by Equities, AllianceBernstein

Global equity markets are still hurting from last week’s sell-off. Yet the renewed volatility could mark a return to reality after an unusually long period of steady gains and may even foster a healthier investing environment over time.

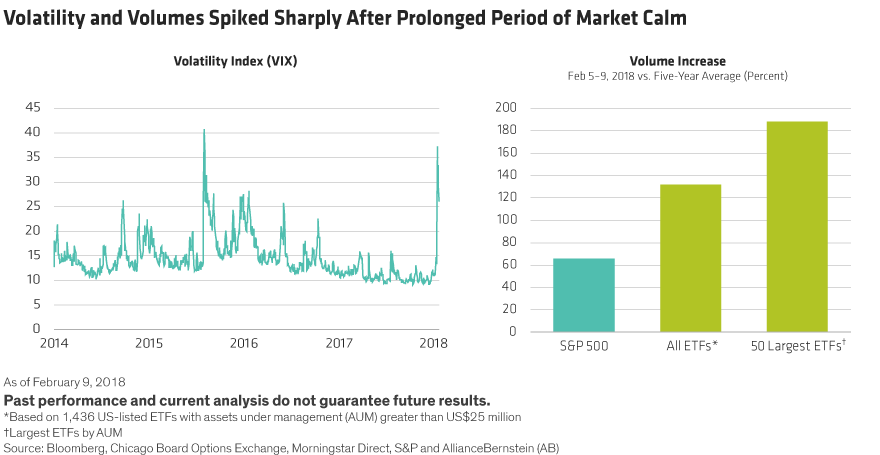

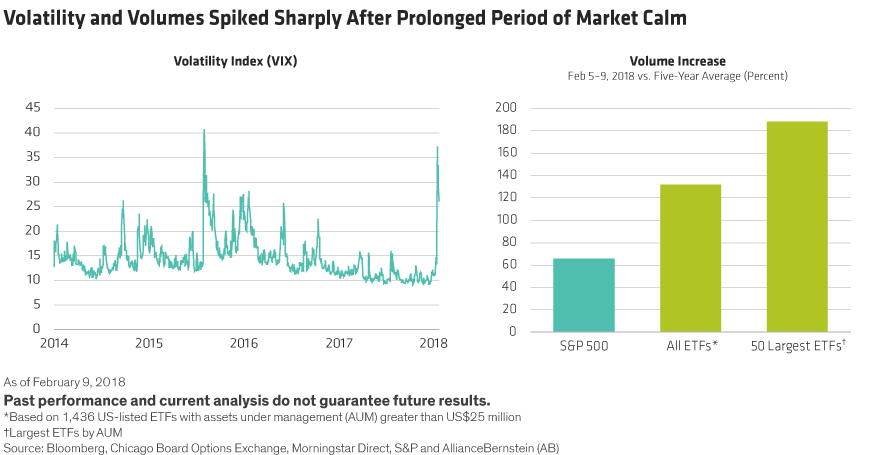

Investors are understandably unsettled, especially given the dramatic spike in volatility (Display, left). The extremely high trading volume of exchange-traded funds (ETFs) last week added fuel to the fire (Display, right). But the speed and size of recent moves seems inconsistent with the fundamentals of the global economy and company earnings, because both are strong.

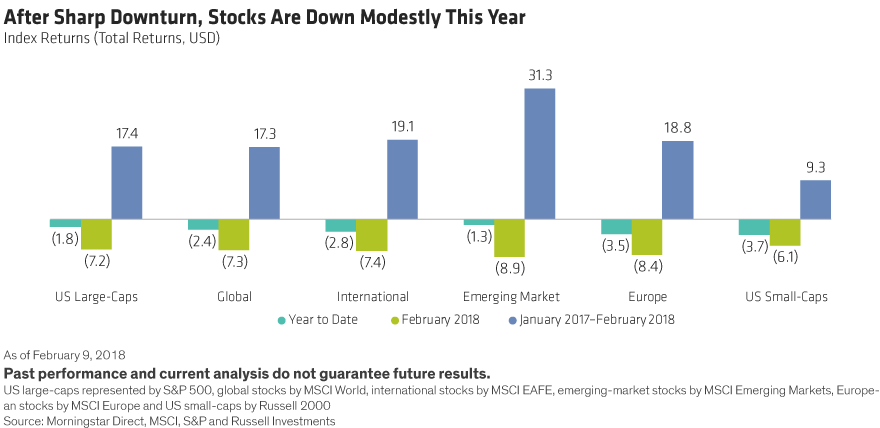

By the end of last week, US stocks had fallen more than 8.8% from their peak in January and at one point were down more than 10.0%, typically defined as a correction. Since the start of the year, the S&P 500 Index dropped 1.8% (Display). Markets in Asia and Europe have also been hit.

