by Shamaila Khan, Director, EM Debt, AllianceBernstein

As the coronavirus crisis unfolded, prices tumbled and yields spiked to record highs across investment-grade emerging-market debt (EMD)—a sector widely considered to have healthy credit fundamentals and a low risk of defaults.

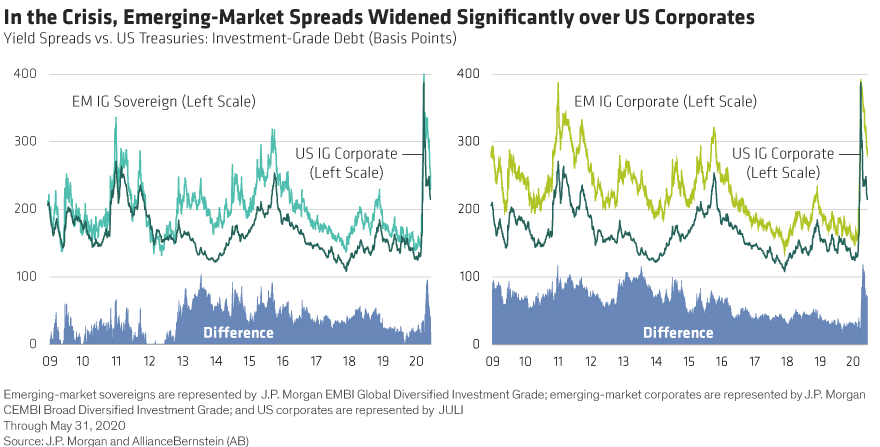

Yield Gap Widens with US Corporates

Over the past decade, the difference in yields between investment-grade EMD and investment-grade US corporates had narrowed steadily, reflecting converging average credit quality. Then came COVID-19.

The pandemic triggered massive market declines as investors rushed to free up cash. Indiscriminate selling hit some of the highest-quality sectors of the market, including investment-grade EMD. Spreads over US Treasuries climbed sharply as prices fell.

The investment-grade EMD sector has rallied in the two months since then. But today’s spreads remain wide, particularly in investment-grade emerging-market (EM) corporates, both by historical measures and compared with spreads on US investment-grade corporates (Display 1).

Why the sudden yawning gap between these sectors?

Rather than deteriorating fundamentals, the wider spread between EMD and US corporates reflects a sizable—but short-term—technical factor. In the early stages of the market drawdown, investment-grade EM corporates and US investment-grade corporates performed in line with one another.

But when the US Federal Reserve announced expanded purchase facilities for US corporate bonds, the recovery in US credit accelerated, leaving investment-grade EMD trailing behind. While investment-grade EM sovereigns have recovered on a relative basis, investment-grade EM corporates still have room to recover, as the effect was even more pronounced for EM corporates than for EM sovereigns.

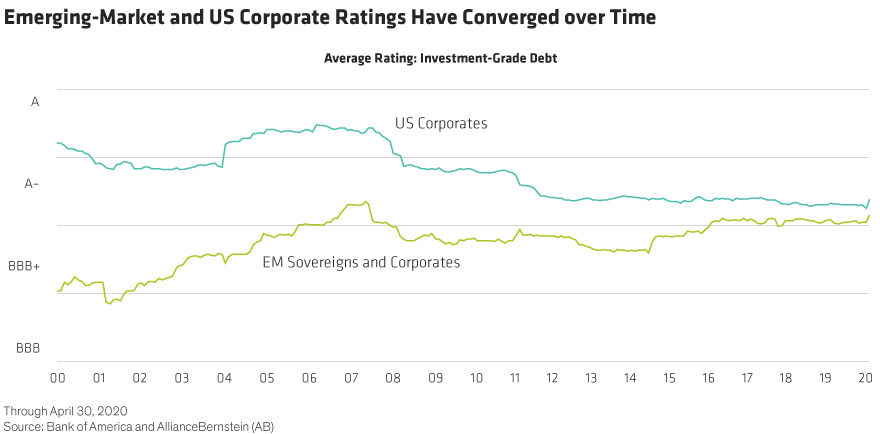

Investment-Grade EMD Boasts Stronger Fundamentals

We expect the yield differential between investment-grade EMD and US corporates to continue to shrink over time as the recovery progresses. That’s because, in the long run, credit fundamentals matter most to bond returns. And investment-grade EMD’s credit fundamentals are strong and improving.

In fact, over the past two decades, while the average credit quality of US investment-grade corporates has declined, the average rating of investment-grade EMD has risen. As a result, investment-grade EMD has virtually closed the ratings gap with US investment-grade corporates (Display 2).

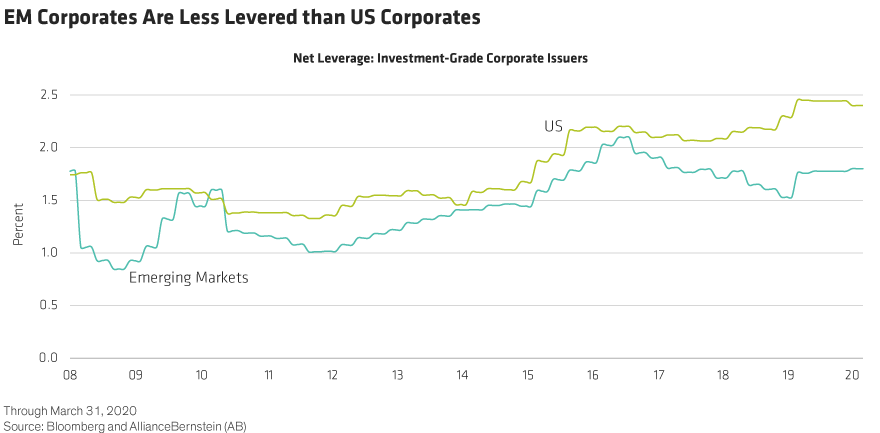

Among the most critical fundamental factors are the financial metrics of the issuers. US investment-grade corporates have become more highly leveraged in recent years (Display 3) as low interest rates have helped finance corporate share buybacks and enabled more aggressive balance-sheet management.

This has left the US investment-grade corporate sector with a higher-than-usual share of BBB-rated debt and significantly increased the risk of fallen angels—bonds downgraded to below-investment-grade ratings.

In contrast, investment-grade EM corporates have overall lower net leverage and a lower risk of fallen angels. Furthermore, our expectations for EM fallen angels have not grown materially as a result of the crisis, thanks to the sector’s strong fundamentals.

EM corporate issuers also have more cash on hand relative to their overall debt than do US corporate issuers (Display 4). This helps them withstand periods of volatility during periods when market access is limited and liquidity is critical. It also means issuers won’t be under pressure to take on new debt unless they can afford it.

Though the oil-price crash at the beginning of March has had a short-term impact on investment-grade EM energy-exporting sovereigns, it has not meaningfully affected credit fundamentals. Over the past few years, these countries have grown external buffers, including sovereign wealth funds and central bank reserves, that are now many times larger than the gross government debt they’ve accumulated. As a result of these ample cushions, the credit ratings of oil producers have held steady despite record-low oil prices.

Yet EMD spreads remain wider than normal. To us, this disconnect between fundamentals and valuations signals opportunity. For investment-grade credit investors, it may be time to tilt away from US investment-grade corporates toward investment-grade EMD. And for any investor giving EMD a closer look, this could be an attractive entry point.

Shamaila Khan is Director of Emerging-Market Debt at AB.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams. Views are subject to change over time.

This post was first published at the official blog of AllianceBernstein..