by Oliver Field, Russell Investments

That new apartment complex across the street. The toll bridge you used to get to work. The silver necklace you got your spouse for your anniversary (if you didn’t forget). What do these all have in common? They fall under the broad umbrella of real assets.

Portfolio construction typically begins with the allocation between equities and fixed income, but we believe it shouldn’t end there. Real assets such as infrastructure, real estate, natural resources and commodities provide an opportunity to diversify your portfolio, while current market conditions offer support for the asset class.

Potential benefits of real assets

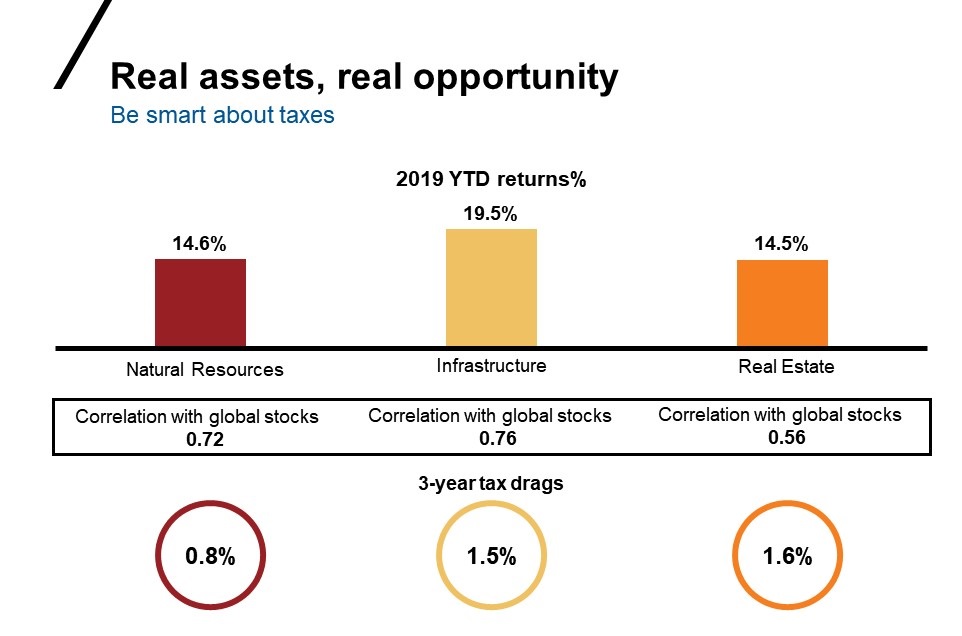

Historically, real estate, infrastructure and natural resources have enjoyed lower correlations to global stocks than other asset classes (shown in the chart below).

Because of these relatively low correlations, real assets may be combined to offer true diversification in an increasingly interconnected marketplace. This approach can be especially useful during market corrections and downturns.

Infrastructure securities, for example, have outperformed during 15 of the 20 quarters of negative equity market performance since 2001.1 Given the late-cycle nature of the current market environment and the return of volatility, we think these asset classes are worth a second look.

Current market environment

The current market environment has offered support to real assets, as witnessed by strong YTD returns:

Click image to enlarge

Index returns represent past performance, are not a guarantee of future performance, and are not indicative of any specific investment. Indexes are unmanaged and cannot be invested in directly. Correlation measures the degree to which two securities move in relation to each other and will show a range of between -1.0 to +1.0. Tax drags: Morningstar category averages – US Fund Natural Resources, US Fund Infrastructure, US Fund Global Real Estate

Sources: Natural Resources: S&P Global Natural Resources, Infrastructure: S&P Global Infrastructure Index, Real Estate: FTSE EPRA Nareit Global Real Estate Index. Global stocks: MSCI World Index. Correlations for the 5 years ending June 30, 2019.

Traditional safe havens such as gold and precious metals have seen positive performance in 2019 and have offered refuge in times of slowing global growth, inflation, or uncertain central bank policy.2

Energy, another key driver of the natural resources and commodity space, has seen a bounce off 2016 lows. Supply cuts have stabilized oil prices, and demand for energy—particularly in emerging markets—remains strong.

Despite minor headwinds including retail spending habits and soft spots in some markets, real estate is buoyed by strong new build numbers and the renewed prospects of low interest rates. While a major infrastructure bill does not appear on the near-term horizon in the United States, global infrastructure spending remains strong and like real estate, it is supported by recent central bank policy.

Beware of taxes

Higher yields and large amounts of distributed income can increase the potential for tax surprises in real assets. In non-qualified accounts, this drag could result in lower after-tax returns and can compound to reduce portfolio growth over time.

For some underlying real asset sectors, this tax drag can be upwards of 2.5% annually.3 Beware of this potential obstacle and opportunities to combat it. Weigh the costs and benefits of diversification and growth against the backdrop of after-tax returns.

Bottom line

The interdependence of markets indicates that investors should look beyond traditional asset classes for diversification. In non-qualified accounts, these benefits should be weighed against potential tax consequences and mitigated when possible. Infrastructure, real estate, natural resources and commodities provide a unique opportunity to access potential differentiated growth, while possibly providing downside protection.

We suggest an allocation to real assets. Current market cycle timing and interest rate movements offer a strong backdrop against which to add real assets to a well-diversified portfolio.

1 Source: S&P Global Infrastructure Index vs MSCI World Index; as of 31 March 2019. Russell Investments calculations.

2 Source of gold and precious metal returns: Morningstar as of June 25, 2019. Gold—HUI Gold Index, precious metals—S&P GSCI Precious Metals.

3 Source: Morningstar Direct, as of March 31, 2019. Morningstar US Fund Real Estate category, 5-year annualized figures.

Copyright © Russell Investments