by David Zahn, CFA, FRM, Franklin Templeton Investments

Will the EU Fall Apart or Stay Together?

Once upon a time, bonds backed by a government’s full faith and credit pledge were generally considered less risky than corporate bonds. Times have changed. In today’s political climate, not all governments inspire us with the same confidence.

Consider Italy. Last year, Rome’s new government was keen to deliver its pledge of overturning pension reforms and offering a citizens’ income for the unemployed. Widely popular with voters, Italy’s proposed budget rattled bond markets and frustrated European Union (EU) leaders in Brussels. Headlines in Europe and the United States warned a new euro crisis was looming.1

The chief reason? Eurozone firewalls—built to prevent a rerun of the 2010–2012 eurozone debt crisis—depend on Italy adhering to strict fiscal rules. And that seems to be the last thing Italy’s populists want to do.

Italy’s showdown with Brussels revived nagging anxieties about the currency union’s stability. If only the eurozone adopted a “fiscal union” like the United States, then things wouldn’t be so bad, says the International Monetary Fund (IMF).2

Establishing a federal EU government with tax and spending authority, however, is a deeply polarising idea in Europe. It also lays bare a stark rift between the EU’s northern and southern economies. As a global firm with fixed income teams across Europe and the United States, we think the EU and US comparison offers a valuable perspective—one that could reveal a pathway forward for Europe. That said, the US approach by no means offers an economic panacea. The same pension issues that sparked Italy’s skirmish with Brussels loom even larger in the United States.

For Europeans suffering from US fiscal union envy, we say the grass isn’t necessarily greener across the Atlantic. In this article, we examine today’s eurozone from the vantage of the United States in the late 18th century, and its bumpy evolution towards a happier union.

A Marriage of Differences

At the heart of many EU challenges is the currency union. Like a bad marriage, the euro has shackled together 19 national economies that some economists believe are simply too different to coexist happily. The marriage was largely promoted for political reasons, not necessarily cogent economics.

