by Michael Hatcher, Head of Global Equities, and Director of Research, Invesco Canada Equity team, Invesco Canada

One of the things I’m often asked about is the amount of research travel that we on the Global Equities team undertake. It may sound glamorous to be on a research trip to Europe, but it’s actually pretty exhausting.

It can also be very enlightening.

Over the course of five days in May, I visited 14 companies. Normally it’s closer to 20 – the lower count was due to the logistics involved, as I was in five different cities.

I needed to see some of the anchor companies in Invesco Global Companies Fund (formerly Trimark Fund), so that took me to Frankfurt, Walldorf, Dusseldorf and Essen, in Germany, and then to London, U.K., before heading home.

These trips require a lot of intestinal fortitude because things happen on the road that you can’t predict. If you’ve ever been on a highly scheduled vacation, where you need to be in a specific place at every single moment in time, that’s what these research trips are like.

I flew overnight, landing in Frankfurt around 6 a.m.

My first stop was SAP SE (see below for fund weightings), a multinational company that makes enterprise business software, about an hour’s drive south of Frankfurt. One of the benefits you get when you visit someone’s head office is you are actually building a relationship. These face-to-face meetings show your level of commitment to the investment. On the other hand, if you’re travelling with a broker where you’re just one of 12 portfolio managers, company representatives often don’t even know you’re visiting their head office.

At SAP, they’re doing something very exceptional – they have completely re-engineered how they structure their databases. In my opinion, this is the biggest transformation in database technology in the past 25 years. This “in-memory” database structure allows its clients to get all business data in real time.

One of SAP’s biggest strengths is its suite of services. As soon as a client experiences a glitch with a third-party software supplier, SAP is able to step in and replace the entire system.

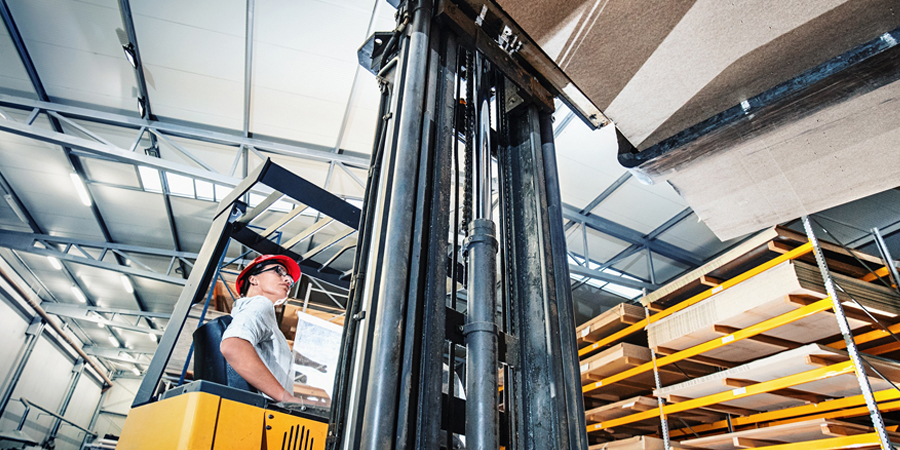

Back in Frankfurt, I met with KION Group, one of the world’s leaders in warehouse infrastructure. It dominates the forklift market, and it also dominates in creating the IT systems used in warehouse management.

It’s an important company in and of itself, but if you want to understand companies that are built on warehouse distribution, like W.W. Grainger, Inc. (see below for fund weightings), or Amazon (which we don’t own), how they distribute product is incredibly important. This is one level down into the companies that you’re investigating, meaning you can gain a first-hand understanding of how their systems, technology and operations work, and how these can provide them with a sustainable competitive advantage.

This ties into another meeting that I had the next day with Henkel AG & Co. KGaA, which we hold in several funds (see below for fund weightings). I spent about three hours touring one of their largest distribution centres in Europe. So, I’ve gone from the people making the warehouses (KION) to an actual state-of-the-art warehouse.

At Henkel, they demonstrated how they’re now doing inventory via drones, which was the first time that I’ve seen that in a warehouse. Picture warehouse racks that go up more than two stories, and the drone can see what’s on every single pallet, check that the pallet is structurally sound and do an inventory count. This greatly reduces the risk of human injury, because the drones are working at heights.

During another part of the tour, I visited the section of the warehouse that was fully automated. The racks were about five stories high. It was semi-dark in this warehouse, which was about the size of two football fields. It is a completely automated warehouse – no humans work there.

Cost/benefit

One of the benefits of these trips, as you can imagine, is you can have these back-to-back conversations. I went straight from an SAP meeting to visiting two of their largest customers. These meetings gave me greater confidence in SAP.

So, everything I’ve learned in the first meeting is still top of mind, and I’m able to test my investment hypothesis with different people. And that’s how you build the mosaic as to how your thesis should actually work.

Arranging a trip to see multiple companies in back-to-back meetings can provide invaluable insight into how they intertwine.

These trips are highly valuable, and while they can be quite expensive, these costs don’t get passed on to our clients. These costs hit the bottom line of Invesco Canada.

A lot of portfolio managers say they travel, but it’s often just to a conference and then they’re going from the airport to a big hotel in London or some other major centre.

Our due diligence doesn’t end with the quarterly earnings call or at an industry conference. I think our rigorous on-site research sets us apart from many other portfolio managers.

And while Europe has its challenges, the emerging markets tend to be at a whole other level of not only risk, but of logistical nightmares, that our team goes through.

This post was originally published at Invesco Canada Blog

Copyright © Invesco Canada Blog