The question Goldman Sachs Asset Management says it now hears from advisors and institutions around the world is "not whether to invest in water, but how." That framing, from a team led by Isobel Edwards, Head of Sustainable and Impact Fixed Income Research, alongside co-authors Sebastian Gruhn, Jeff Possick, and Sebastiaan Reinders, signals something important: the water investment case has moved past the awareness stage and into portfolio construction.

The Demand Case Is Already Here

Water stress is not a projection. It is a present condition. Demand is surging from a growing global population, from agriculture, energy production, and manufacturing, and increasingly from the data centers powering artificial intelligence. The supply is finite. The infrastructure connecting the two is aging. The authors cite United Nations research classifying nearly three-quarters of the world's population as living in countries that are water-insecure or critically water-insecure.

What makes this a structural investment thesis rather than a crisis narrative is the capital response it demands. The World Economic Forum puts the total investment required to build resilient, sustainable, up-to-date drinking water and sanitation systems at $13.2 trillion by 2040. Annual investment would need to more than double from its current level of approximately $380 billion per year. Governments lead the funding at roughly 85% of annual spending, according to the World Bank, but the size of the task means private capital is essential.

A Three-Question Framework

GSAM structures its approach around three evaluative questions: Does the opportunity address potential downside risks? Does it enhance efficiency to improve margins? Does it provide access to secular growth? This framework is designed to help investors understand what is actually driving value in a given company or asset, rather than simply labeling it a "water play."

Fixed Income: The Broadest Entry Point

In GSAM’s view, the broadest water investment opportunity sits in fixed income. It extends beyond public utilities to corporates, governments, agencies, and state-owned enterprises issuing labeled green, blue, and social bonds alongside conventional instruments. Blue bonds, a more recent market development, expand eligible projects to marine ecosystems, coastal climate adaptation, and prevention of marine pollution. In 2025, an Italian multi-utility issued the country's first blue bond, a five-year private placement financing water network management, supply systems, and wastewater treatment. Globally, approximately 30% of water is lost before reaching customers due to leaks in distribution networks, giving that mandate concrete operational urgency.

GSAM's analysis finds that bonds eligible for a blue portfolio carry a higher aggregate credit rating than the global corporate aggregate index and a greater proportion denominated in US dollars than the broader green bond market. That combination produces distinct risk-return characteristics and potential currency diversification, not a repackaging of existing sustainable fixed income exposure.

Equity: Exposure Is Bigger Than Most Realize

On the equity side, GSAM's research using the MSCI ACWI IMI finds that 19% of total revenue across the index carries high or very high dependency on water. Food and beverage, pharmaceuticals, consumer products, electric utilities, energy producers, chemicals, metals and mining, and paper companies all fall into this category. Water-related questions on earnings calls remain elevated for utilities, materials, and energy producers even as broad sustainability questions trend lower.

