by Edward D. Perks, CFA, Franklin Templeton Investments

The question of “where do we go from here?” appears to be on the lips of trade negotiators, central bankers and investors worldwide. The more that people scratch their heads and wonder what happens next, the more likely it is that two things happen: the yield on perceived safe-haven assets declines, and the price of insuring against uncertainty goes up.

We believe that a return to long-run levels of market volatility since early 2018—rather than the muted levels seen for much of the past 10 years—indicated that we have entered a new risk regime. Taken together with the ongoing headwinds to global growth, we are not surprised to have seen sharp moves in financial assets and a rise in expected volatility.

But what is the impact on the global economy; where is it headed? Many of our concerns have remained the same through the first half of 2019. Few have been resolved. Simmering concerns over the European auto sector and arguments over the level of tax to be paid by online businesses generating profits in foreign markets demonstrate that uncertainties look set to remain elevated.

Most notably, trade relations between the United States and China have seen a marked breakdown in trust, despite a decent working relationship between Presidents Donald Trump and Xi Jinping personally. The truce they brokered just a few weeks ago, at the meeting of G20 leaders in Osaka, has been superseded by the announcement of new tariffs on Chinese goods imported into the United States.

With no clear path to a resolution between the United States and China, exchange rates appear to be the next battleground with fears of competitive devaluations presenting a new aspect to the ongoing trade war. By allowing the renminbi to weaken beyond seven to the US dollar, the Chinese authorities appear to be less optimistic about reaching a near-term settlement over trade. Letting the currency move to better reflect deteriorating fundamentals is an example of how, at least for now, President Xi has more levers to pull than President Trump.

Despite all of this tension, it is not inconceivable that deals could get done, and investors could relax once more. But the uncertainty persists for now.

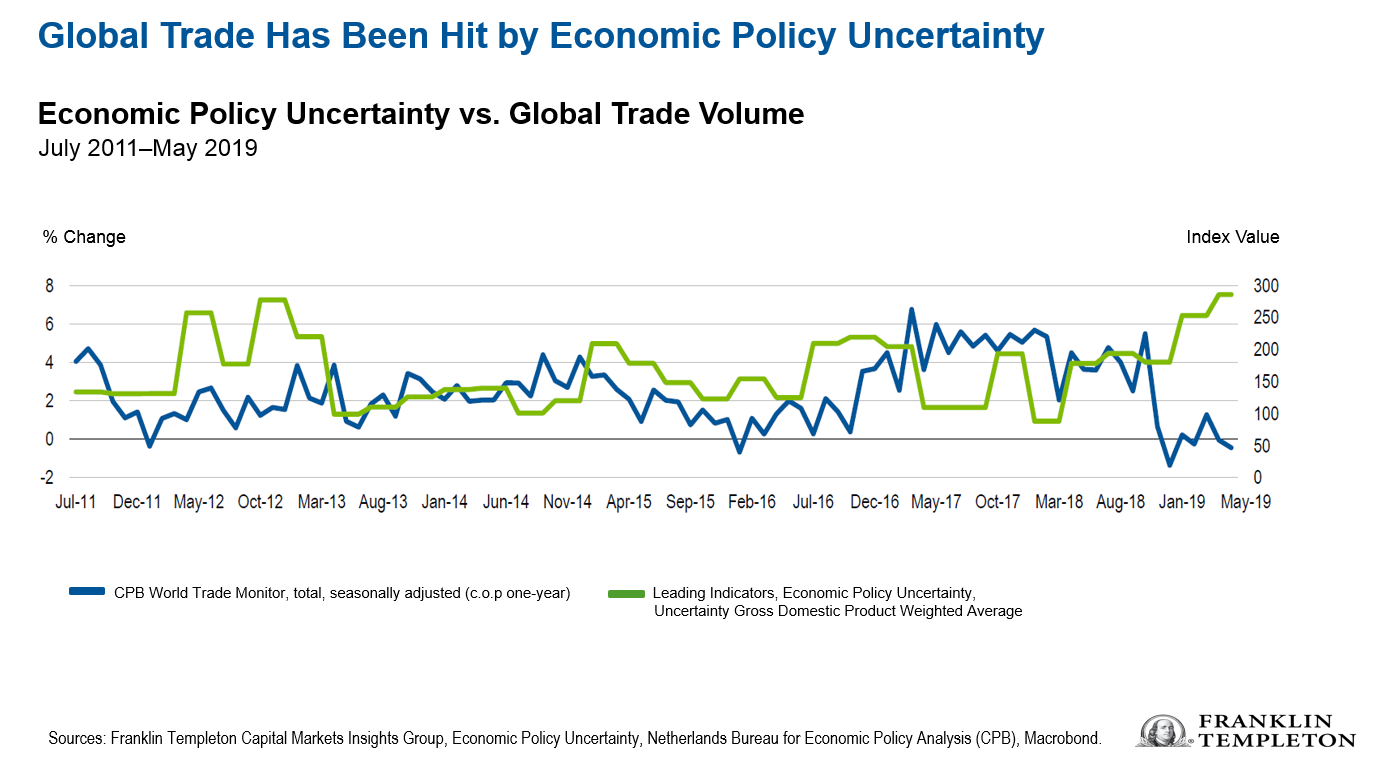

The longer these concerns impact investor sentiment, the more new orders are deferred and investment plans curtailed. Although many parts of the major developed economies are holding up well—with the service sector yet to feel the direct impact from slower global trade—the knock-on effects have become more likely.

