by AdvisorAnalyst.com Editorial Team

The AI trade runs on nerves. Every sharp pullback over the past few years has landed at a moment when investors started asking the same uncomfortable question: has the AI business model hit a tipping point?

In a June 15, 2026 note from the Deutsche Bank Research Institute, research analysts Luke Templeman and Galina Pozdnyakova come at that question from a fresh angle. Instead of arguing about AI's promise, they pull the S&P 500 apart, tech on one side, everything else on the other, and follow the money. What they find cuts against the prevailing mood.

"Amongst our key takeaways is that while tech dominance in the stock market is growing, other S&P 500 corporates offer solid fundamentals which means the bulk of companies in the index do not look overpriced," write Templeman and Pozdnyakova. "That should keep the potential fallout from any further AI disenchantment more contained than many currently fear."

The Financing Question Behind the Wobbles

So what set off the latest jitters? A shift in how the biggest AI spenders pay their bills. "The recent wobbles have also come as investors consider the financing methods of some the largest hyperscalers which have signalled they are ready to turn to equity issuance to invest in AI capacity," the authors write. Selling stock to fund capex tests the pecking order theory of financing. And it comes right as this year's AI related IPOs raised fresh doubts of their own.

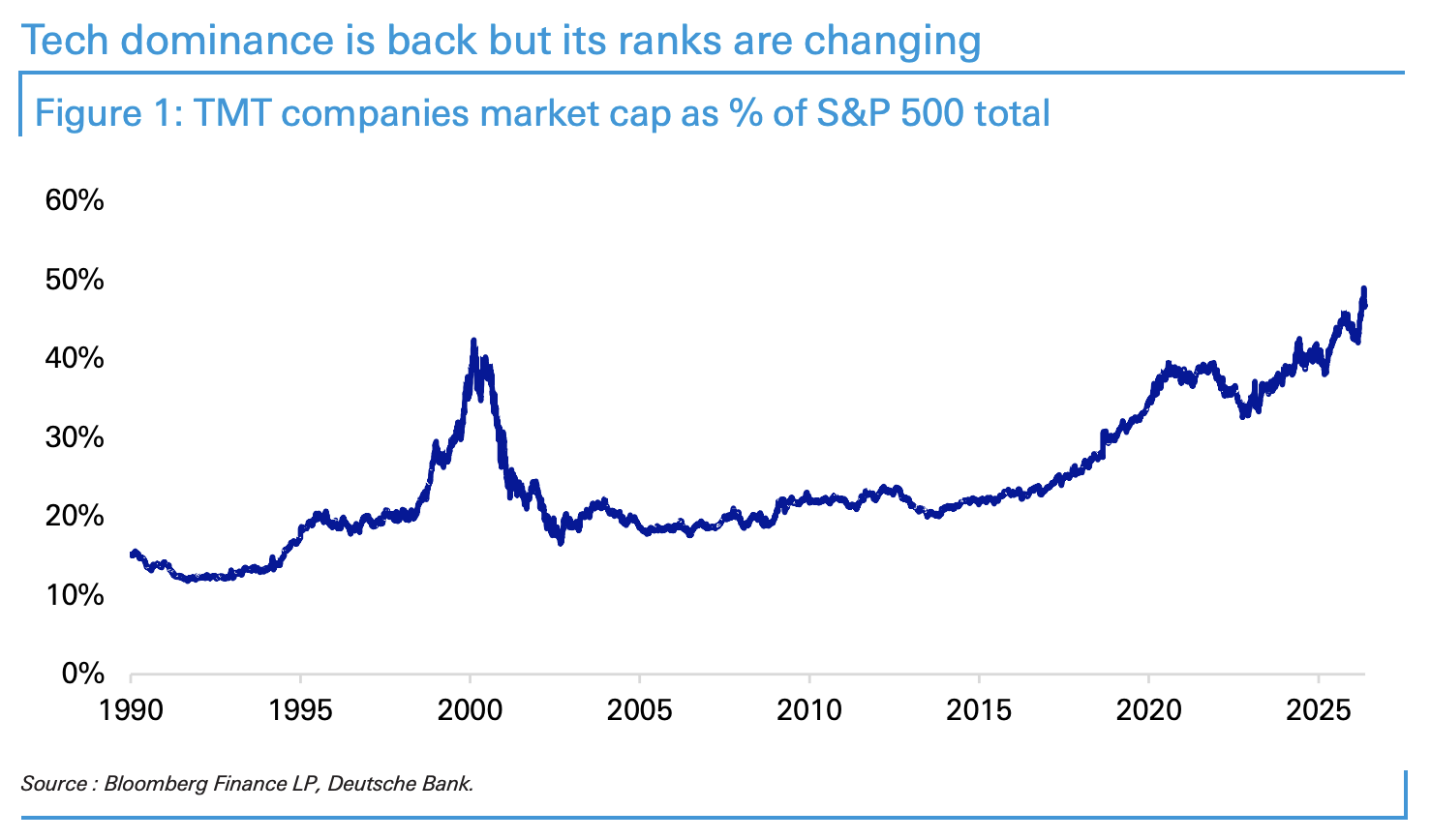

The timing stings. TMT companies now make up nearly half the S&P 500's total market cap, a level not seen since the dot com peak. "The run-up in the share of TMT companies' market cap relative to the S&P 500 total comes just as the biggest tech players that have propelled index fundamentals in recent years are expected to experience declines in free cash flow," the analysts write. "That comes on top of slowing sales growth for some which will weigh on their asset efficiency, particularly given their capex plans."

