There is a quiet crisis in modern advice.

Not a crisis of products. Not a crisis of platforms. Not even a crisis of performance.

A crisis of identity.

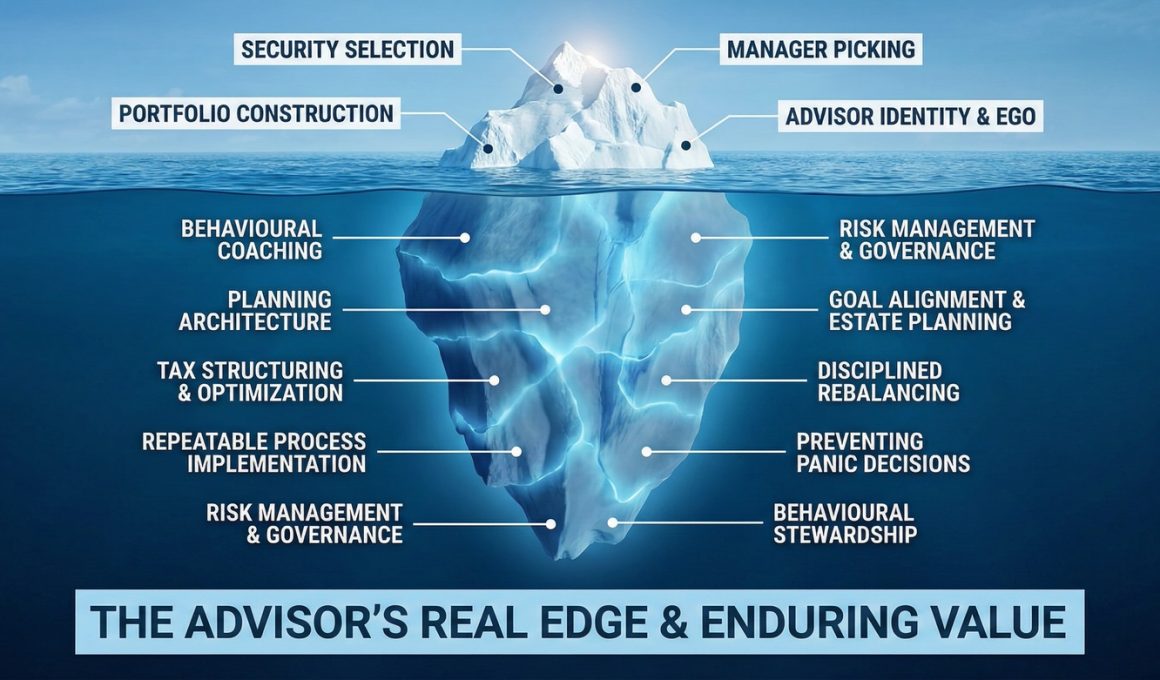

Because in a world where portfolios are increasingly commoditized, the investment advisor’s real defensible edge is no longer security selection. It is behavioural coaching, planning architecture, tax structuring, and the implementation of a repeatable process that clients can actually stick with in real life.¹

And yet, many advisors continue to cling to the idea that their edge lives in picking managers or constructing “their” model.

This is not a technical problem. It is a behavioural one.

I. The Real Edge: Not the Stock Picker, but the System Architect

For diversified public-market portfolios, asset-class exposure is widely available and competitively priced. As research from Russell Investments emphasizes, the durable value of advice increasingly comes from behavioural coaching rather than product selection.²

Russell frames it plainly in its research on advisor value: behavioural coaching is one of the largest contributors to what they describe as "advisor value.”³ In volatile markets, the incremental value often comes from keeping clients invested, rebalancing when it feels uncomfortable, and preventing panic selling or performance chasing.

In other words, the advisor’s edge is not the instrument. It is the intervention.

Other industry research reinforces the same conclusion. Expanding the advice value proposition “beyond portfolio performance” toward holistic planning builds trust and deepens client relationships.⁴ Coordinating goals, tax strategy, debt, retirement income, estate planning, and risk management creates structural value that no single fund can replicate.

Tax-aware implementation alone — asset location, withdrawal sequencing, product structure — can materially improve after-tax outcomes.⁵

And process matters. A disciplined Investment Policy Statement, documented rebalancing bands, and governance rules mitigate both client and advisor biases.⁶ As one white paper warns advisors directly, “Do not continue to let behavioural biases impact portfolio construction.”⁷

The real edge is being the architect and behavioural steward of the system — not the stock picker inside it.

II. Why Advisors Resist One-Ticket Solutions

If this is true, why the reluctance toward model portfolios or dynamic multi-asset solutions?

The resistance is not technical. It is psychological.

Model portfolios are increasingly described as “a must-have in [the] advisor arsenal.”⁸ They free advisors to focus on client relationships and planning. Yet adoption remains uneven.

Why?

1. Identity and Ego

Many advisors were trained to believe that portfolio construction defines their professionalism. Outsourcing that function feels like surrendering their core craft. Behavioural bias research confirms that overconfidence is common in financial professionals.⁹

In fact, roughly 65% of advisors in one survey believed their portfolio management skill could help clients outperform the market.⁷

That belief may feel empowering. It may also be statistically fragile.

2. Fear of Commoditization

In a fee-transparent environment, advisors worry that if the portfolio is outsourced, clients will ask: “So what am I paying you for?”10

The instinctive response is to make the portfolio visibly “custom,” even if the customization is operationally inefficient.

But visibility is not the same as value.

3. Loss of Control

Delegating dynamic allocation decisions to a centralized model team can feel like relinquishing control. Russell Investments notes that model portfolios allow advisors to focus on “what matters most.”11

Yet behavioural biases such as recency and availability bias — particularly following a bad product experience — can make advisors distrust delegated solutions.⁶

The paradox: the very biases advisors help clients overcome can govern their own professional decisions.

