by Collin Martin, CFA, Fixed Income Strategist, Schwab Center for Financial Research

Key Points

- High-yield bonds offer some of the highest yields and income potential of all fixed income investments.

- High-yield defaults are occurring at the fastest pace since 2009, and we believe the trend will continue.

- We suggest investors focus on “higher-rated” high-yield bonds, and limiting exposure to bonds rated “CCC,” as they are the most likely to default.

With average yields close to 6%, high-yield bonds can offer investors an opportunity to earn more income in a very low-interest-rate world. That’s a benefit not many fixed income investments can provide.

Those higher yields come with greater risks, however, and despite the strong performance recently, we believe investors should approach the market carefully because risks remain elevated. High-yield corporate bonds are defaulting at the fastest pace since the 2008-2009 financial crisis, and we expect the number of defaults to continue to climb. While the economic rebound from the lows earlier this year is a positive, many high-yield issuers were already struggling before the pandemic hit.

Meanwhile, support from the Federal Reserve is primarily focused on investment-grade corporate bonds, not high-yield corporate bonds. If the economic outlook were to deteriorate or the stock market were to fall further, it could be a bumpy ride for high-yield bonds.

Despite those risks, investors can still consider high-yield bonds as a complement to a well-diversified bond portfolio, but we do not suggest an overweight allocation. We suggest investors limit any high-yield allocation to no more than 20% of the overall portfolio. Those interested in high-yield corporate bonds should consider an “up-in-quality” tilt, focusing on bonds (or funds that hold bonds) whose ratings are in the upper rungs of the high-yield universe, like those rated “BB.”

The search for yield

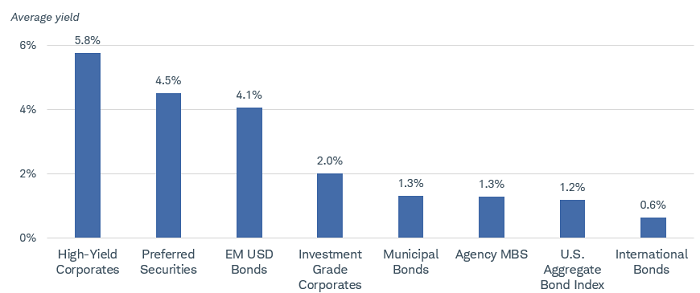

With yields low across the globe, it’s no surprise that some investors are looking anywhere and everywhere for investments that can offer higher yields and income payments. High-yield bonds certainly fit that bill, as their average yields are higher than any other fixed income investment we track.

No surprise: High-yield bonds offer higher yields

Source: Bloomberg, as of 9/30/2020. Yield represents average yield-to-worst for all investments, except preferred securities which represents yield-to-maturity. Yield to worst is a measure of the lowest possible yield that can be received on a bond that fully operates within the terms of its contract without defaulting. Indexes representing the investment types are: High-Yield Corporates = Bloomberg Barclays U.S. Corporate High-Yield Bond Index; Preferred Securities = ICE BofA Fixed Rate Preferred Securities Index; EM USD Bonds = Bloomberg Barclays Emerging Market USD Aggregate Bond Index; Investment Grade Corporates = Bloomberg Barclays U.S. Corporate Bond Index; Municipal Bonds = Bloomberg Barclays Municipal Bond Index; Agency MBS = Bloomberg Barclays U.S. MBS Index; U.S. Aggregate Bond Index = Bloomberg Barclays U.S. Aggregate Bond Index; International Bonds = Bloomberg Barclays Global Aggregate ex-US Bond Index. Past performance is no guarantee of future results.

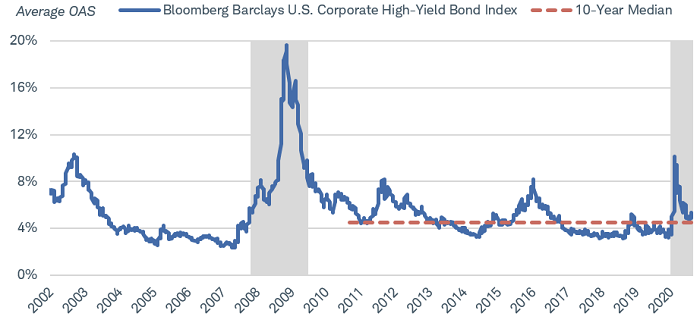

This chart doesn’t tell the whole story, however. We prefer to look at relative yields—in other words, how much additional yield investors can earn above and beyond a comparable Treasury security. The additional yield is called a credit spread.

Credit spreads have fallen sharply from the March highs. After hitting a peak of 11% on March 23rd, the average option-adjusted spread of the Bloomberg Barclays U.S. Corporate High-Yield Bond Index was down to 5.2% at the end of September. The good news is that it’s still above the 10-year median spread of 4.5%. The bad news is that we believe risks are still high and price declines are possible.

High-yield spreads are slightly higher than the 10-year median

Source: Bloomberg, using weekly data as of 9/30/2020. Shaded areas represent recessions. Option-adjusted spreads (OAS) are quoted as a fixed spread, or differential, over U.S. Treasury issues. OAS is a method used in calculating the relative value of a fixed income security containing an embedded option, such as a borrower's option to prepay a loan.