The deeper the trade slowdown and the longer it persists, the harder it is to see the service sector—the largest part of the developed economies—avoid some form of contagion. For now, employment levels have remained high and consumers have been able to sustain their spending. While we continue to see few imbalances, and the probability of recession remains moderate, the risks are rising. Our dominant theme remains “Slower Global Growth Is a Rising Concern.”

Bond Yields Are Depressed for a Reason

In recent months, markets have moved to discount lower interest rates from many of the main central banks across the globe. In July alone, rate cuts were delivered in key emerging markets such as Brazil, Russia and Turkey as well as in major economies such as Australia and the United States.

The European Central Bank (ECB) signalled that it would likely follow suit as soon as September and consider re-starting its quantitative easing programme. The Bank of Japan (BoJ) similarly indicated that it stood ready to act decisively if need be, especially if the Japanese yen was to appreciate making it harder to achieve the central bank’s inflation objective.

Across emerging market economies, inflation pressures are muted, and many central banks have scope to cut interest rates to support activity. We observe that, unlike their developed-market peers, emerging market currencies tend to appreciate in such an environment. In the absence of a strongly appreciating US dollar more broadly, we have increased our conviction in the longer-term value seen in emerging market currencies, supported by the prospect of additional injections of liquidity from developed markets. To reflect this, we have upgraded our outlook for emerging market local currency bonds.