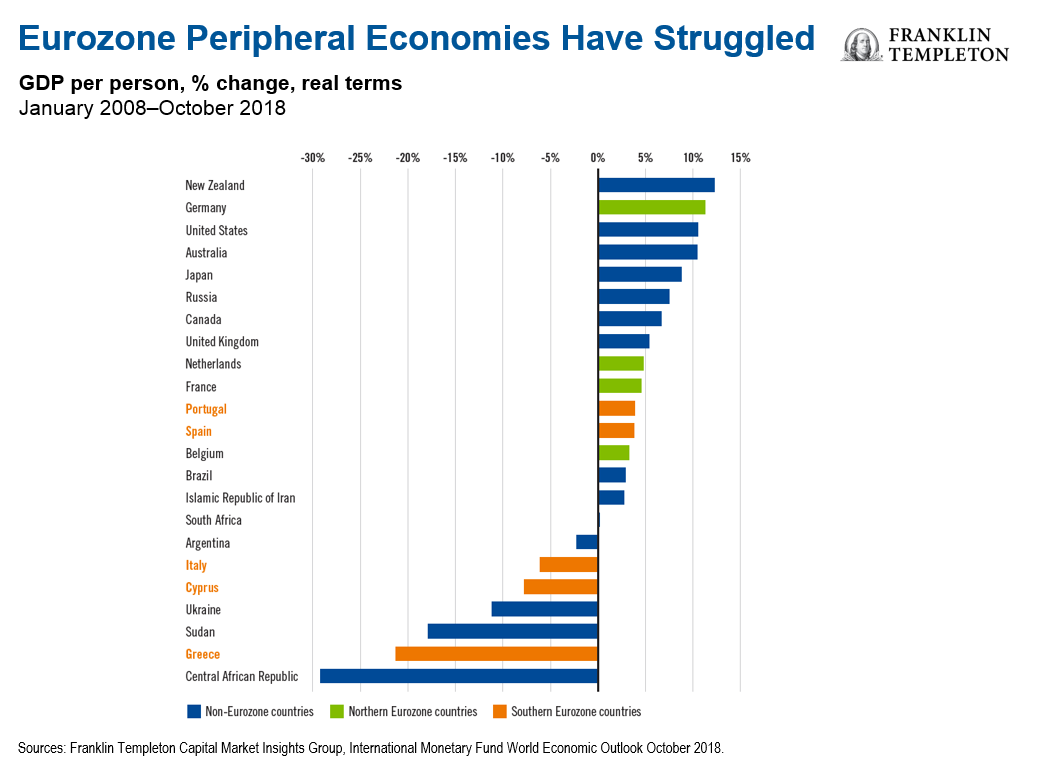

“Nations with a common currency never went to war against each other,” said Helmut Kohl, Germany’s chancellor at the euro’s birth. Looking at some of the world’s best and worst performers in terms of gross domestic product (GDP) growth, the chart below highlights the predicament the eurozone’s peripheral economies find themselves in. Greece has fallen behind Sudan and Ukraine in terms of growth. Italy and Cyprus have been outgrown by Iran and Brazil. And Spain and Portugal by Britain.

Tied to the euro, Italy can’t devalue its currency to be more competitive globally, and now faces spending cuts mandated by the EU’s Fiscal Stability Treaty. Brussels’ rules may appear callous to Italians, particularly during a recession, but Brussels thinks Italy’s political class is the real culprit. For decades, Italy refused to dismantle its Byzantine state, invest in infrastructure or crush entrenched corporate interests.

The Need for More Sharing

For economists like Ken Rogoff, Italy’s best long-term solution is for the EU to enhance its currency union—a half-marriage of sorts—with a fiscal union. “For southern Europe as a whole, the single currency has proved to be a golden cage, forcing greater fiscal and monetary rectitude but removing the exchange rate as a critical cushion.”3

Successful unions like the United States—the argument goes—transfer money from wealthier regions to struggling ones. EU economists call it “fiscal risk sharing.” We think broader fiscal risk sharing is a tall order for the EU at this moment in time. Many EU voters think handing more power to Brussels is insanity. Case in point is Hungarian Prime Minister Viktor Orban, who explicitly warns against becoming a “United States of Europe.”

Despite rising anti-EU sentiment across Europe, we think the United States offers some perspective on a pathway forward. We see today’s Europe at an interim stage similar to the United States in the late 18th century. The ratification of the US Constitution in 1788 was preceded by a loose confederation of states, which sometimes worked but mostly didn’t. To form a more perfect union, the United States’ first Secretary of the Treasury Alexander Hamilton proposed creating a single US currency along with a national bank to take care of the war debt each of the 13 states still owed.

Hamilton’s proposals were quite polarising in Congress. The most visceral opposition came from congressmen representing agrarian states such as Georgia and Maryland. Most southern states had nearly paid off their debts. In their eyes, nationalising the remaining liabilities would give an unfair advantage to profligate merchants living up north in states like Massachusetts and Pennsylvania.

The belief was those states simply hadn’t managed their debts properly. Southern members of Congress were also opposed to a US currency. Centralising power away from local banks was dangerous, and likely favoured the commercial interests of the industrialists and merchants up north. A backroom political compromise—one that included locating the new US capital in the south—eventually resolved the impasse in 1791.

Cross-Cultural Relationships

Fast forward to today, and we see a similar north and south divide in the EU. This time, northern EU members like the Dutch are balking at the idea of fiscal transfers and eurobonds. They make the same arguments Thomas Jefferson did against Hamilton’s federal institutions.

Their feelings are shared mutually by the eight members of the New Hanseatic League (“the Hansa”). Comprised of Ireland, the Netherlands, Nordic and Baltic states, this fiscally conservative, free-trade group formed after losing the like-minded United Kingdom after Brexit. The Hansa’s key policy focus is helping large and small EU businesses access more private capital instead of bank loans, harmonise EU bankruptcy rules, and uproot barriers to cross-border investments. Why is this worth doing? They believe more risk sharing from private capital markets could mean fewer bank bailouts—largely paid for by Germany.

