by AdvisorAnalyst.com Editorial Team

Three years ago, artificial intelligence was a curiosity. Today it is a capital allocation decision. That distinction frames every argument in Morgan Stanley Investment Management's landmark Big Picture report, authored by Jitania Kandhari, Deputy CIO of the Solutions & Multi-Asset Group and Head of Macro & Thematic Research for Emerging Markets Equity.

The report's core premise is unambiguous: AI is not a sector. It is a full-stack capital cycle spanning every asset class, every layer of the technology stack, and every time horizon relevant to institutional portfolios.

The Flywheel Is Already Spinning

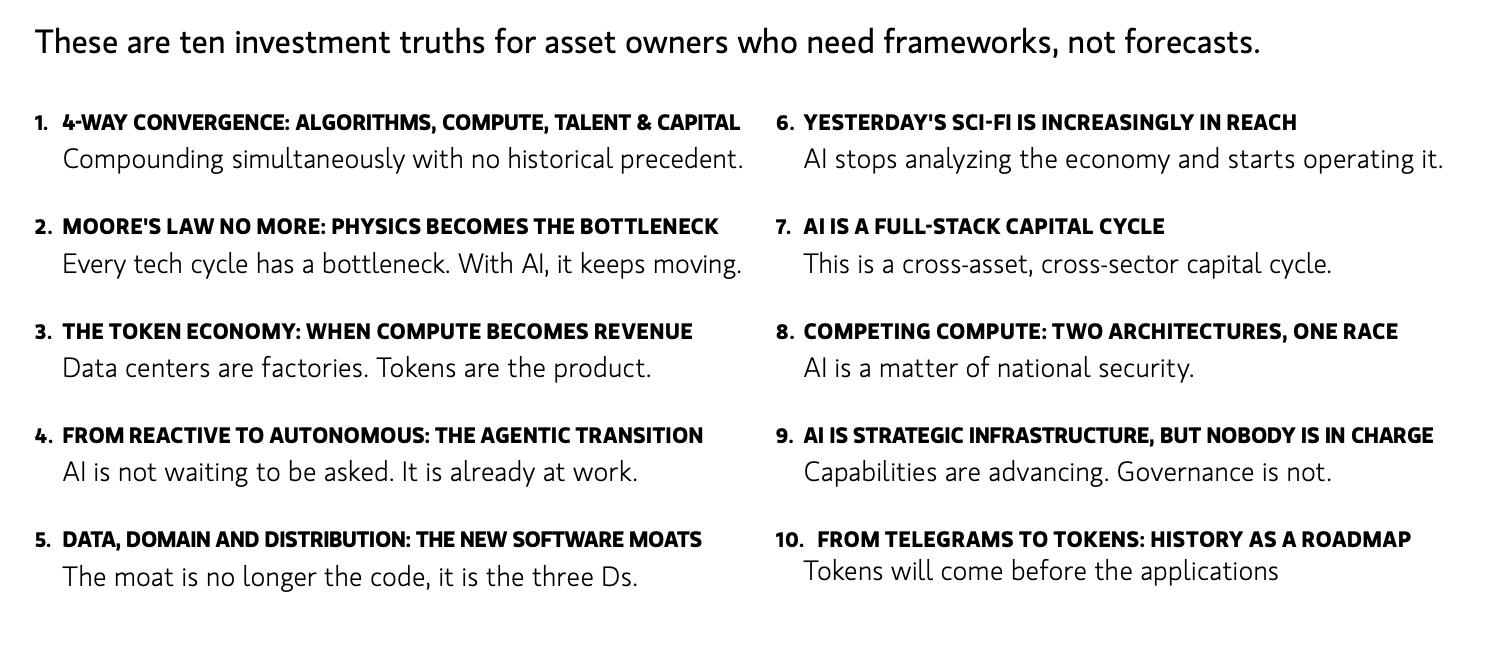

Kandhari's starting point is the 2017 Google Transformer breakthrough — the inflection that triggered a self-reinforcing convergence of algorithms, compute, talent, and capital. Approximately $2.3 trillion in AI capex has been committed since that moment, and the pace is accelerating. Token consumption — the basic unit of AI output — grew more than 10x in 2025 alone. AI capabilities are currently doubling every four months, implying systems 250 times more powerful by 2028 than exist today.

The report frames the destination clearly: Artificial General Intelligence — systems capable of performing any intellectual task a human can, across any domain, without task-specific retraining. Beyond AGI lies Artificial Superintelligence. The report cites Anthropic's CEO framing the near-term horizon as "a country of geniuses in a data center by end of 2027."

Physics, Tokens, and the New Unit of Revenue

Moore's Law is over. The report is direct: "The physics have run out." The bottleneck in AI infrastructure is no longer transistor density. It migrates — first chips, then power, then memory, then networking, then cooling. Memory is currently undersupplied through end of 2026, with AI demand expected to create 75–100 exabytes of incremental memory demand in 2027, doubling again in 2028.

