by Chris Ferrarone & Michelle Gibley, Schwab Center for Financial Research

Key takeaways

- The backdrop for global equities remains supportive in our view, driven by strong earnings growth stemming from increased capital spending from the business sector.

- The artificial intelligence (AI) investment cycle remains one of the primary growth drivers of global economic activity in 2026, but it is also now one of the market's most significant sources of dependency risk.

- We believe the path forward is still positive, but higher inflation, geopolitical turmoil, and policy uncertainty might lead to more frequent bouts of volatility.

- Looking through the second half of 2026, we anticipate a global equity market supported by solid earnings growth, while also facing higher concentration risk and a greater chance that inflation could disrupt returns.

Global economic activity has accelerated, with business investment being a key factor. Earnings are rising at a faster pace than last year, supported by a powerful capital expenditure cycle tied to AI and related infrastructure buildout. This combination of improving economic activity and strong earnings growth has historically been bullish for equities, helping to explain the general resilience of markets in the first half of 2026 in the face of geopolitical and inflation risks.

However, the same forces driving equities higher seem to be concentrating risk. Global earnings growth has become increasingly dependent on a relatively small set of companies tied to AI capital spending (capex). AI capex could continue to grow in coming months, but market leadership has narrowed significantly, with a small subset of stocks driving a disproportionate share of performance in the MSCI indexes for both developed and emerging markets.

Inflation has also re-emerged as a source of market risk. While recent pressure has been tied in part to the energy shock from the Middle East, broader geopolitical tensions, protectionist policy shifts, and large fiscal deficits may also contribute to a more inflation-prone environment than investors experienced over the last several decades.

Looking through the second half of 2026, we see an equity market supported by solid earnings growth, but one also facing higher concentration risk and a greater chance that inflation could disrupt returns. Global equities could continue to move higher if growth supersedes inflation pressure, but the shifting environment argues for deliberate diversification and risk management.

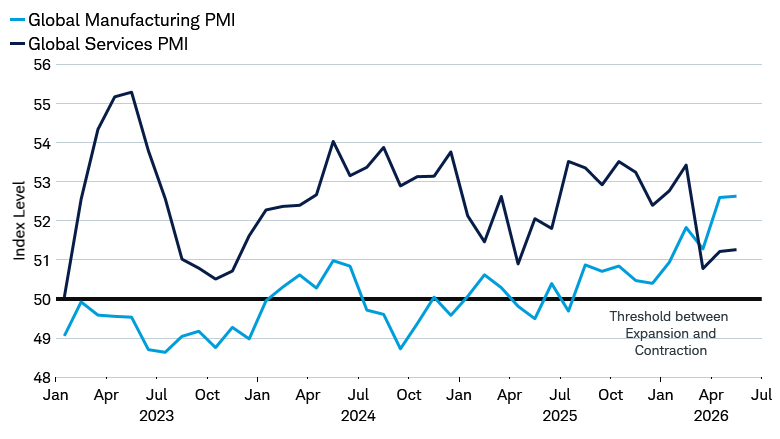

Growth is strengthening, but uneven

Manufacturing taking the lead

Source: Charles Schwab, S&P Global, and Macrobond data between 1/1/2023 and 6/2/2026.

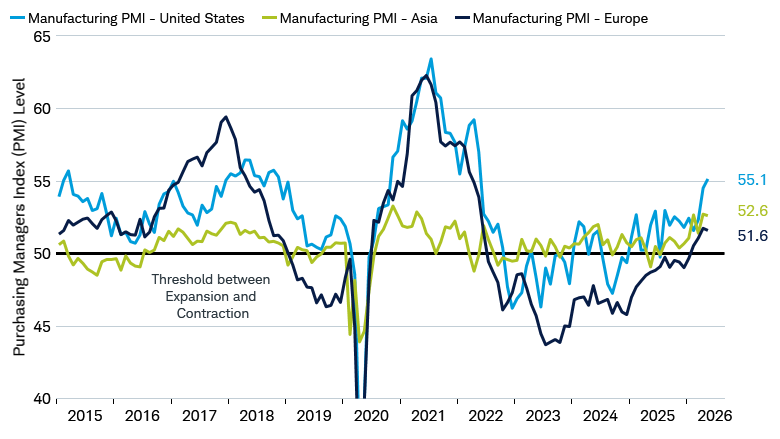

Regional differences in manufacturing

Source: Charles Schwab, S&P Global, and Macrobond data between 12/31/2014 and 6/2/2026.

