by Jason Xavier, Franklin Templeton Investments

Many investors associate exchange-traded funds (ETFs) with passive styles of investing. But that isn’t always the case—today, there are a range of different types of ETFs available in the marketplace beyond the traditional passive, capitalisation-weighted funds that first came on the scene.

As an asset manager offering a range of ETFs—from passive to smart beta to active—we see it as our responsibility to raise awareness of the different structures of ETFs and their different characteristics. As we engage with investors and talk about our ETF offerings, common questions focus on the role of active ETFs in particular: How they work, how they trade and how they’re used.

Tracing the Emergence of Active ETFs

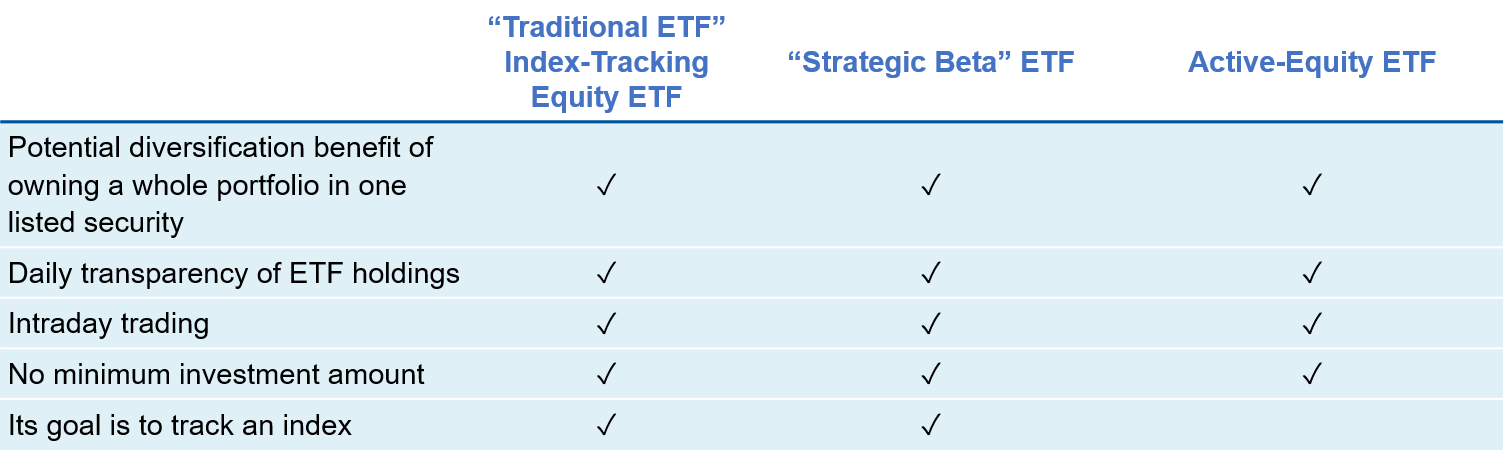

So-called “traditional” ETFs were constructed as a way for an investor to be able to buy and sell all the securities in an established index (such as the FTSE 100 or MSCI Europe share indices) in one vehicle that trades throughout the day. Market capitalisation refers to the market value of a company’s outstanding shares, which is computed by multiplying its stock price by the number of shares outstanding. In a capitalisation-weighted index, components are weighted according to the total market value of their outstanding shares.

These traditional ETFs tracked market-capitalisation weighted indices. Many investors may not realise a passive ETF can have what’s called a “tracking error;” that is, it may not perfectly mirror or track the underlying index. Certainly, one would not want their ETF to underperform the underlying index—which can happen—but outperforming the index also is considered a tracking error. In addition, market-cap weighted indexes are backward-looking, reflecting stocks that have performed well in the past—rather than looking at potential opportunity.

Over time, many investors recognised market-cap weighting methodology had issues that could cause unintended risks, which led to the development of “strategic” or “smart beta” ETFs. Smart beta ETFs also track an index, but follow a different set of rules regarding the construction of the portfolio.

Smart beta ETFs can be fairly simple, or quite complex. One of the simplest approaches of these portfolios is to hold securities in equal weights, rather than using market capitalisation. Others take a quantitative approach that systematically analyses, selects, weights and rebalances portfolio holdings based on certain investment style characteristics—called factors. In essence, these smart beta ETFs track a customised index.

Eventually, proponents of a more advanced approach to ETF construction recognised they could potentially attain many of the benefits of an ETF without having an underlying index at all. Active ETFs emerged in an attempt to achieve better investment outcomes versus traditional index products by combining the many benefits of the traditional ETF structure with an active investment approach.

Active ETFs don’t aspire to simply replicate or track a benchmark index, but seek to outperform it. To this aim, portfolio managers can actively respond to market events, changing allocation amid changing market environments. In some instances, they may even invest outside the confines of the benchmark index. The portfolio manager has full discretion on what assets go inside the fund.