What fills the performance gap is architectural innovation: chiplet designs, co-designed multi-chip systems, and silicon photonics replacing copper interconnects at scale. For investors, Kandhari's signal is precise: "The semiconductor story is no longer about who makes the best chip. It is about which layer of the supply chain becomes indispensable next."

The output of this infrastructure is the token. Data centers have crossed a threshold: they are no longer cost centers. They are production facilities, and their output is priced at dollars per million tokens — the AI analog to kilowatt-hours. The report identifies the single most critical efficiency metric in this economy: "tokens per watt, the measure of intelligence produced per unit of energy consumed."

The demand trajectory is non-linear. Generative AI established the baseline. Reasoning AI required approximately 1,000 times more compute. Agentic AI — systems that act, execute, and run continuously — requires approximately one million times more compute than the original conversational model.

Agents Are Already at Work

The transition from reactive to autonomous AI is not theoretical. Agent traffic on major internet infrastructure networks went near-vertical in early 2026. Some engineers are already managing four or more agents concurrently. Microsoft describes three modes of AI at work: simple chat, delegated tasks, and full digital workers with their own identities, tools, and workspaces.

The organizational implication is structural. "Over the next three years," the report states, "most individual contributors will involve managing groups of agents rather than executing tasks directly."

More consequentially, agentic systems are beginning to transact. Agent-to-agent commerce — autonomous purchasing, payment settlement, financial interaction — is already emerging as infrastructure, naturally favoring payment rails that require no human authorization and settle in seconds.

The New Moats: Data, Domain, Distribution

As AI commoditizes code, the durable competitive advantages shift. The report identifies three: Data, Domain, and Distribution. Unified data access allows agents to reason across all enterprise systems simultaneously. Domain expertise — compliance depth, implementation complexity, mission-critical workflow embeddedness — is not eroded by AI. It is deepened. Distribution, built over decades through network effects, cannot be replicated in days regardless of how capable the model.

The warning for incumbents is sharp: "The vendors who silo data behind export fees are not protecting a moat. They are likely accelerating their own displacement."

Two Architectures, One Race

The geopolitical dimension of AI cannot be separated from the investment thesis. Two distinct ecosystems are forming. The U.S. model is capital-intensive and innovation-driven, constrained primarily by power availability. The Chinese model, constrained by semiconductor export controls, has evolved into a low-cost, efficiency-focused parallel stack — leveraging surplus power, open-source ecosystems, and deep emerging market hardware partnerships.

The performance gap is closing faster than consensus expected. Despite spending only 18% of what American hyperscalers have invested, Chinese models now benchmark broadly in line with U.S. peers — with the reported performance lag narrowing to approximately one month. "Harnessing AI is becoming a matter of national security," the report concludes, noting that governments and defense establishments have moved from passive observers to active customers.

The Governance Gap — and Four Risks

Capabilities are advancing. Governance is not. Private companies are effectively setting global access policy for systems capable of identifying decades-old vulnerabilities in critical infrastructure, without government mandate or international framework. Half the enterprise market remains on legacy cybersecurity protection while AI-driven threats operate at machine speed.

The report identifies four risks investors must hold simultaneously. First, scaling laws may be flattening — more compute may no longer produce proportionally better models. Second, the gap between AI capability and economy-wide productivity remains unresolved. Third, agentic errors carry real consequences: unlike a hallucination in conversational AI, a wrong action in an autonomous workflow is a liability event with no established legal framework. Fourth, apparent diversification across the AI stack may be illusory — hyperscalers, labs, semiconductors, and cloud platforms are deeply correlated. A geopolitical shock or capex pullback does not affect one layer. It ripples through all of them.

History as a Roadmap

Kandhari closes with a structural historical parallel. Telegraph infrastructure collapsed per-message costs while volume grew 11-fold. The fiber overbuild of the late 1990s enabled search, social, streaming, and e-commerce — applications that did not exist when the cables were laid. "The applications that will consume the infrastructure being built today are still ahead of us. The companies that generate the greatest returns may not yet have been founded."

AI token costs fell 10x in 2025 alone. The adoption inflection that took fiber a decade may take AI two years.

Key Takeaways for Advisors and Investors

1. Think full-stack, not single-layer. The opportunity migrates as bottlenecks shift — from chips to power to memory to networking. Position frameworks to move with it.

2. Tokens are the new revenue unit. Compute capacity and revenue are now directly proportional. Infrastructure is the factory; tokens are the product.

3. Agentic AI changes the demand math permanently. Each phase of AI evolution has expanded the market rather than replaced it. Agentic systems require compute at a scale that resets every prior assumption about infrastructure sizing.

4. The moat is the three Ds. Data unity, domain depth, and distribution durability separate durable winners from AI-vulnerable incumbents.

5. Geopolitics is now priced into the AI stack. The U.S.–China compute race is strategic, not merely commercial. Strategic races, historically, run longer and attract more capital.

The infrastructure comes first. History says the applications that justify the buildout are not yet visible. That is the signal, not the risk.

Footnote:

1 Kandhari, Jitania. "Artificial Intelligence: Ten Investment Truths." Big Picture, Morgan Stanley Investment Management, 2Q 2026,

Copyright © AdvisorAnalyst.com