Values in 2020 are truncated for visualization purposes, with a low of 36.1 for the United States, 43.9 for Asia, and 33.3 for Europe on 4/30/2020. Indexes are unmanaged, do not incur management fees, costs, or expenses, and cannot be invested in directly.

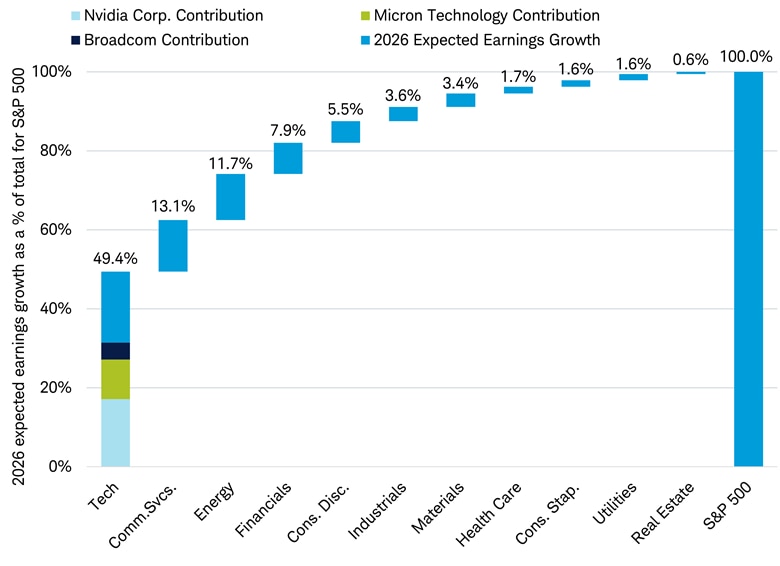

An earnings boom, but concentrated

While earnings growth across sectors for 2026 has improved, the contribution to aggregate earnings has been narrowly concentrated. A small group of companies tied to AI's innovation cycle, particularly semiconductors and digital platforms, are driving a large percentage of total earnings growth.

Distribution of total earnings growth in the S&P 500

Source: Charles Schwab, S&P Global, and FactSet data as of 5/27/2026.

Sectors are determined using the Global Industry Classification Standard (GICS®). Global Industry Classification Standard (GICS®) was developed by and is the exclusive property of MSCI Inc. (MSCI) and Standard & Poor's (S&P). GICS is a service mark of MSCI and S&P and has been licensed for use by Charles Schwab & Co, Inc.

Forecasts contained herein are for illustrative purposes only, may be based upon proprietary research and are developed through analysis of historical public data. All names and market data shown are for illustrative purposes only and are not a recommendation, offer to sell, or a solicitation of an offer to buy any security. Past performance is no guarantee of future results.

Extreme concentration can make markets more vulnerable. When a large share of earnings growth comes from a limited group of companies, market performance and valuations become more dependent on those firms continuing to meet high expectations. Concentration Risk. To the extent that index composition, earnings growth, or investor positioning becomes concentrated in a particular region, sector, group of industries, or individual securities, the broader index or asset class may be adversely affected by the performance of those securities, may be subject to increased price volatility and may be more susceptible to adverse economic, market, political or regulatory occurrences affecting that market, industry, group of industries, sector or asset class.

