by Matt Sheridan, Portfolio Manager – Global Multi-Sector, AllianceBernstein

Credit barbell strategies are designed to provide protection on the downside, participation on the upside, and efficient income. But with government bond yields at historic lows, can these fixed-income strategies still meet their objectives? We think so.

Credit barbells combine interest-rate-sensitive assets with credit assets in a single portfolio. This approach can help managers get a handle on the interplay between interest-rate risk and credit risk and make better decisions about which way to lean as conditions change.

Credit barbell strategies are effective because they blend asset classes whose returns are negatively correlated. Risk-mitigating assets, such as US Treasuries, tend to do well when growth slows, while return-seeking assets, such as high-yield corporates, shine when growth accelerates and interest rates rise.

In this way, strong returns on one side of the barbell can help offset weakness on the other. This was the case when the capital markets sold off sharply in March. While returns for some income-generating assets—such as emerging-market debt and securitized assets—were down by more than 20%, the Bloomberg Barclays US Intermediate Treasury Index enjoyed a flight to safety that boosted monthly returns above 5%. In credit barbells, Treasury positions helped mitigate the broader market drawdown.

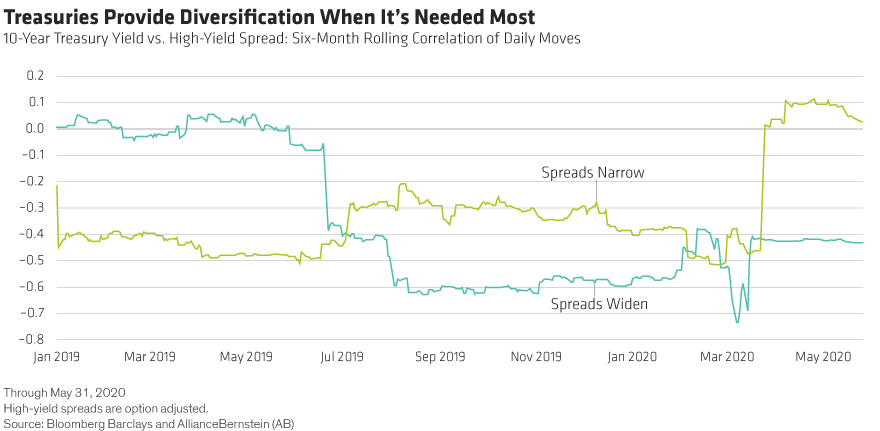

Negative Correlation Still Key to Downside Protection

But what of fears that the relationship between risk-mitigating and return-seeking assets has broken down under the extreme stress of the pandemic? That would be concerning. If the correlation between Treasuries and high yield has turned positive, that could limit the downside-protection benefits of a barbell.

To address this concern, we’ve given recent correlations a closer look. In Display 1, we divided correlation data between the 10-year US Treasury yield and high-yield spreads into days when spreads narrowed (a risk-on environment) and days when spreads widened (a risk-off environment) over rolling six-month periods.

In risk-on environments, correlations indeed increased. When high yield performed well, so too did Treasuries. This makes sense because the US Federal Reserve and other central banks have pledged to keep rates low and have instituted numerous programs to boost investor confidence and return liquidity to the system. These actions have been helpful across the risk spectrum.

But critically, when high-yield spreads widened and risk assets declined, correlations between Treasuries and high yield remained negative. In other words, government bonds continued to be an offset to risk assets when protection was needed most, allowing credit barbells to mitigate the downturn.

Low Yields Don’t Unhinge a Barbell Strategy

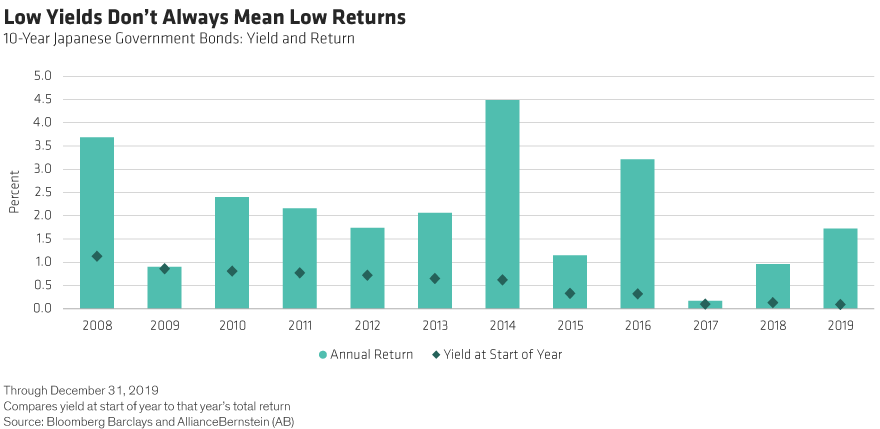

Despite reassurance about negative correlations, some investors worry that today’s low, low yields will limit downside protection going forward. They’re concerned that, with central banks anchoring rates at historic lows, government bonds will have less room to rally during risk-off periods—and that returns will be commensurately curtailed. This fear is especially prevalent in the US, where 10-year Treasury yields below 1% are new territory.

Historical experience outside of the US, however, shows that low yields do not necessarily translate into low returns. Japan has a long history of extremely low yields (Display 2). For 11 of the last 12 years, the yield on the 10-year Japanese government bond was less than 1%. Meanwhile, annual returns over the same period averaged more than twice as much and, in fact, rarely matched starting yield levels.