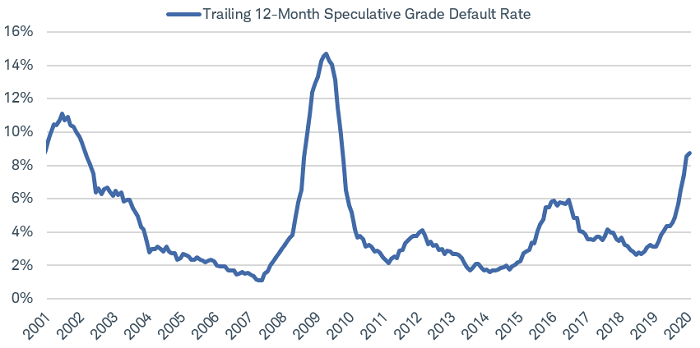

Corporate defaults are on the rise

We believe the biggest risk to the high-yield corporate bond market today is the risk of default. Lost in the headlines of the ongoing economic recovery and stock price gains since the March lows is the fact that high-yield bonds are defaulting at their fastest pace since the 2008-2009 financial crisis.

According to the Moody’s Investors Service, the trailing 12-month speculative-grade default rate rose to 8.7% in August, more than double the rate from just one year ago.1 When we discuss default rates, we are strictly discussing the rate for high-yield bonds that have defaulted, not the entire corporate bond universe. It’s rare for an investment-grade-rated bond to default, because by the time a default occurs the rating agencies usually have already downgraded it to junk.

The high-yield default rate is at its highest level in years

Source: Moody’s, “Default Trends – Global August 2020 Monthly Default Report,” September 9, 2020.

Corporate defaults appear likely to continue to rise. Moody’s expects the rate to reach 12% by next February, while S&P forecasts a rate of 12.5% by June 2021.2 We believe that the pandemic is simply pulling forward many corporate defaults that may have happened anyway, albeit at a later date. Energy companies have been under pressure for years and the low price of oil makes it more challenging for highly leveraged oil producers to stay afloat. The “death of retail” also has been a story line for years—with so much commerce taking place through the internet, many retailers with large physical presences were already struggling. Unfortunately, the pandemic exacerbated the situation.

Given the risk of defaults continuing to rise, we suggest investors focus on higher-rated high-yield bonds. That may sound like an oxymoron, but we mean bonds that are in the higher rungs of the “junk” bond rating scale, like those rated “BB.”

Generally speaking, bonds with the lowest ratings are those that are most likely to default. As a result, corporate bonds with ratings in the “CCC” area should be the most vulnerable. Avoiding these types of bonds might help limit some of the downside if the economic outlook deteriorates.

Finally, the Federal Reserve’s credit facilities can buy only a very limited number of high-yield bonds—only those that had been downgraded to junk after March 22, 2020, and still maintain ratings of “BB.”

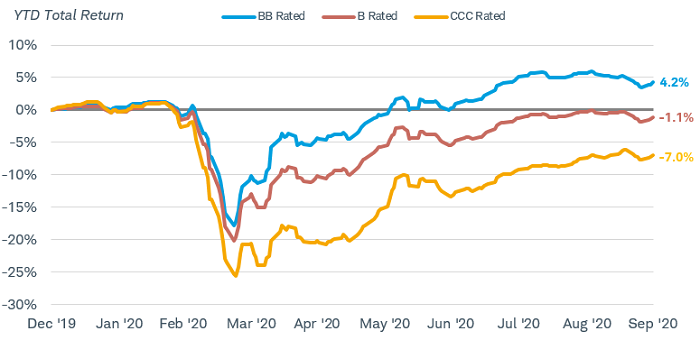

Staying up in quality has generally paid off this year, with high-yield bonds with the highest ratings outperforming those with lower ratings. In fact, as the chart below illustrates, total returns for the “B” and “CCC” rated sub-indexes are still negative through the first three quarters.

Higher-rated high yield has outperformed the lower-rated parts of the market this year

Source: Bloomberg. Cumulative total returns from 12/31/2019 through 9/30/2020. Returns assume reinvestment of interest and capital gains. Indices represented are the “BB”, “B”, and “CCC” sub-indexes of the Bloomberg Barclays U.S. Corporate High-Yield Bond Index. Past performance is no guarantee of future results.

While the high-yield market has rebounded from the pandemic-driven lows, the steep drop in February and March should give more conservative investors pause. Even the “BB” rated sub-index suffered a drop of more than 15% in just a few weeks’ time. This highlights the risky and volatile nature of high-yield bonds, and helps explain why they should be used as a complement for high-quality fixed income investments, not a substitute.

What to do now

Consider high-yield bonds if you can handle heightened volatility—it could be a bumpy ride going forward. We do suggest investors consider an up-in-quality tilt, focusing on bonds with “BB” ratings.

- If you invest using individual bonds, don’t just screen for the highest yielding bond. Rather, simply search for those bonds with ratings in the “BB” area. While it might be tempting to consider a bond with a low price and a maturity not too far in the future, “hoping” the issuer can just make it to the maturity date, that’s a risky strategy. A very low price implies the risk of default is high, and that comes with its own set of headaches. Yields on “BB” rated bonds are likely well below bonds with ratings of “B” or “CCC,” but the likelihood of repayment is also higher.

- If you invest through bond funds, we suggest an active approach. With an active high-yield bond mutual fund or exchange-traded fund (ETF), the fund manager can at least make the decision of what to hold, or perhaps more importantly, what not to own. A passive, index-tracking approach might have more exposure to the lowest-rated parts of the market, meaning those bonds that might be most likely to default. When examining bond mutual funds or ETFs, we prefer funds that have a greater allocation to “BB” rated bonds than the overall index does.

1 Source: Moody’s Investor Services, “Default Trends – Global, August 2020 Default Report,” September 9, 2020

2 Source: Moody’s Investor Services, “Default Trends – Global, August 2020 Default Report,” September 9, 2020 and S&P Global Ratings, “Corporate Defaults Slowed in August,” September 3, 2020.