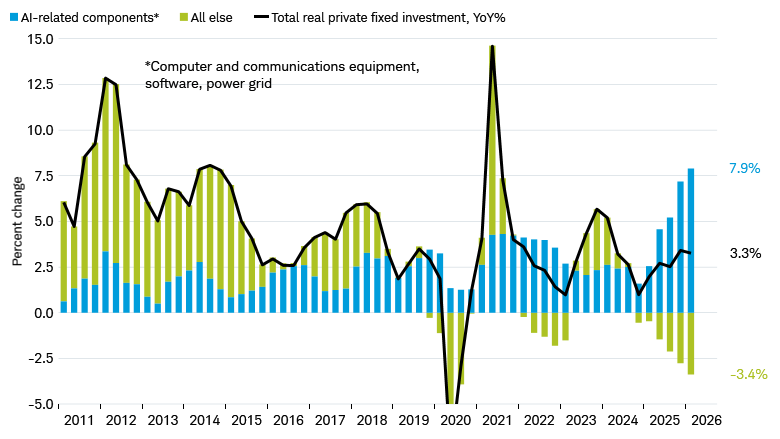

AI investment cycle: A stimulus, but also a dependency risk

Capital spending by hyperscalers, which are large-scale cloud-service providers with vast, global networks of data centers, has risen sharply and is expected to continue to grow along with AI-related investments by the broader business community. This spending is functioning as a macro-level stimulus supporting revenue growth, driving demand across supply chains, and boosting industrial and infrastructure activity.

AI dominating business investment

Source: Charles Schwab, U.S. Bureau of Economic Analysis, and Macrobond data from 3/31/2011 through 3/31/2026.

Values in 2020 are truncated for visualization purposes, reaching a low of -7.84% on 4/30/2020.

If returns on AI investment disappoint, market expectations will need to readjust if capital spending slows and financing conditions tighten. The potential impact could extend across the broader markets given the increased concentration and activity.

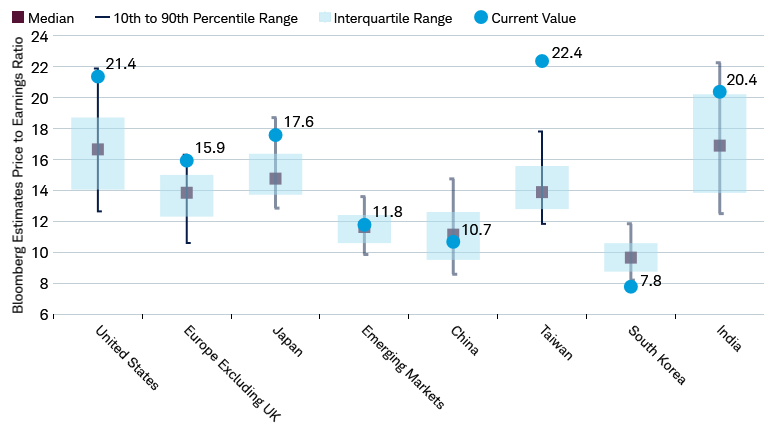

Valuations and expectations: Little margin for error

Valuations at the higher end of their 20-year range in most major markets

Source: Charles Schwab, MSCI, S&P Global, Bloomberg, and Macrobond data from 5/1/2006 through 5/29/2026.

Data for P/E estimates ranges is 20 years, from May 2006 to May 2026.

Country data reflects constituents of the MSCI Country Indexes For illustrative purposes. Chart is showing current valuation ratios relative to historical average and percentiles. Past performance is no guarantee of future results.

While higher profitability and structural growth may justify valuations above historical averages, our analysis indicates that market pricing appears to be discounting continued profit margin expansion and above-average earnings growth.

However, when valuations and earnings expectations are both elevated, especially after a long period of outperformance, downside risk may also increase. If current earnings expectations prove too optimistic, markets could reprice quickly. Today, many of the companies with the largest upward revisions to earnings estimates—primarily in the Technology and Communication Services sector—also carry large weights in the S&P 500 and MSCI Emerging Markets Index, which may leave less margin for error in those markets.