Here's why that matters. Tech's payouts have been the market's ballast for years, holding up even through covid when the rest of the index cut back. Now the report's forecasts show free cash flow for Alphabet, Amazon, Apple, Meta and Microsoft sliding through 2028 while asset turnover erodes.

Here's why that matters. Tech's payouts have been the market's ballast for years, holding up even through covid when the rest of the index cut back. Now the report's forecasts show free cash flow for Alphabet, Amazon, Apple, Meta and Microsoft sliding through 2028 while asset turnover erodes.

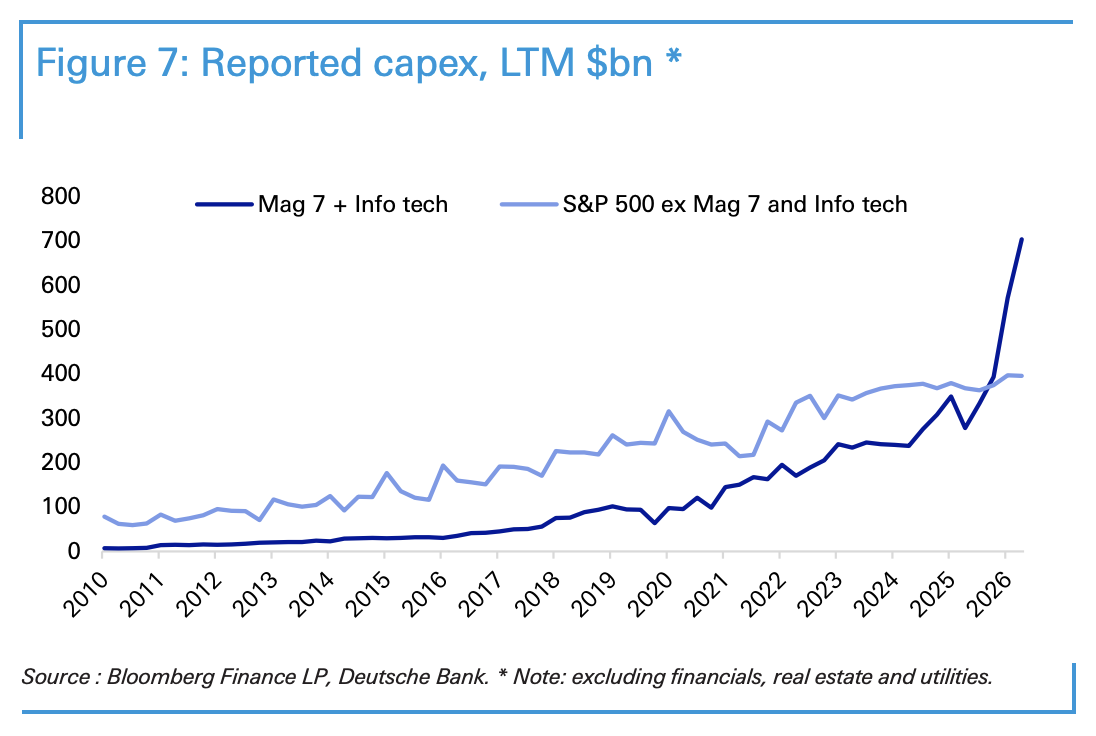

Tech Spends, Everyone Else Saves

One number tells the story: capex is up 876% for tech since 2019. For everyone else? Just 62%.

The rest of the index went the other way entirely. "Unlike tech companies, the rest of the S&P 500 corporates have been in cash-preservation mode, which is reflected in almost no new net borrowing in the last 12 months as well as a relatively slower increase in capex," write Templeman and Pozdnyakova.

That caution built a war chest. Non-tech cash piles have grown roughly 8% a year since 2019, beating inflation, and they dwarf what the Mag 7 plus info tech cohort holds. The authors don't expect the hoarding to last. "We believe this cash preservation is likely to change," they write. "Big M&A deals are already one of the signs that companies are looking to decrease their cash piles."