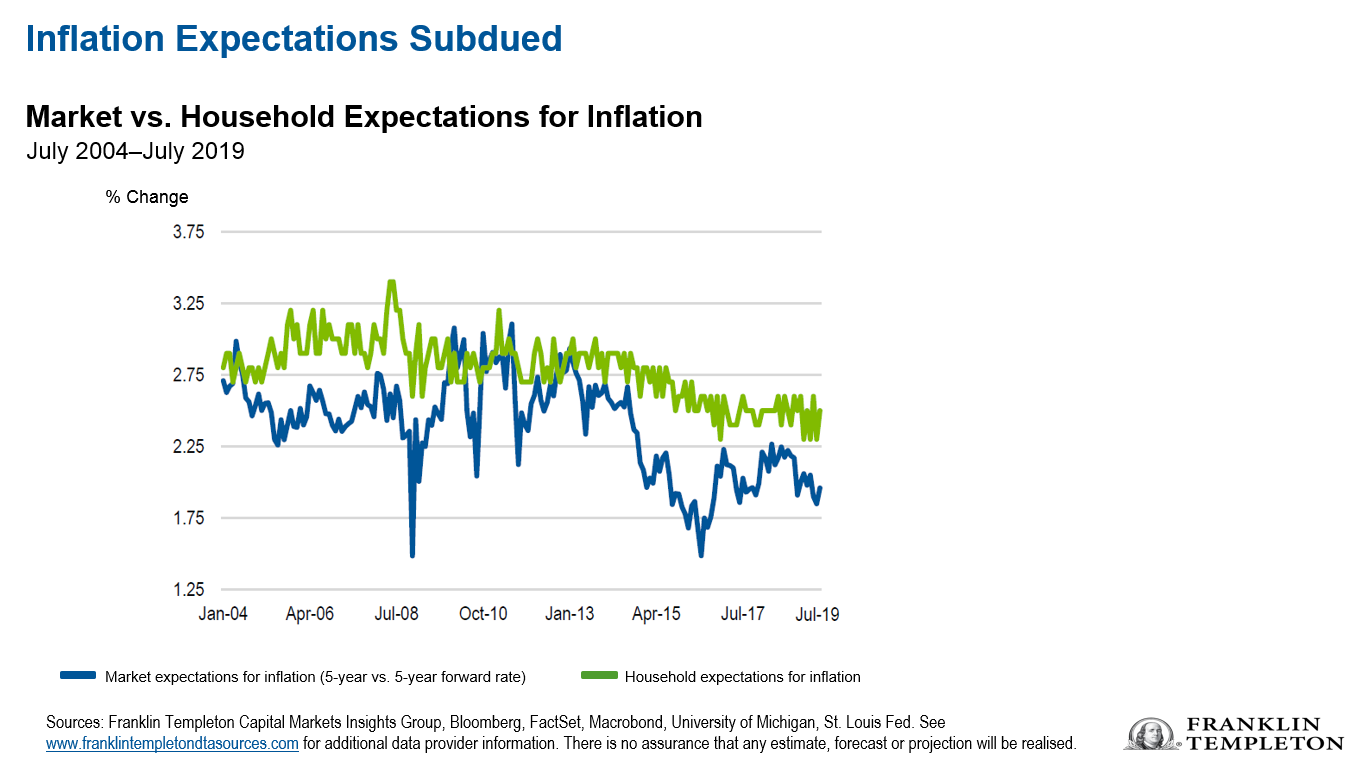

Efforts to resuscitate inflation expectations remain the key driver of monetary policy. Market-based inflation expectations have fallen sharply (see chart below) and remain well below the targets set by policymakers. Government bond yields have moved towards cyclical lows in many markets and to all-time lows in others. This reflects inflation expectation as much, if not more so, than fears of slower economic growth. While we remain cautious about the valuation of developed market bonds, this is balanced in our neutral overall view by the continued impact of our major theme of “Subdued Inflation Across Economies.”

Ongoing Policy Tensions

The extent to which policymakers are able to meet market expectations is being tested. The US Federal Reserve (Fed) cut interest rates for the first time in a decade at the end of July. Although this move had been well flagged to markets and its size (25 basis points) was in line with consensus expectations, the accompanying message seemed less palatable. Comments by Fed Chair Jerome Powell that the central bank was offering a limited mid-course correction to policy, rather than suggesting that it might mark the start of a longer series of cuts, appeared to disappoint equity markets.

The decline in bond yields that accompanied this message, and was further extended when President Trump raised the prospect of tariff increases, makes the next move even harder for the Fed. Markets now anticipate a succession of rate cuts through year-end, at least in part to offset the impact of trade concerns, but also to offset any hit to market confidence. Increasingly, it looks like the Fed is being pushed towards actions that it is less able to justify on the basis of the central bank’s dual mandate of stable prices and maximum employment, highlighting our theme of “Ongoing Policy Tensions.”

Against a backdrop of slower growth and concerns that profit margins have peaked, global equities as a whole are not cheap, in our analysis. Any further market confusion over the Fed’s delivery of rate cuts might hurt market stability.

Having taken a more cautious stance on risk assets over the first half of the year, we continue to believe navigating the challenges 2019 presents will require nimble management.

Get more perspectives from Franklin Templeton delivered to your inbox. Subscribe to the Beyond Bulls & Bears blog.

For timely investing tidbits, follow us on Twitter @FTI_Global and on LinkedIn.

Important Legal Information

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as at publication date and may change without notice. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market.

Data from third party sources may have been used in the preparation of this material and Franklin Templeton Investments (“FTI”) has not independently verified, validated or audited such data. FTI accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments opinions and analyses in the material is at the sole discretion of the user.

CFA® and Chartered Financial Analyst® are trademarks owned by CFA Institute.

What Are the Risks?

All investments involve risks, including possible loss of principal. The value of investments can go down as well as up, and investors may not get back the full amount invested. The positioning of a specific portfolio may differ from the information presented herein due to various factors, including, but not limited to, allocations from the core portfolio and specific investment objectives, guidelines, strategy and restrictions of a portfolio. There is no assurance any forecast, projection or estimate will be realised. Stock prices fluctuate, sometimes rapidly and dramatically, due to factors affecting individual companies, particular industries or sectors, or general market conditions. Bond prices generally move in the opposite direction of interest rates. Thus, as the prices of bonds in an investment portfolio adjust to a rise in interest rates, the value of the portfolio may decline. Special risks are associated with foreign investing, including currency fluctuations, economic instability and political developments. Investments in emerging markets, of which frontier markets are a subset, involve heightened risks related to the same factors, in addition to those associated with these markets’ smaller size, lesser liquidity and lack of established legal, political, business and social frameworks to support securities markets. Because these frameworks are typically even less developed in frontier markets, as well as various factors including the increased potential for extreme price volatility, illiquidity, trade barriers and exchange controls, the risks associated with emerging markets are magnified in frontier markets. Derivatives, including currency management strategies, involve costs and can create economic leverage in a portfolio which may result in significant volatility and cause the portfolio to participate in losses (as well as enable gains) on an amount that exceeds the portfolio’s initial investment. A strategy may not achieve the anticipated benefits, and may realise losses, when a counterparty fails to perform as promised. Currency rates may fluctuate significantly over short periods of time and can reduce returns. Investing in the natural resources sector involves special risks, including increased susceptibility to adverse economic and regulatory developments affecting the sector—prices of such securities can be volatile, particularly over the short term.

This post was first published at the official blog of Franklin Templeton Investments.