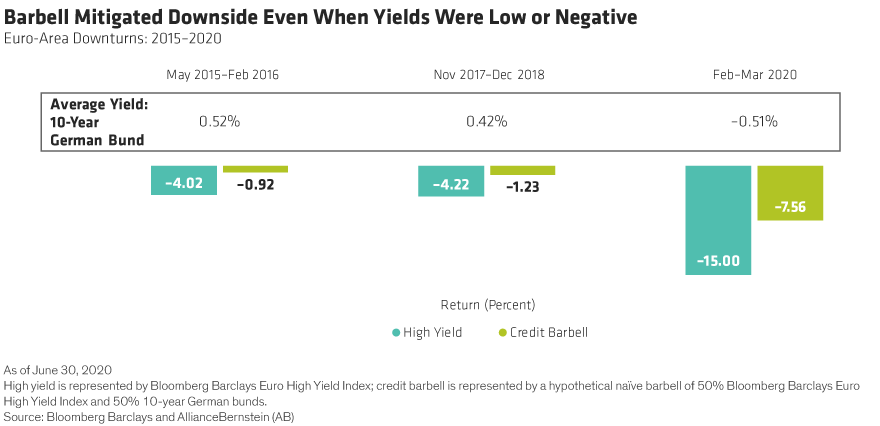

This dynamic has allowed credit barbells to provide downside protection during periods of both high market stress and low or negative yields. Take, for example, a barbell between German bunds and euro high yield (Display 3).

During the periods shown above, when high-yield spreads widened meaningfully, government bond yields were at or below half a percent. Yet in every case, a barbell between government and high-yield bonds significantly muted the credit downdraft.

Even when German bund yields were negative, as in the most recent downturn, government bonds proved an adequate buffer and led to meaningfully higher returns for a barbell strategy compared with risk assets alone.

The Path to Efficient Income

Despite the advantages to holding government bonds as a buffer, some income investors may be tempted to simply forgo exposure to rate risk in today’s low-yield environment. In this case, the most likely alternative to a credit barbell strategy is an investment-grade corporate portfolio.

At first glance, a corporate portfolio seems like a reasonable option. We can construct a US investment-grade corporate portfolio that has roughly the same average quality as a simply constructed credit barbell comprising 50% US Treasuries and 50% US high yield (excluding debt rated CCC). The two hypothetical portfolios would have an average quality of A–/BBB+ and also have similar durations and historical volatility.

But there the similarities end. When we compare the average yield on the investment-grade corporate portfolio (2.2% as of early June) to the average yield on the naïve credit barbell (3.4%), we see that the barbell supplies meaningfully higher income—and income would be higher still if we were to diversify across higher-yielding sectors.

Beyond a Static Barbell

The credit barbell story doesn’t end here. Active management can increase income still further as well as potentially enhance downside protection and/or upside participation.

Managers can and should go beyond a naïvely constructed, fixed barbell—diversifying their credit exposure across higher-yielding sectors, capitalizing on relationships along the yield curve, and tilting the structure toward rates or toward credit, depending on the market environment. Here are some approaches to consider today:

Actively manage interest-rate risk. As we’ve argued above, it’s important to hold duration during stressed market environments, even when yields are low. But where you take that interest-rate risk is also important. For example, the intermediate range of the US Treasury yield curve is relatively attractive today. Because it’s steeper, it provides both more generous yield and a price bump as bonds “roll” down the curve toward maturity.

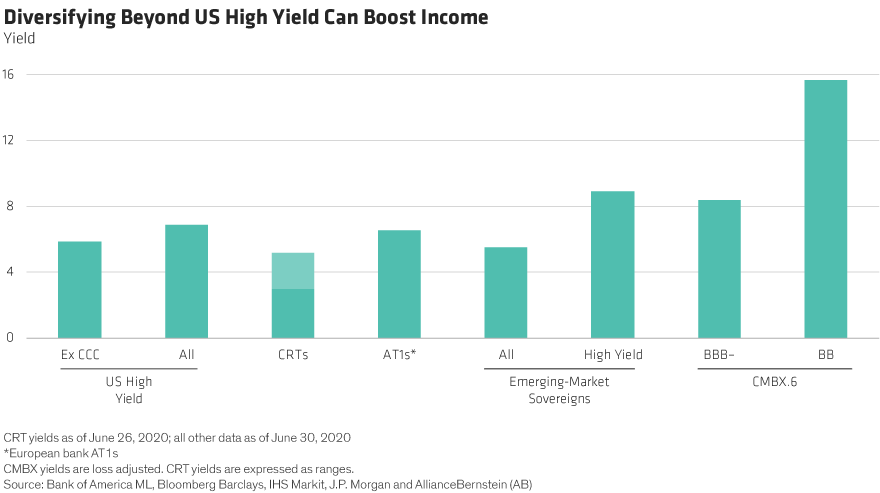

Diversify beyond US high-yield corporates. On the credit end of the barbell, consider diversifying across sectors to enhance income and potential return. This approach takes advantage of differing correlations among sectors and capitalizes on relative value opportunity.

For example, today we see opportunities—and compelling yield (Display 4)—in select BBB-rated corporates; subordinated (AT1) European bank debt; securitized assets, such as credit risk–transfer securities; sovereign emerging-market debt; and even fallen angels.

Lastly, avoid concentrating in any single issuer or bond, given today’s uncertain environment. And be selective; fundamentals matter.

Far from being broken, credit barbell strategies can meet their objectives—downside protection, upside participation and efficient income—in volatile, low-yield environments. Indeed, for income investors looking to navigate today’s challenging markets, credit barbells will continue to serve an important role in asset allocations.

Matt Sheridan is Portfolio Manager—Global Multi-Sector, and Monika Carlson is Senior Investment Strategist—Fixed Income at AB.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams. Views are subject to change over time.

This post was first published at the official blog of AllianceBernstein..