Deutsche Bank's Jim Reid argues that the emerging markets ETF has quietly become one of the most tech-concentrated vehicles in global markets -- and that most investors don't know it.

By AdvisorAnalyst.com Editorial Team

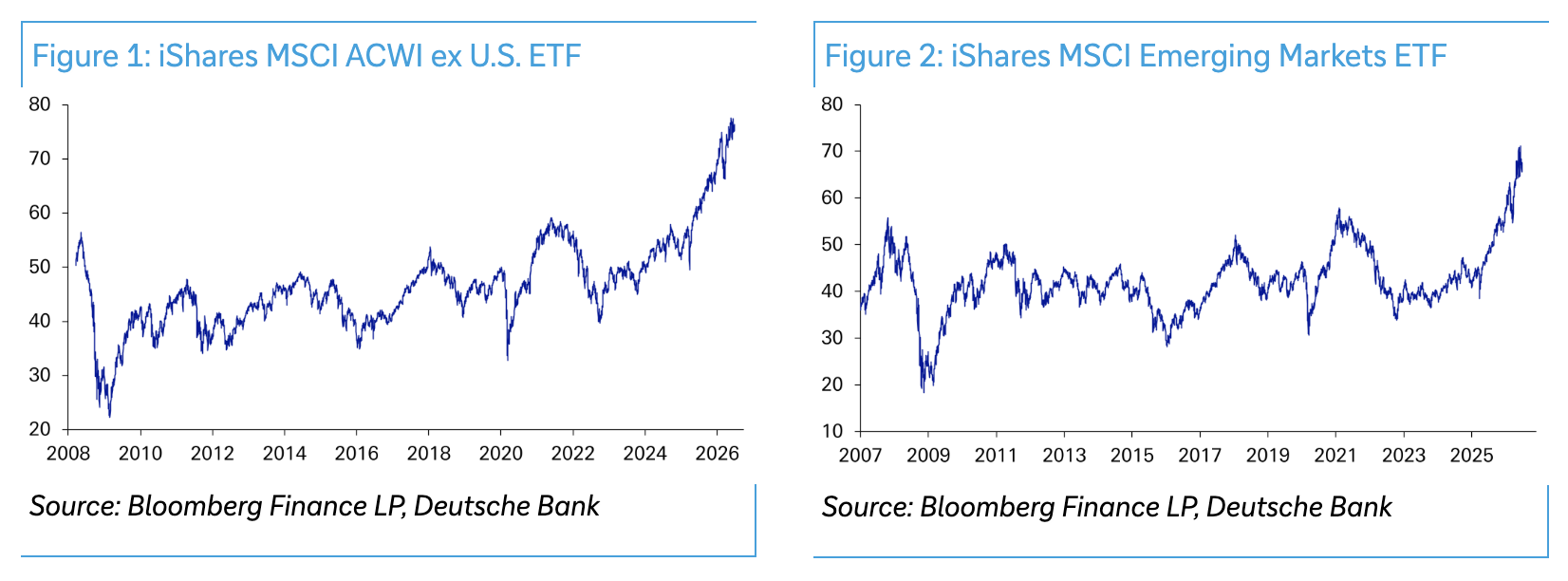

Jim Reid's latest Deutsche Bank "Chart of the Day"1 opens with a question that doubles as a verdict. For most of the past two decades, he writes, "owning equities outside the US has often made investors question whether diversification or valuations really matter." The numbers justify the frustration. The ex-US ETF sat "slightly lower in price terms at the start of 2025 than it was in June 2007, with the EM ETF similar." Over the same period, the S&P 500 nearly quadrupled. Two decades of broad diversification, functionally flat.

The explanation was structural. Ex-US indices carried heavy weights in what Reid describes as "old economy" sectors -- "financials, energy, materials and industrials, with less exposure to the mega-cap tech stocks that powered the S&P 500 through the 2010s." While US mega-cap tech compounded relentlessly through the decade, the rest of the world sat on sectors the market spent years penalizing.

The Shift That Changed the Calculus

That story is now running in reverse, and Reid maps the reversal through several converging forces. The geopolitical backdrop has pivoted hard toward defence and industrial self-sufficiency -- "the renewed focus on defence and industrial self-sufficiency is just one example," he notes, rerating precisely the sectors where rest-of-world and EM indices carry structural weight. AI capital expenditure is "spilling over into power, hardware and materials," once again benefiting the sectors EM indices have always overweighted.

Fiscal activism is accelerating the shift. Germany's stimulus is Reid's headline DM example, but the pattern extends inside the EM universe itself. In Mexico, Reid points to "a massive investment in traditional-economy rail infrastructure." European banks, "laggards for nearly 15 years, have massively re-rated on improved profitability." The US dollar, which ran roughly 40% from 2010 to 2024, may be plateauing: it fell by over 9% in 2025, its worst year since 2017, removing a persistent drag on unhedged returns for dollar-based investors.

The Concentration Twist

Here is where Reid sharpens the blade. The macro recovery thesis is real, but its actual engine is not what EM bulls have historically cited. "The outperformance of both indices has increasingly been driven by tech," he observes. The three largest names in both the EM index and the world ex-US index are TSMC, Samsung, and SK Hynix. Nearly 30% of the EM index is concentrated in those three companies. In the world ex-US index, the same trio accounts for nearly 10%.

The top-10 concentration data lands harder still. The world ex-US index holds 16.8% in its top 10 — modest by any measure. The EM index top 10 now accounts for 39.4%, "above the S&P 500 at 36.7%." The index that many advisors present as a global diversifier has a higher top-10 concentration than the index most associated with mega-cap risk.

Reid's conclusion is direct: "Somewhat ironically, buying an EM ETF today is effectively a large tech play. That may be positive or negative, but it means that a typical EM ETF looks very different from what many generalist investors might assume."

3 Key Takeaways for Advisors and Investors

1. The EM label no longer describes the underlying exposure.

With nearly 30% in three semiconductor and hardware names, the EM index carries a concentration profile that now exceeds the S&P 500. Advisors should audit EM allocations for tech overlap before positioning them as diversifiers.

2. The macro tailwinds are real but need accurate framing.

The recovery in ex-US and EM performance reflects a geopolitical rerating of old-economy sectors and AI capex spillover -- not a broad emerging markets growth renaissance. Client conversations should reflect that distinction.

3. The dollar is now a structural factor, not background noise.

After a 14-year bull run that acted as a persistent drag, a plateauing or declining US dollar meaningfully amplifies unhedged returns for dollar-based investors in international positions. Currency dynamics deserve a place at the portfolio construction table.

Footnote:

1 Reid, Jim, Henry Allen, Luke Templeman, and Raj Bhattacharyya. "DB CoTD: Is EM a Huge Tech Play?" Deutsche Bank AG, Thematic Research, 8 July 2026.

Copyright © AdvisorAnalyst