Investment implications and risks

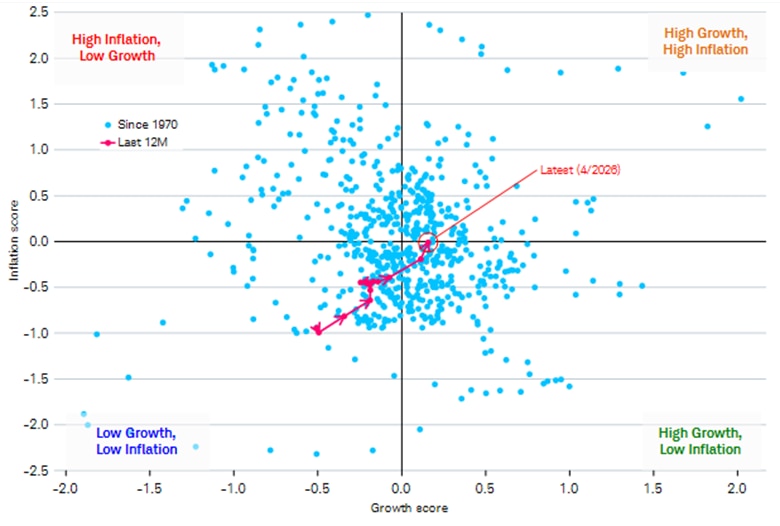

At the same time, our macro work suggests markets may be moving into a new phase in which both growth and inflation are running stronger than they were over the last several years.

U.S. growth and inflation regime indicator shifting to high growth/high inflation

Source: Charles Schwab, data from 1/1/1970 through 4/30/2026.

The red line connects the points of the 12 months between April 2025 to April 2026 and includes arrows to show the direction of movement.

The Inflation Score and Growth Score are based on a proprietary indicator using data from the U.S. Bureau of Labor Statistics, Federal Reserve, Organisation for Economic Co-operation and Development (OECD), Institute for Supply Management, S&P Global, U.S. Department of Labor, the U.S. Bureau of Economic Analysis, and the University of Michigan. Past performance is no guarantee of future results.

Historically, global equity returns have been positive in this phase with market leadership typically driven by higher-growth, cyclically oriented sectors. The U.S. and emerging markets have typically outperformed international developed markets in this phase, and our view is that could be the case as long as rising inflation does not upend growth. This remains a key uncertainty due to the conflict in Iran as well as broader geopolitical fragmentation. However, it is important to note that historical patterns are not reliable indicators of future results.

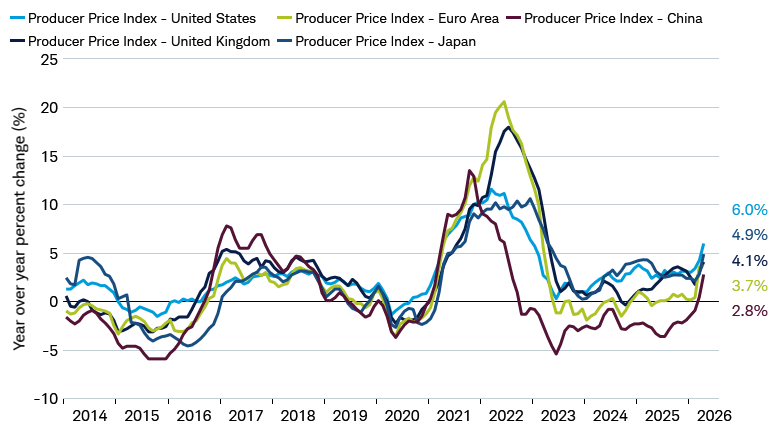

Macro risks: From "moderation" to "turbulence"

Production costs have risen lately

Source: Charles Schwab, U.S. Bureau of Labor Statistics, U.K. Office for National Statistics, Eurostat, Bank of Japan, China National Bureau of Statistics, and Macrobond data from January 2014 through April 2026.

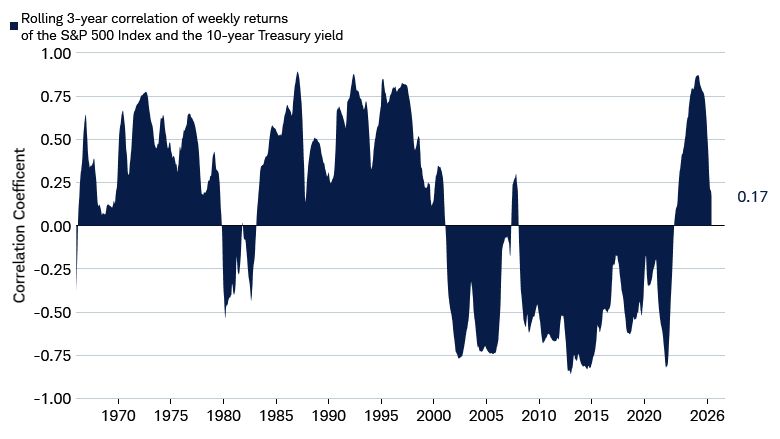

The recent energy shock reinforces our view that inflation may be more volatile than it was during the Great Moderation. That matters for markets. In recent years, stock and bond correlations have turned positive at times, raising questions about how consistently bonds can diversify equity and other risk exposures during periods of market stress.