Tug-of-War: Inflation vs. Fundamentals

In many ways, the downturn was widely expected. In our view, equity markets are facing a tug-of-war between enthusiasm for good underlying economic conditions and earnings, and rising interest rates, which means more volatile market conditions are likely to persist.

The US wage report on February 2 appears to have been the epicenter of the downturn. Stronger-than-expected wage data reminded investors that inflation remains a real risk and fueled a rise in bond yields that began last September and accelerated in January. Many were already worried that rapidly rising interest rates would prompt a revaluation of equities.

Technical forces also played a role. Rules-based investment strategies that are forced to sell stocks when volatility jumps may have amplified the losses. Nine of the 20 ETFs with the biggest volume increases were nontraditional funds that were betting on volatility to stay low or were shorting the entire market. Indeed, the sell-off has so far been largely indiscriminate, with share prices falling even for companies that have reported strong earnings.

Still, the macroeconomic environment remains resilient. Unemployment is low and global economic growth is solid. US tax reform is expected to fuel capital investments and consumer spending.

The current earnings season has started well: More than halfway through US earnings season, 74% of S&P 500 companies have beaten earnings expectations. Across the US, Europe and Japan, earnings have so far risen by around 15% on average. Earnings expectations for US companies have been revised up by 6.4% since the end of 2017, as measured by the Russell 3000 Index.

Context Matters

When markets are falling, it’s easy to lose sight of the bigger picture. Last year was an abnormally strong year for stocks. Developed markets rose in all 12 months of 2017—the only time this has happened in 48 years. Emerging-market stocks posted 11 months of gains, which occurred only once in the past 30 years. Investors remained bullish in January 2018, when all US-listed ETFs pulled in US$78 billion—their largest monthly inflows ever.

Until this week, US stocks hadn’t experienced a 10% downturn in 100 weeks, more than three times longer than the average since 1928.

Volatility has been extraordinarily low. These gains and market conditions were always unlikely to continue indefinitely.

Real Risks to Consider

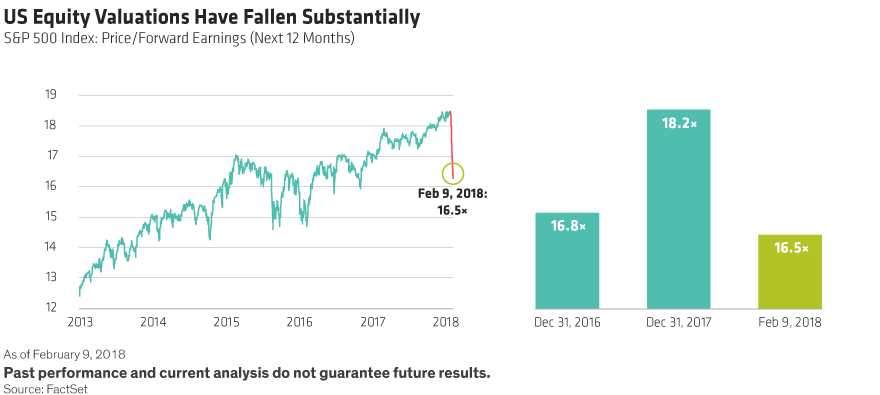

Valuations have been a persistent concern. At the start of the year, they were above historical averages, especially in the US. Now, the price/forward earnings ratio of S&P stocks has fallen to 16.5x, taking us back to 2016 levels (Display) as share prices dropped while earnings continued to rise.

In addition, the risk of a policy mistake remains real. It’s probably a coincidence, but last Monday’s market fall happened on Jay Powell’s first day as new Chair of the US Federal Reserve. To establish credibility, he can’t afford to take risks with inflation and may raise rates faster than markets expect.

If interest rates rise faster than expected, the discount rate applied to future earnings will go up, while companies’ borrowing costs will eventually rise. Rising bond yields would also prompt investors to demand a higher risk premium from equities, which could push valuations downward.

But would rising rates fundamentally undermine the market? Not necessarily. In the past, rising rates haven’t impeded stock market gains if they reflected improving economic growth—as they do today—rather than central banks slamming on the brakes to control inflation.

New Challenges, Improving Conditions

Even if equity returns fall back to lower levels, we still believe that the long-term return potential of stocks is attractive versus bonds. Our research also suggests that higher volatility creates better conditions for active equity managers to exploit mispricings of stocks and to deliver outperformance.

Market corrections are never easy to digest. But equity downturns can have a silver lining by providing investors with a better entry point to the market. When markets are in the throes of anxiety about short-term volatility, we believe that staying focused with a long-term perspective on company fundamentals is the key to steering through turbulent conditions and delivering results.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AllianceBernstein portfolio-management teams.

Copyright © AllianceBernstein