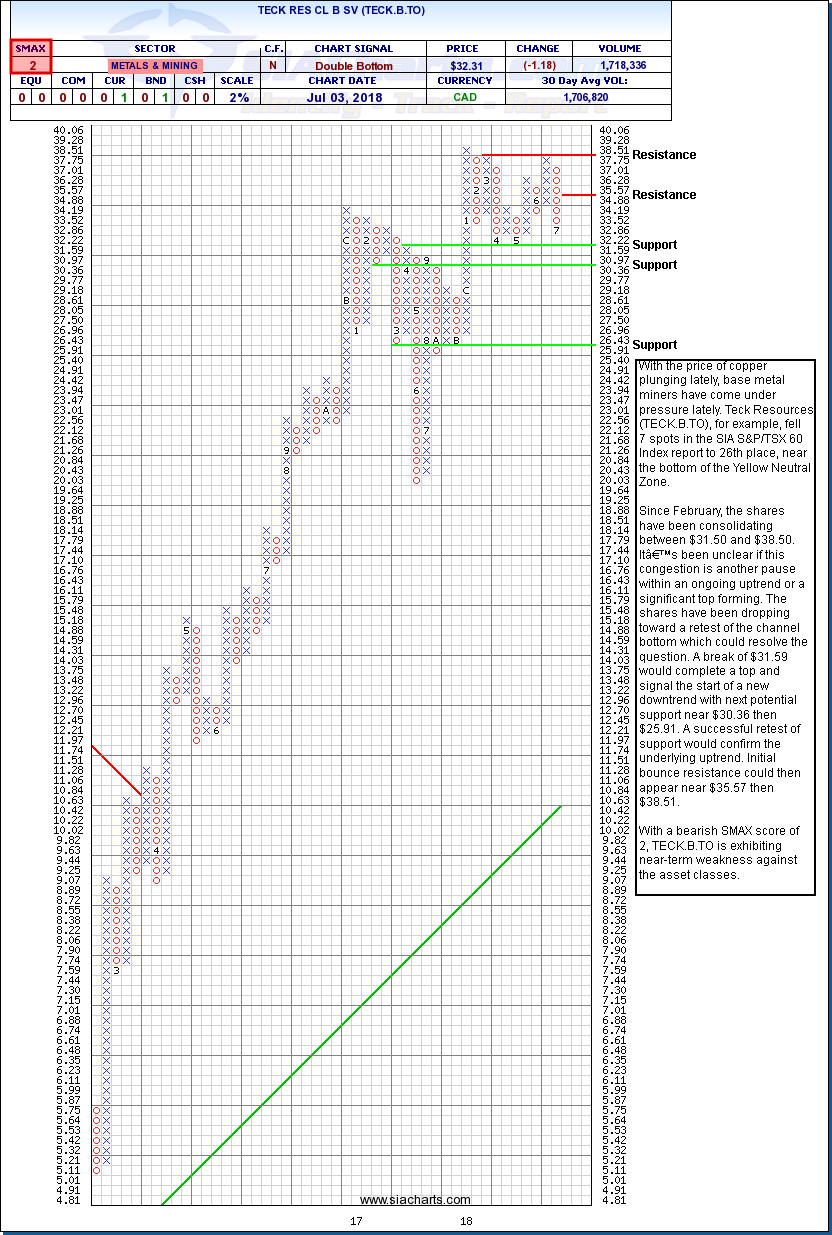

TECK RES CL B SV (TECK.B.TO) TSX - Jul 04, 2018

SIA Charts Daily Stock Report (siacharts.com)

The SIA Daily Stock Report utilizes a proven strategy of uncovering outperforming and underperforming stocks from our marquee equity reports; the S&P/TSX 60, S&P/TSX Completion and S&P/TSX Small cap. We overlay these powerful reports with our extensive knowledge of point and figure and candlestick chart signals, along with other western-style technical indicators to identity stocks as they breakout or breakdown. We provide SIA Subscribers with truly independent coverage of the Canadian stock market with specific buy and sell trigger points.

Note: Subscribers can screen all Canadian and U.S. stocks and mutual funds, or as components of equally weighted mutual fund sectors indices, and fund groups by issuer, all Canadian Exchange Traded Funds, by issuer (iShares, Horizons, BMO), or as components of Equally Weighted Fund Sector Indices (e.g. 2020+ Target date, Cdn Equity Lg Cap), and create and monitor their own, or SIA's existing model portfolios.

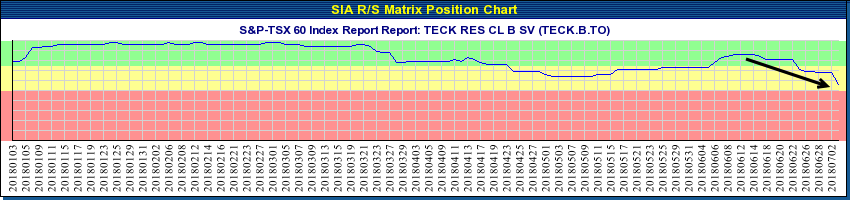

Subscribers may generate BUY-WATCH-SELL Signals on demand with SIA Charts' proprietary Favoured/Neutral/Unfavoured, SMAX scoring algorithm (see green-yellow-red graph 1 below).

GREEN - Favoured / Buy Zone

YELLOW - Neutral / Hold Zone

RED - Unfavoured / Sell / Avoid Zone

TECK RES CL B SV (TECK.B.TO) TSX - Jul 04, 2018

Important Disclaimer

SIACharts.com specifically represents that it does not give investment advice or advocate the purchase or sale of any security or investment. None of the information contained in this website or document constitutes an offer to sell or the solicitation of an offer to buy any security or other investment or an offer to provide investment services of any kind. Neither SIACharts.com (FundCharts Inc.) nor its third party content providers shall be liable for any errors, inaccuracies or delays in content, or for any actions taken in reliance thereon.

Copyright © siacharts.com