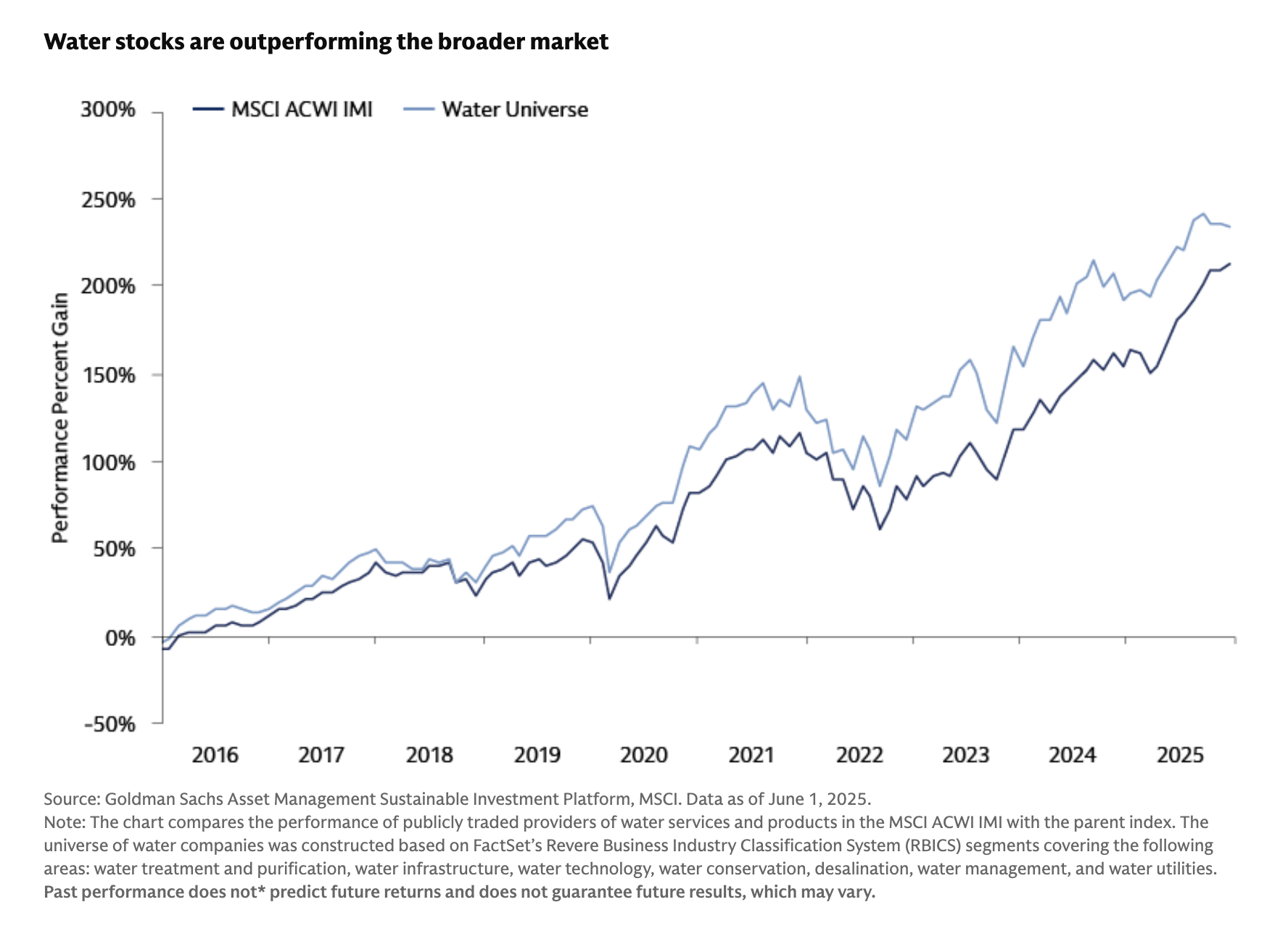

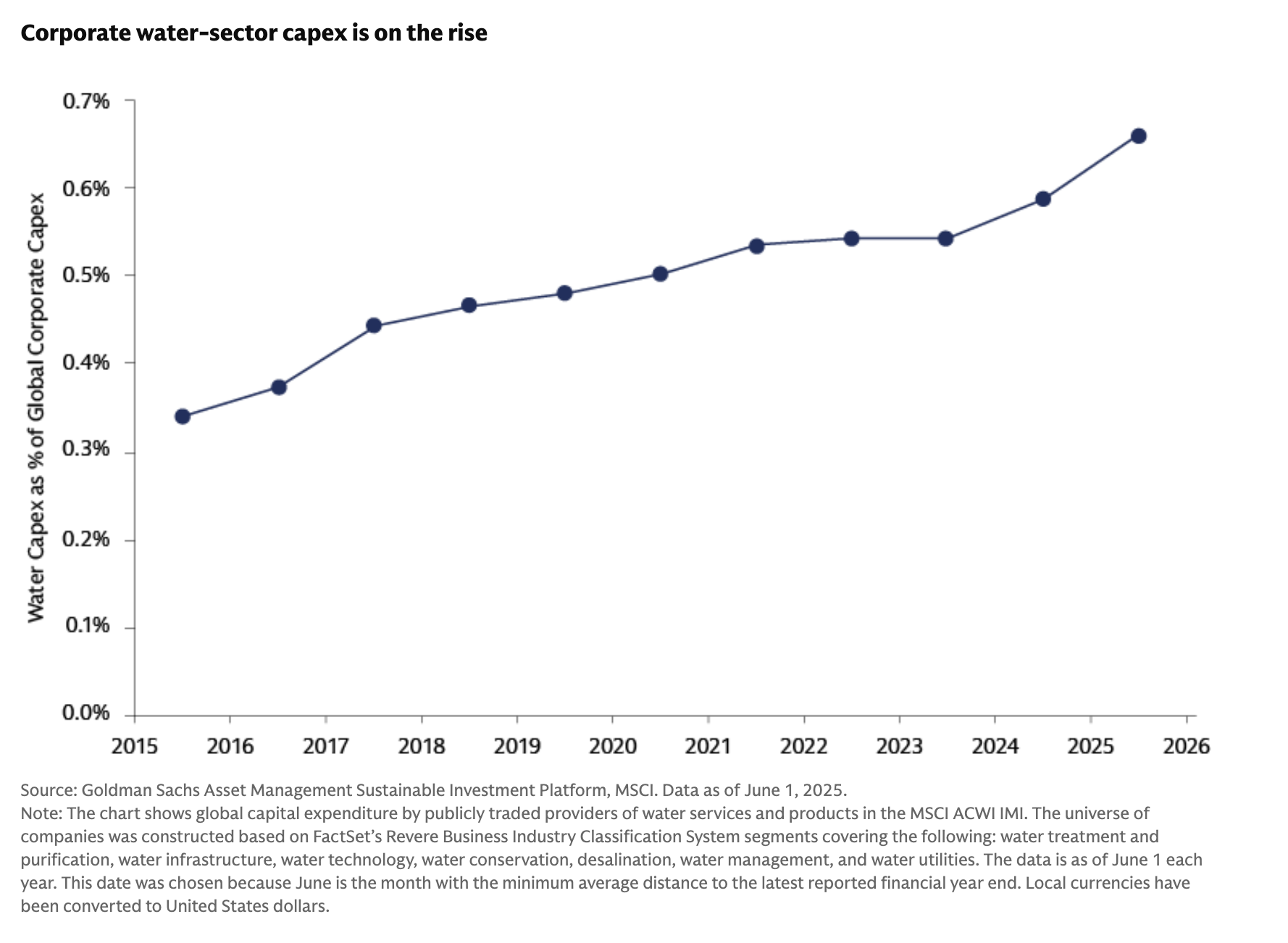

The report documents a decade of outperformance by publicly traded providers of water services and products within the MSCI ACWI IMI relative to the parent index, alongside a steady rise in corporate water-sector capital expenditure both in absolute terms and as a share of overall corporate capex.

The opportunity for equity investors is to identify which "pick-and-shovel" companies are winning a growing share of this spending. GSAM focuses on solution providers with a broad product range, a critical role in the value chain, and demonstrated ability to expand market share through organic growth and strategic acquisition.

The report also raises a counterintuitive diversification argument. Unlike clean energy, which is increasingly priced relative to AI sentiment given its role as a power source for data centers, water stocks have not been absorbed into that trade. The connection between AI and water stock prices is not yet a driver of share prices in the sector, which means allocating to water could increase diversification relative to tech-heavy sustainable portfolios.

Private Markets: The Growth Frontier

Private companies remain active across the water value chain and are staying private longer, the authors note, creating potential returns for private equity investors. One case study in the report involves an agricultural technology company whose software platform delivers real-time, AI-driven agronomic recommendations to permanent-crop operations including orchards and vineyards. The system saved farmers 132 billion gallons of water in 2024. Data-center developers, under pressure to offset their own water footprint, are beginning to finance installations at farms where operators cannot independently invest. This convergence of agriculture, AI, and water scarcity represents an early but structurally compelling intersection.