So, in many ways, an active ETF resembles a traditional actively managed mutual fund, but the ETF vehicle trades on an exchange with the perceived benefits the ETF structure brings.

How Does an Active ETF Trade?

At the heart of the ETF ecosystem are two crucial sets of players: market makers (MMs) and authorised participants (APs). We explained their respective roles in detail in a previous article.

MMs facilitate the trading of ETFs by setting buy and sell prices for the ETF shares. These MMs tend to be household banking or stock broking organisations.

An AP acts as an intermediary between the buyer and seller of the ETF shares. Shares will only be created and transferred once the ETF issuer has received cash from the AP.

To trade an ETF effectively, MMs need to know either 1) the price of the underlying basket or 2) the price of other correlated instruments.

Pricing an Active ETF

One question that often comes up is: How would a MM update prices should an active ETF portfolio manager decide to change the composition of his or her portfolio during the day?

For a mutual fund investor, the price at which he or she buys or sells a fund is the current net asset value (NAV), calculated after all underlying markets close. So, if an active manager decides to buy or sell a security during the day, this purchase will be reflected and reconciled at the subsequent end-of-day NAV.1

However, owing to the intraday trading nature of ETFs, MMs need to know the portfolio composition daily. They need to ensure they can offer efficient buy/sell prices to clients, hedge subsequent flows accurately and ultimately know what they will receive at the end of the day, if they need to trade in the primary market with the issuer in question.

Every day the MMs receive a portfolio composition file (PCF) from the ETF issuer. This file is a clear snapshot of the constituents and weightings of the fund at the previous close.

Any buying or selling done by the active ETF manager during the day will be reflected in the same manner as an active mutual fund. In addition, it will be reconciled at the end-of-day NAV and be included for accurate market making in the subsequent PCF sent to the MMs the following morning.

Hence, active ETFs give investors similar features as an active mutual fund, but with the additional benefits of enhanced liquidity options and intraday access to that liquidity.

The trading of an active ETF in the secondary market (public exchange) is identical to the trading of any other ETF. In other words, the ETF trades in line with the prices of its underlying basket, but basket weights and/or composition will differ from one active ETF to another.

Liquidity of Active ETFs

Liquidity is a crucial concern for many investors today. The multiple layers of liquidity that ETFs can offer via both the secondary and primary markets—where investors directly purchase or sell securities from an issuer—may prove an attractive consideration.

Investors have the option to offer their ETF units to another investor in a so-called secondary market trade. But what if there are no willing buyers? That’s where the structure of ETFs makes a difference: One of the central characteristics of an ETF is that the supply of shares is flexible.

Should there be no willing buyers, an ETF investor may still have the option to sell to an AP who effectively offers primary market liquidity. These functions apply equally to active as well as passive ETFs. So, an active ETF should ideally offer the combination of the liquidity of an ETF structure with the asset selection function of an active mutual fund. In our view, this flexibility provides a strong use case for active ETFs.

View Jason Xavier’s previous articles here.

To get insights from Franklin Templeton delivered to your inbox, subscribe to the Beyond Bulls & Bears blog.

To comment or post your question on this subject, follow us on Twitter @FTI_Global and on LinkedIn.

Important Legal Information

The comments, opinions and analyses are the personal views expressed by the investment managers and are intended to be for informational purposes and general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice. The information provided in this material is rendered as at publication date and may change without notice and it is not intended as a complete analysis of every material fact regarding any country, region market or investment.

Data from third-party sources may have been used in the preparation of this material and Franklin Templeton Investments (“FTI”) has not independently verified, validated or audited such data. FTI accepts no liability whatsoever for any loss arising from use of this information, and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user. Products, services and information may not be available in all jurisdictions and are offered by FTI affiliates and/or their distributors as local laws and regulations permit. Please consult your own professional adviser for further information on availability of products and services in your jurisdiction.

What Are the Risks?

All investments involve risks, including possible loss of principal. The value of investments can go down as well as up, and investors may not get back the full amount invested. Brokerage commissions and ETF expenses will reduce returns. ETF shares may be bought or sold throughout the day at their market price on the exchange on which they are listed. ETFs trade like stocks, fluctuate in market value and may trade above or below the ETF’s net asset value. However, there can be no guarantee that an active trading market for ETF shares will be developed or maintained or that their listing will continue or remain unchanged. While the shares of ETFs are tradable on secondary markets, they may not readily trade in all market conditions and may trade at significant discounts in periods of market stress.

1. Net asset value represents the amount per share you would receive if you sold shares that day. It is calculated by diving the total value of cash and securities in a fund’s portfolio (minus any liabilities) by the number of shares outstanding.

This post was first published at the official blog of Franklin Templeton Investments.