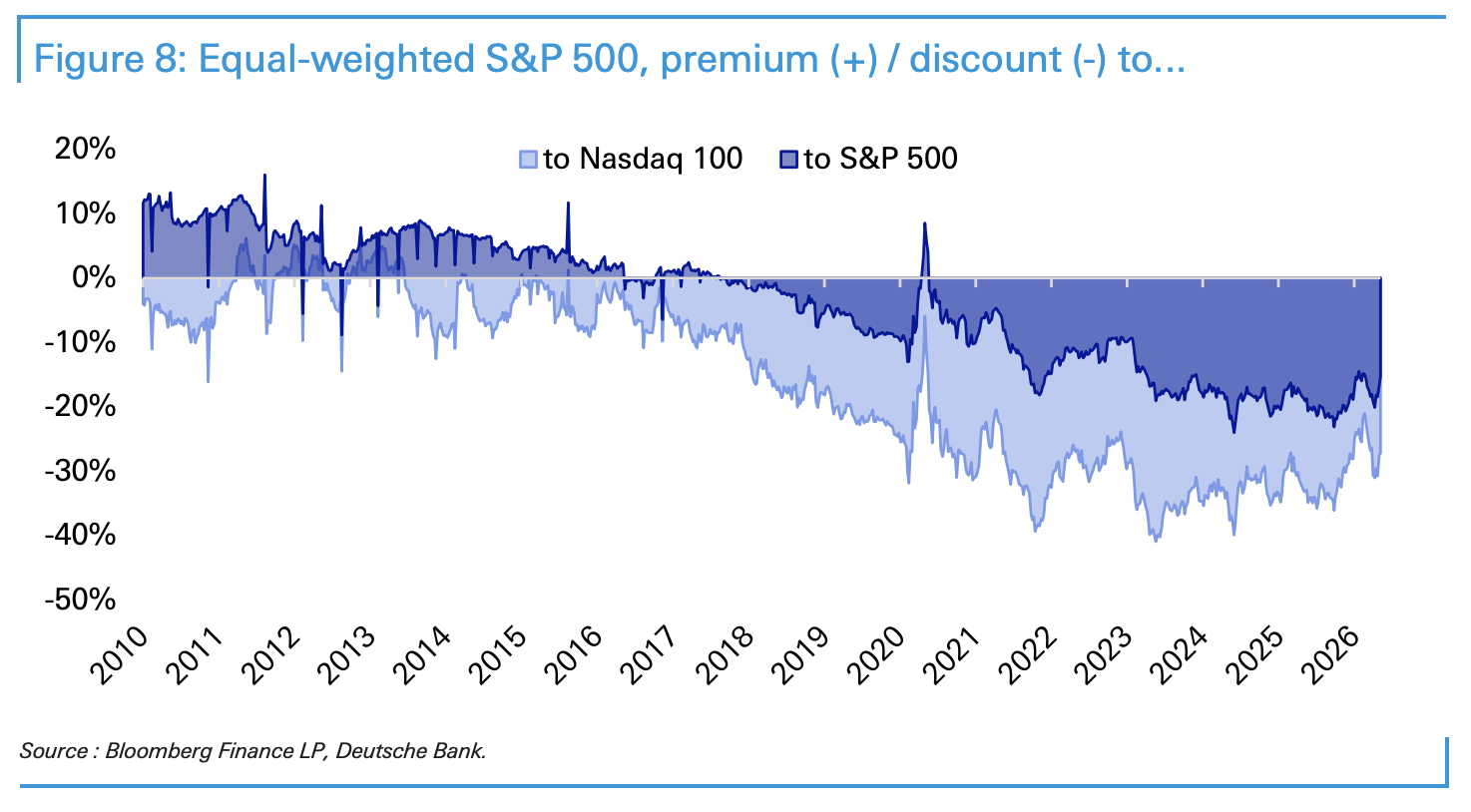

The Value Hiding in Plain Sight

The equal weighted S&P 500 trades at roughly a 15% discount to the cap weighted index, and 27% to the Nasdaq 100 on forward P/E. Sure, non-tech firms are expected to grow EPS just 13.2% in 2026 versus 23.7% for tech. But that still beats Europe at 11.2% and Japan at 10.5%.

"When we now look at large non-tech American corporates, there are strong signs of resilience," the authors write. "This leads us to expect them to increase their investing and payout activities in the coming few years."

Five Takeaways for Advisors and Investors

- Concentration risk is real but ring fenced. Tech's weight nears 50%, yet the fundamentals problem sits with the hyperscalers, not the broad market.

- Watch the financing shift. Hyperscalers issuing equity to fund AI capex signals strain on internal cash generation.

- The 876% versus 62% capex gap defines this decade. Tech spent aggressively while everyone else saved, borrowed nothing, and got stronger.

- The equal weighted discount is a flag worth watching. A 15% discount plus EPS growth ahead of Europe and Japan suggests the average S&P 500 name isn't overpriced.

- Expect the cash to move. Rising M&A points to non-tech corporates finally deploying reserves, a potential catalyst for market broadening.

Footnote:

Templeman, Luke, and Galina Pozdnyakova. Capital Allocation without Big Tech. Deutsche Bank Research Institute, 15 June 2026.

Copyright © AdvisorAnalyst.com