by Masahiko Loo, AllianceBernstein

Yoshihide Suga assumed the mantle of Japanese prime minister in September. While the political message is continuity from Shinzō Abe’s administration, there are underlying hopes for a resurgent Japan. Can Suganomics offer stability while rebooting Abenomics and the Japanese economy?

Who Is Suga?

Known as a fixer, Prime Minister Suga was Abe’s longest-tenured chief cabinet secretary and right-hand man. Suga has a reputation for efficiency and deregulation—a positive for an economy that needs structural reform. During his time in government he has already lowered mobile phone prices once, overhauled the inbound tourist visa process and implemented a hometown tax rebate program.

Suga inherited Abe’s Liberal Democratic Party (LDP) presidential seat and parliamentary term, which expire in September and October 2021, respectively. Because of this, there are concerns that Suga may be perceived as a caretaker PM. While we believe there is clear incentive for Suga to call snap elections before next October to consolidate political power, he would do so without the political base of his predecessor. Unlike Abe, who was part of a political dynasty, Suga comes from humble beginnings—his parents were strawberry farmers.

Political continuity and consistency have been and will continue to be important for Japanese markets. Prior to Abe’s record tenure of just over seven and a half years, the prime minister’s office had a revolving door—the average PM lasted only 382 days—and the instability proved difficult for Japan’s economy and markets. Suga runs the risk of becoming the eighth PM since 2000 to last less than 500 days in office.

The Legacy of Abenomics

The three arrows of Abenomics—monetary easing, flexible fiscal policy and structural reform—have had varied levels of success. A couple of them worked, until they didn’t.

While Japan no longer suffers from deflation, thanks to quantitative easing, no one would call Abe’s average core inflation rate of 0.68% a roaring success. Fiscal stimulus initially increased economic growth, but two consumption tax hikes dampened sentiment, eventually muted growth and then COVID-19 amplified deficits. And structural reform started on the back burner but eventually came down to mildly effective labor market reform designed to increase women in the workplace and a free childcare policy designed to boost birthrates.

Still, Abe accomplished some major milestones: successful trade negotiations with the European Union as well as the Trans-Pacific Partnership, reigniting the Japanese stock market while devaluing the yen and simultaneously increasing GDP.

One of Abe’s most meaningful moves was to overhaul the gargantuan but staid Government Pension Investment Fund (GPIF). The result was a change from ultraconservative investments with a hyperfocus on safety and Japan-based assets to a modern allocation that includes approximately 50% global stocks and bonds—and better potential returns.

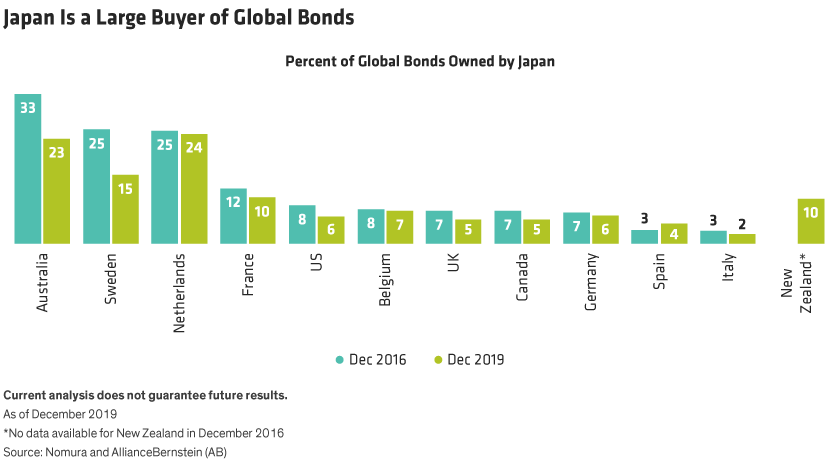

This move has not only allowed the $1.6 trillion (169 trillion yen) GPIF to access higher global yields, but along with other Japanese pensions, financial institutions and retail investors, it has made Japan one of the largest buyers of global assets. By December 2016, for example, Japan was the single largest investor in Australian government bonds, holding a full third of all Aussie bonds outstanding and making Japan an important investor in markets worldwide (Display).