Stock and bond prices have moved together recently

Source: Charles Schwab, S&P Global, U.S. Department of the Treasury, and Macrobond data from 1/1/1966 through 5/29/2026.

Correlation is a statistical measure ranging from +1 to -1 used to describe the relationship between two or more variables. A measure of +1 indicates that the variables are positively correlated and move in sync in both direction and magnitude. A measure of -1 indicates that the variables are negatively correlated and move in opposite direction and magnitude. And a measure of 0 implies no discernable relationship between the variables.

What to keep in mind moving forward

Equity markets may continue to move higher in this environment, although periods of volatility could become more frequent. The path forward appears increasingly dependent on a narrow set of drivers, which may leave markets more sensitive to disruption. Diversification across regions and sectors remains important.

Investors may want to emphasize earnings quality and durable, earnings-supported themes rather than chase speculative headlines. Concentration risk should also be managed to help avoid overexposure to single themes or narrow leadership groups, particularly if valuations become stretched.

Heather O'Leary, Senior Manager, Equity Research and Strategy, contributed to this report.

This material is intended for general informational and educational purposes only. This should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned are not suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decisions.

All expressions of opinion are subject to change without notice in reaction to shifting market, economic or political conditions. Data contained herein from third party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed.

Past performance is no guarantee of future results.

Investing involves risk, including loss of principal.

All corporate names and market data shown are for illustrative purposes only and are not a recommendation, offer to sell, or a solicitation of an offer to buy any security.

International investments involve additional risks, which include differences in financial accounting standards, currency fluctuations, geopolitical risk, foreign taxes and regulations, and the potential for illiquid markets.

Investing in emerging markets may accentuate this risk.

Commodity-related products carry a high level of risk and are not suitable for all investors. Commodity-related products may be extremely volatile, may be illiquid, and can be significantly affected by underlying commodity prices, world events, import controls, worldwide competition, government regulations, and economic conditions.

Fixed income securities are subject to increased loss of principal during periods of rising interest rates. Fixed income investments are subject to various other risks including changes in credit quality, market valuations, liquidity, prepayments, early redemption, corporate events, tax ramifications, and other factors. Lower rated securities are subject to greater credit risk, default risk, and liquidity risk.

The policy analysis provided by the Charles Schwab & Co., Inc., does not constitute and should not be interpreted as an endorsement of any political party.

Concentration Risk. To the extent that an underlying strategy is concentrated in the securities of issuers in a particular market, industry, group of industries, sector or asset class, the strategy may be adversely affected by the performance of those securities, may be subject to increased price volatility and may be more susceptible to adverse economic, market, political or regulatory occurrences affecting that market, industry, group of industries, sector or asset class.

Diversification and asset allocation do not ensure a profit and do not protect against losses in declining markets.

Indexes are unmanaged, do not incur management fees, costs, and expenses and cannot be invested in directly. For more information on indexes, please see schwab.com/indexdefinitions.

The Schwab Center for Financial Research is a division of Charles Schwab & Co., Inc.

Source: Bloomberg Index Services Limited. BLOOMBERG® is a trademark and service mark of Bloomberg Finance L.P. and its affiliates (collectively "Bloomberg"). Bloomberg or Bloomberg's licensors own all proprietary rights in the Bloomberg Indices. Neither Bloomberg nor Bloomberg's licensors approves or endorses this material, or guarantees the accuracy or completeness of any information herein, or makes any warranty, express or implied, as to the results to be obtained therefrom and, to the maximum extent allowed by law, neither shall have any liability or responsibility for injury or damages arising in connection therewith.

0626-SXXC