by Daryl Clements, AllianceBernstein

Municipal bonds have had a good run since the beginning of the year, but there’s still room for additional positive performance in 2019. That’s particularly true for investors who choose active strategies with the flexibility to move money around the bond market as conditions evolve.

As of late July, municipal bonds had returned 5.8% year to date and seen net mutual fund inflows of some $52 billion. We expect the strong demand and relatively weak issuance driving those returns to continue. This summer, bond calls and maturities are expected to exceed new issuance by $48 billion.

Against that overall positive backdrop, muni investors should keep three things in mind as 2019 winds down.

1. Think Carefully About Cash

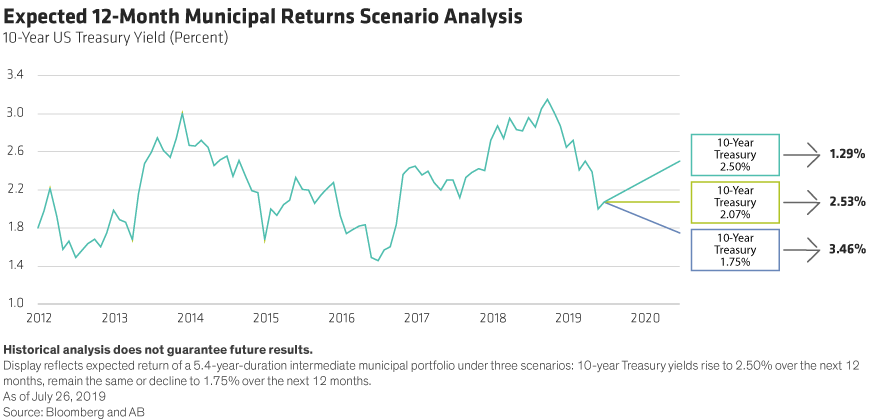

Despite the technical factors driving muni performance and the fact that muni bond investors will receive $45 billion in coupons this summer, some investors are still parking money in cash and wondering if it makes sense to buy when yields are so low. Our research shows that a portfolio of intermediate-duration munis would outperform cash in most scenarios.

The 10-year US Treasury yield would have to climb to 2.54%—up from 2.07% as of July 26—for one-year returns on intermediate municipal bonds to break even with returns on one-year Treasury bills, a proxy for cash (Display 1).

With central bank easing on the horizon, rising rates are less of a concern for many investors now than they were a few months ago. However, should the Federal Reserve change its stance again, it’s worth noting that municipal bonds held steady even when rates were rising quickly. Intermediate-duration municipal bonds have held their value as the Fed hiked rates seven times between July 2016, when 10-year yields touched a low of 1.37%, and November 2018, when they topped out at 3.24%.

2. Be Ready to Pivot

That said, investors will benefit from the flexibility to move into other types of bonds at the appropriate times.

Consider the relationship between US Treasuries and municipals. For example, after taxes, 10-year AAA-rated muni bonds yield just 0.31% more than 10-year US Treasuries, compared to the long-term average of 0.94%. Indeed, long-duration munis are almost as expensive as they’ve ever been. Over time we would expect US Treasuries to outperform munis when spreads inevitably revert to the mean, and owning them now would dampen volatility—which is, after all, the goal of a muni bond portfolio.

At a time when yields are low and supply is extremely limited, the flexibility to own mid-grade and higher-yielding bonds is also a boon to muni investors. The expanding economy has bolstered muni credit fundamentals. For example, during this summer’s budget season, 28 states reported that they’d collected more than they expected in taxes, and state rainy day funds reached an all-time high of 7.5% as a share of general fund spending.