As long as growth and yields remain low in Japan, we expect Japanese investors will likely remain significant buyers of any international credit weakness or stock market dips for years to come.

Turning Abenomics into Suganomics

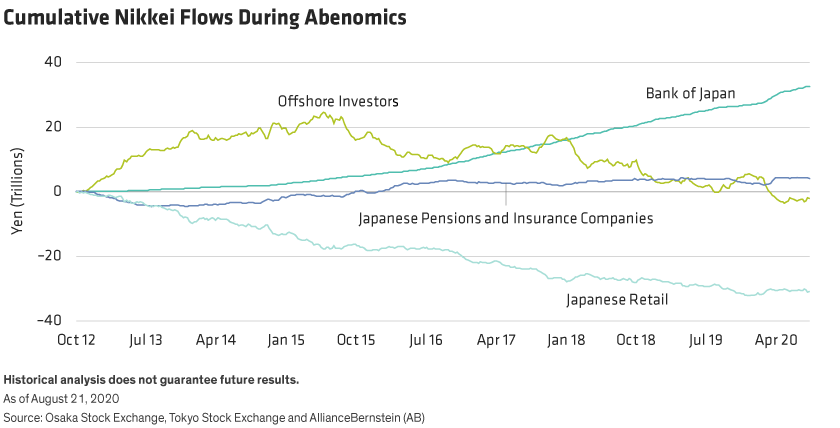

Unfortunately for Suga, most of the heavy lifting of Abenomics with large macro implications has already taken place. The yen is no longer overvalued or limiting economic growth. The stock market has been revived, albeit via a recovery that was heavily influenced by Bank of Japan exchange-traded funds purchases (Display). And there’s little chance of strong capital flows into Japanese assets, as most investor groups are already neutrally positioned and would be looking for macro improvement before further investment.

So Suga’s present challenge is to continue what’s left of Abenomics with his own twist—and to hopefully create quick, small victories while doing it.

Suga’s first policy move as PM was to instruct the communications minister to work toward lowering mobile phone costs yet again. We think this is emblematic of Suga’s approach—small changes that may feel good but don’t move mountains.

Suga is also expected to go for an early win with a new digital agency to haul Japan’s antiquated government services into the 21st century. Long revered for its technology development, Japan’s internal politics have thus far kept it from successfully harnessing technology for its own use. The pandemic highlighted government inefficiencies, including delayed stimulus payments and the difficulty of collecting coronavirus data via fax. Digital efficiencies could bring economic benefits in the form of saved time and costs, as well as increased technology sales.

However, while Suga has a reputation as a fixer, we believe a digital agency that would effectively dismantle the silos of ministries might be a bigger political bite than Suga can chew, and certainly more than can be accomplished prior to the next election. If successful, it might also have the unintended and unwelcomed consequence of putting people out of work.

Another issue Suga may have to address is regional banks struggling with low rates and tepid loan demand due to local depopulation. In an ultra-low-yield environment, efficiency and strong lending standards are imperatives for banks. Unfortunately, neither of those are currently hallmarks for Japanese regional banks, most of which still rely on passbooks and stamps. A slate of bank reorganizations and consolidations would undoubtedly lead to branch closures and lost jobs, doing little to endear Suga’s LDP to voters.

However, should voters grant him a longer term, other items on Suga’s to-do list include dismantling ministry silos and reducing government bureaucracy, further labor market reform, reshoring supply chains and spurring economic competition in small and medium enterprises—all designed to make Japan more competitive and drive economic growth.

Suga isn’t as charming as his predecessor and is not as gifted at foreign policy, but he is famous for his work effort and dedication to accomplishing things for Japan. We expect that Suganomics, for however long it lasts, will be an accumulation of small successes. But until there are real improvements in Japan’s macroeconomy, we believe Japanese investors will continue to seek yields and returns elsewhere.

Should Suganomics not deliver results, the revolving door of the prime minister’s office may start to swing again. Investors should brace themselves for the impact of changing policies and priorities if Suganomics fails to sweeten the Japanese economy.

Masahiko Loo is Portfolio Manager—Japan Multi-Sector Fixed Income at AB.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams. Views are subject to change over time.

This post was first published at the official blog of AllianceBernstein..