4. Business Frictions

Compensation grids, platform governance, and legacy books create inertia. Advisors are “flocking to model portfolios” in part because of efficiency and scalability, but migration requires operational effort and short-term trade-offs.¹²

Change is costly — psychologically and commercially.

5. Narrative Risk

When the portfolio story belongs to the manufacturer, the advisor’s “I built this” narrative fades. That feels like a loss of differentiation.⁸

But differentiation based on visible construction may not be defensible in a world of low-cost beta and institutional-grade models.

III. The Advisor as Behavioural Subject

The deeper irony: many advisors cling to “my way is optimal” because of the same biases they explain to clients.

Behavioural finance literature identifies overconfidence, confirmation bias, status quo bias, and sunk-cost effects as powerful drivers of portfolio decisions.⁹

Advisors, like all humans, remember wins more vividly than losses. They seek confirming evidence. They resist abandoning models they have spent years refining. And they fear that if a new outsourced solution underperforms temporarily, clients will blame the change.⁷

Humans need coherent identity narratives. “I select investments” is simple and flattering. “I orchestrate outsourced risk management, planning, tax optimization, and behavioural discipline” is more accurate — and less intuitive.¹³

Meanwhile, research consistently shows that clients value trust, peace of mind, and life-outcome alignment more than marginal benchmark outperformance.¹⁴ ¹⁵

There is a persistent mismatch between what advisors think clients value and what clients actually value.

And that mismatch sustains the ego trap.

IV. What Actually Holds the Weight

The distinction between surface differentiation and foundational strength is not unique to advisory practice. It is visible in any durable structure.

Consider the difference between a building’s appearance and the engineering beneath it. Architectural flourishes, glass facades, and aesthetic design may define how the structure is perceived. They attract attention. They signal distinction. They create identity.

But they are not what keep the building standing.

Load-bearing columns, foundational depth, material integrity, and structural redundancy determine whether the building survives stress. When external forces arrive — wind, weight, time — the integrity of the unseen components becomes decisive.

Advisory practices operate under the same principle.

Portfolio construction, tilts, tactical shifts, and manager selection are visible. They are tangible. They are easily narrated to clients and prospects. They create the sense of craftsmanship.

But they are not what ultimately determines whether clients achieve their goals.

Behavioural governance, disciplined rebalancing, tax-aware structuring, and a repeatable decision framework form the load-bearing system of an advisory relationship. They are less visible, harder to market, and often under-appreciated in calm markets. Yet they are precisely what prevent structural failure when volatility tests conviction.

In rising markets, almost any structure appears stable. It is only under stress that weaknesses are exposed.

If advisors prioritize visible differentiation at the expense of process discipline, they are refining the exterior while neglecting the engineering. Over time, that imbalance becomes consequential.

The real question is not whether a portfolio looks distinctive. It is whether the advisory system can endure turbulence without clients abandoning it.

Foundations are rarely glamorous. But they are what carry the weight.

Is the foundation behavioural governance and repeatable process — or is it performance theatre?

V. Reframing the Edge

The path forward is not to attack identity. It is to expand it.

The conversation might sound like this:

- Your edge is not that your 60/40 looks slightly different.

- Your edge is designing the overall strategy and keeping clients aligned with it through cycles.

- Outsourcing the portfolio engine upgrades the factory so you can focus on architecture, tax, governance, and behaviuor.¹²

- In a fee-transparent world, the most defensible value is a repeatable process and better real-world decisions over 10–20 years.¹

This framing does not diminish the advisor. It elevates the role.

It shifts the narrative from craftsman of components to steward of outcomes.

Conclusion: The Quiet Competitive Advantage

The durable competitive advantage in advice is not brilliance in security selection.

It is:

- Preventing clients from making catastrophic decisions.

- Structuring tax-aware withdrawals.

- Aligning capital with life goals.

- Building governance rules that survive volatility.

- Communicating consistently through uncertainty.

It is designing a system that works in real life.

The argument here is that sustainable financial architecture must rest on secure foundations rather than cosmetic scalability, sustainable advisory practice must rest on behavioural discipline rather than performance theatrics.

The advisor’s real edge is not what they pick.

It is what they prevent. What they structure. What they steady.

And most importantly — what clients are able to stick with when it matters most.

Footnotes:

- AdvisorAnalyst.com

- Russell Investments. “Value of an Advisor: B is for Behavioral Coaching.” July 2024.

- Russell Investments. “Value of an Advisor: Behavioral Coaching.” 2024.

- CSI. “Expanding the Advice Value Proposition: Go Beyond Portfolio Performance to Earn Clients’ Trust.”

- Snap Projections. “How Financial Advisors Can Show Value & Positively Impact Their Clients’ Lives.”

- Mitigating the Impact of Advisors’ Behavioral Bias. Cerulli, 2022.

- Investments & Wealth Institute. “Do Not Continue to Let Behavioral Biases Impact Portfolio Construction.”

- Broadridge Financial Solutions. “Why Model Portfolios Are a Must-Have in Advisor Arsenal.”

- AnalystPrep. “Influence of Behavioral Factors on Portfolio Construction.”

- CRM3 and fee transparency.

- Russell Investments. “Why Use Model Portfolios? So Advisors Can Focus on What Matters Most.”

- SmartAsset. “Why Advisors Are Flocking to Model Portfolios.”

- Purpose Built Financial Services. “Financial Success: The Behavioral Coaching Advantage.”

- eMoney Advisor. “How to Illustrate the Value of Financial Planning.”

- Covenant Wealth Advisors. “Value of a Financial Advisor: What You Need to Know.”

Copyright © AdvisorAnalyst.com