5 Key Takeaways for Advisors

- Water is a secular structural theme supported by irreversible demand drivers including population growth, AI infrastructure, agriculture, and decades of infrastructure underinvestment. It is not a cyclical rotation.

- Fixed income is the broadest and most accessible entry point, with green and blue bonds offering labeled transparency, above-average credit quality, and distinct currency exposure relative to mainstream sustainable benchmarks.

- Water revenue exposure inside existing equity portfolios is far larger than most advisors recognize. Nearly one in five dollars of global equity revenue carries high or very high water dependency, creating both risk management and thematic opportunity.

- The equity opportunity is concentrated in "pick-and-shovel" solution providers with broad product lines, critical roles in the water value chain, and consistent organic growth records rather than pure-play utility exposure alone.

- Water offers a meaningful diversification benefit within sustainable allocations precisely because it has not yet been priced as an AI story. Unlike clean energy, water stocks are insulated from AI sentiment swings, making the sector a potential stabilizer in sustainable portfolios.

Footnote:

Edwards, Isobel, Sebastian Gruhn, Jeff Possick, and Sebastiaan Reinders. "Finding Investment Opportunities in the Global Response to Water Stress." Goldman Sachs Asset Management, 22 Apr. 2026, am.gs.com/en-us/advisors/insights/article/2026/finding-investment-opportunities-in-water-stress.