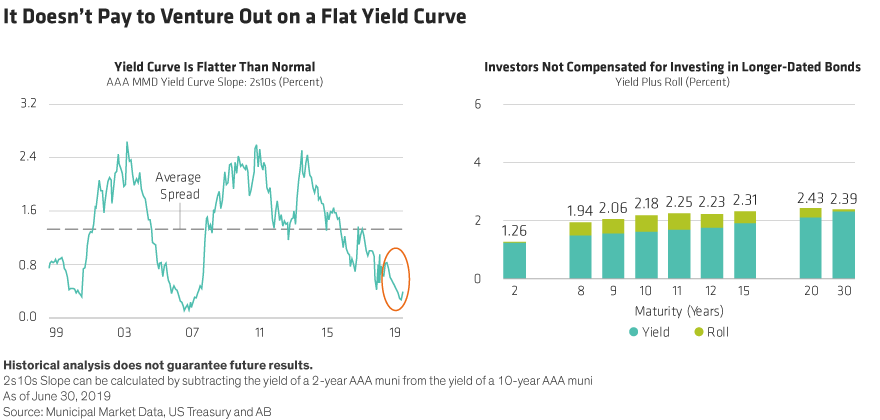

Finally, being able to change maturity structures as the yield curve changes shape may also be a boon to investors in the months ahead. At the moment, the yield curve is flatter than usual, so it generally makes sense for investors to be somewhat concentrated in intermediate-duration bonds. However, should the curve steepen again, it will behoove investors to move into a more barbell-like structure.

3. Don’t Reach Too Far for Yield

Though investing in higher-yielding bonds can be helpful in a low-yield environment, it’s the wrong time to reach too far out on the yield curve or too far down the credit spectrum.

The yield curve is remarkably flat, and we believe investors aren’t being adequately compensated for taking on additional duration risk. A 10-year, AAA-rated muni bond pays just 38 basis points more than a two-year bond with the same rating, compared to the long-term average spread of 1.33%. And investors can earn 91% of what they would earn on a 30-year bond by investing in a 10-year (Display 2).

Investors also need to be highly selective when choosing high-yield bonds. High-yield municipal funds have performed particularly well in 2019, returning 6.5% on average and attracting $10.5 billion in net new money. That’s nearly 10% of all high-yield municipal assets under management.

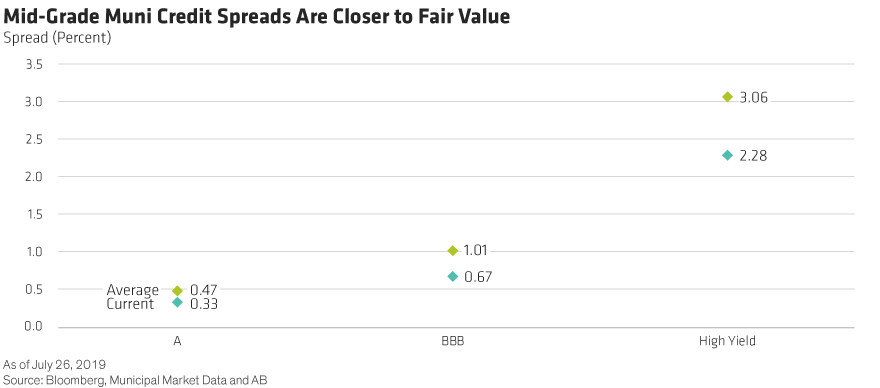

But the spread over investment-grade muni bonds has also narrowed significantly—to 2.28% compared to the post-2008 average of 3.28%. These aren’t uncharted waters, as the average spread from 1996 through 2007 was 1.9%, but investors do face a risk that spreads could widen again.

Where appropriate, investors should consider moving out of high-yield muni bonds that appear to be fully valued and into mid-grade bonds that appear to be more fairly valued. BBB- and A-rated credits are running close to their post-crisis averages and may offer better opportunities. (Display 3). There is always the option to swap back into high yield bonds when spreads widen.

Investors should also be mindful that as enthusiasm for high-yield munis has grown, so has the number of relatively risky deals featuring borrowers such as nursing homes or charter schools, which lack direct taxation power and don’t provide an essential service such as clean water or sewage treatment. Now more than ever, investors must rely on strong fundamental research into each individual high-yield credit before investing.

The long and the short of it? Active muni managers with flexible approaches have more options for taking advantage of opportunities and avoiding potential sinkholes. Sitting on the sidelines isn’t a good option at this point, but being locked into a tightly restricted approach isn’t the best choice, either.

Daryl Clements is Portfolio Manager—Municipal Bonds at AllianceBernstein (AB)

The views expressed herein do not constitute research, investment advice or trade recommendations, do not necessarily represent the views of all AB portfolio-management teams, and are subject to revision over time.

This post was first published at the official blog of AllianceBernstein..