In research papers published by the European Commission, the Hansa points out that small and medium-sized companies—the engine of growth in many countries—receive five times more funding from private capital in the United States than they do in the EU.4 When small firms grow into large companies, deep credit markets offer another non-bank source of capital and risk sharing. Here too the Hansa thinks the United States outshines the EU; the value of corporate-bond markets equals 31% of US GDP but just 10% of the EU GDP (once the UK is removed).5 Research from the IMF shows how important deep capital markets are in cushioning economic downturns in federalist countries like Germany and the United States.

Despite strident opposition to fiscal transfers across countries, we think the Hansa will eventually make incremental concessions. A chief hurdle in the near term is the cultural divide between northern and southern EU members—an obstacle the early United States didn’t have. The term “hanseatic” references a confederation of merchant guilds that grew from a few north German towns in the 1100s. Enthusiastic about free trade economics, the Hansa’s views on debt line-up with older Germans of the post-war era who still prefer shopping with hard cash rather than relying on credit cards.

Consider this cultural artifact: The word for debt in German is “schulden.” Schuld means blame or guilt. In the future, we think the eurozone will evolve to combine its fiscal capacity to help struggling members achieve a sustainable glidepath—one that relieves the young from performing penance for their forebear’s economic sins.

We’re not talking about embracing Modern Monetary Theory where public debt has no limits or consequence. In our view, a combination of rewards through fiscal risk sharing and penance through structural reforms can build a more stable and prosperous European Union.

Want more insights? Read the full “FT Thinks” paper.

To get insights from Franklin Templeton delivered to your inbox, subscribe to the Beyond Bulls & Bears blog.

For timely investing tidbits, follow us on Twitter @FTI_Global and on LinkedIn.

What Are the Risks?

All investments involve risks, including possible loss of principal. The value of investments can go down as well as up, and investors may not get back the full amount invested. Bond prices generally move in the opposite direction of interest rates. Thus, as prices of bonds in an investment portfolio adjust to a rise in interest rates, the value of the portfolio may decline. Investments in lower-rated bonds include higher risk of default and loss of principal. Special risks are associated with foreign investing, including currency fluctuations, economic instability and political developments. Investments in emerging markets involve heightened risks related to the same factors, in addition to those associated with these markets’ smaller size and lesser liquidity.

Important Legal Information

The comments, opinions and analyses expressed herein are for informational purposes only and should not be considered individual investment advice or recommendations to invest in any security or to adopt any investment strategy. Because market and economic conditions are subject to rapid change, comments, opinions and analyses are rendered as of the date of the posting and may change without notice. The material is not intended as a complete analysis of every material fact regarding any country, region, market, industry, investment or strategy.

The securities mentioned herein are used solely for illustrative purposes; any investment may or may not be currently held by any portfolio advised by Franklin Templeton Investments. The opinions are intended solely to provide insight into how securities are analyzed. It is not an indication of the trading intent of any Franklin Templeton managed portfolio. This is intended to provide insight into the portfolio selection and research process.

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice.

Data from third-party sources may have been used in the preparation of this material and Franklin Templeton Investments (“FTI”) has not independently verified, validated or audited such data. FTI accepts no liability whatsoever for any loss arising from use of this information, and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user. Products, services and information may not be available in all jurisdictions and are offered by FTI affiliates and/or their distributors as local laws and regulations permit. Please consult your own professional adviser for further information on availability of products and services in your jurisdiction.

CFA® and Chartered Financial Analyst® are trademarks owned by CFA Institute.

_________________

1. Source: The New York Times, J. Ewing and J. Horowitz, “Why Italy Could Be the Epicenter of the Next Financial Crisis,” 12 October 2018.

2. Source: International Monetary Fund, H. Berger, G. Dell‘Ariccia. and M. Obstfeld, “Revisiting the Economic Case for Fiscal Union in the Euro,” February 2018.

3. Source: Project Syndicate, “The Eurozone Must Reform or Die,” Rogoff, K. 14 June 2017.

4. Source: European Commission Brussels Green Paper, “Building a Capital Markets Union,” 18 February 2015; COM (2015) 63 final.

5. Source: European Commission Brussels, “Economic Analysis Accompanying the Mid-Term Review of the Capital Markets Union Action Plan, 8 June 2017; SWD (2017) 224 final.

Copyright © Franklin Templeton Investments