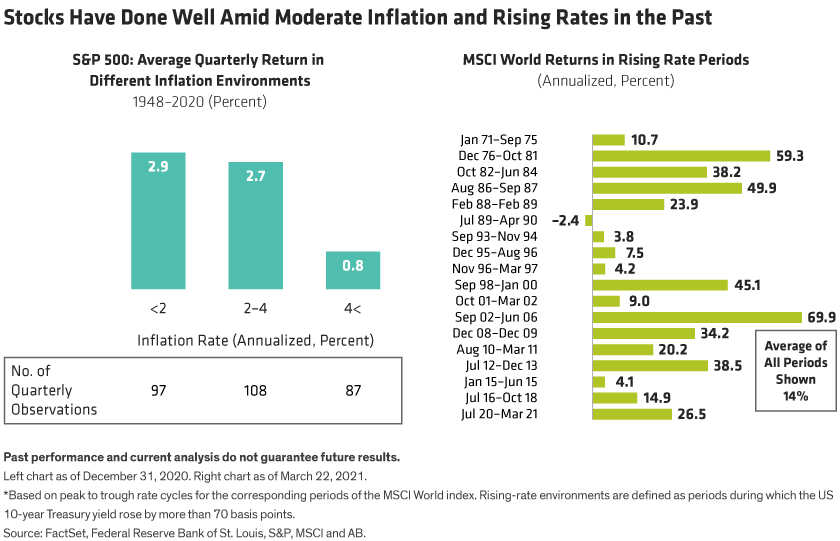

Are inflation and rising interest rates bad for stocks? Not necessarily. Our research suggests that since 1948, US stocks posted average quarterly returns of 2.7% when inflation was between 2% and 4% (Display, left). Returns only fell below 1% when inflation exceeded 4%, which is well beyond current five-year forward US inflation expectations of about 2.1%.

Similarly, stocks have done well when interest rates rose (Display above, right). Over 18 periods of rising US Treasury yields since 1971, global stocks gained an average of 14% a year, according to our research. Rising rates don’t typically hurt stock returns as they usually accompany an acceleration of economic growth and corporate earnings.

To be sure, investors should prepare for inflation. Portfolio managers should check that their holdings are positioned for inflation; for example, companies with pricing power have an advantage in an inflationary environment. Make sure equity allocations are diversified across stocks that may respond differently to a return of moderate inflation and higher interest rates. And consider allocating to real assets, such as real estate or commodities, which tend to perform well when inflation rises.

Risk 2: The Swinging Style Pendulum

Interest rates do, of course, have a profound effect on different types of stocks. Rising rates increase the discount rate that investors use for valuing equities. This suppresses price/earnings multiples, particularly for growth stocks, which tend to have cash flows and earnings in the more distant future. Value stocks often perform better when rates rise.

This may explain the sharp style swings in the first quarter as investors began to digest how different stocks would perform in the changing environment. Valuations of hypergrowth stocks with especially inflated multiples fell back to earth while value stocks outperformed.

The recent rate and style volatility have provided a real-world test of portfolio sensitivity to rising rates. For investors with large allocations to growth and underweights to value, it may be time to reassess. Even after recent gains, global value stocks traded at a 51% discount to growth stocks at the end of February, following several years of extreme underperformance. As a result, we think value stocks still have recovery potential. For growth stocks, it’s important to verify that holdings have solid business drivers and resilient cash flows to support sustainable returns if multiples come under pressure.

Stocks in the middle—such as lower-volatility stocks—were shunned throughout the pandemic. Many defensive sectors, such as consumer staples and utilities, trade at attractive valuations and could help provide a cushion for volatility. Indeed, amid nervous trading in late March, there were signs that these lower-beta stocks might again be playing their traditional risk-reduction role.

Risk 3: Market Behavior Risks: From US Retail Investors to Hedge Funds

More instability could result from trading trends seen during the quarter. In particular, the Reddit darlings episode reflects a sharp increase in retail trading of US stocks, facilitated by popular trading apps and an increase in spare cash driven by the US stimulus program.

These trends won’t disappear, especially with more stimulus checks heading to US citizens. Portfolio managers can monitor unusual retail trading activity by scraping big data from popular trading boards, which can provide an early warning signal for a potential single-stock frenzy. We don’t think these trends present a systemic risk to US markets. However, with US households holding much more of their wealth in equities, as shown above, they’re more exposed to a potential market correction.

At quarter-end, share prices of several US media stocks and Chinese ADRs plunged amid immense selling pressure—despite no change to their earnings. Archegos Capital Management, a US-based hedge fund, is believed to have prompted the sell-off after suffering massive losses from equity derivatives trades.

These types of market volatility can create opportunities for active managers. Indeed, markets with a high proportion of retail investors—such as the China A Shares market—tend to be prone to swings in sentiment. This often leads to inefficiencies that can be exploited by active, long-term investors, who identify stocks with valuations that have become disconnected from fundamentals.

Risk 4: Return to the New Normal

Many companies’ fundamentals were impaired by the pandemic. When economic shutdowns began, business visibility disappeared, particularly in hard-hit industries.

As economies reopen, many questions remain unanswered. How will consumers and businesses recalibrate spending for the new normal? Will some industries face oversupply, for example, of aircraft, hotel rooms or office space? If rates rise, will debt-laden companies face financing risks? How will extraordinary fiscal policy deployed to bring economies back to normal affect different companies? And what about geopolitical risk—which dropped off radar screens last year but may become more prominent post-pandemic?

There aren’t simple answers. But these questions all point to the importance of highly selective stockpicking through the recovery.

To understand how companies are positioned for the new normal requires independent research of their businesses. Demand must be assessed in real time, using new data analysis techniques to determine which companies have adjusted well from crisis to recovery. Financing risk warrants thorough scrutiny of balance sheets to identify companies that didn’t prudently manage their debt amid low interest rates. In the US, higher corporate taxes could push down future earnings, though some companies will enjoy a fiscal windfall from Biden’s infrastructure plan. Political risk is hard to predict; for example, we still don’t have a good idea of the Biden administration’s trade policy plans. But company exposures to specific political risks can be pinpointed to help ensure that a portfolio isn’t too vulnerable to some of the biggest hazards.

Steering Through Sentiment to Sustainable Returns

Perhaps the biggest overriding risk that surfaced in early 2021 is the power of a sentiment-driven market. Intense sentiment can seduce investors to forget about fundamentals. Piling into a single group of stocks that is suddenly breaking out can be tempting, but it isn’t a recipe for long-term investing success.

Positioning for the recovery requires rising above headline noise. With a clear framing of the risks, investors can develop high conviction in the companies that are best placed to overcome hurdles and deliver long-term investment returns as the world economy and markets get back to business as usual.

Christopher Hogbin is Head of Equities at AllianceBernstein (AB).

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams and are subject to revision over time.

MSCI makes no express or implied warranties or representations and shall have no liability whatsoever with respect to any MSCI data contained herein. The MSCI data may not be further redistributed or used as a basis for other indices or any securities or financial products. This report is not approved, reviewed or produced by MSCI.

This post was first published at the official blog of AllianceBernstein..