by Carl Tannnenbaum, Chief Economist, Northern Trust

By Carl Tannnenbaum

We just closed another banner year for asset prices. The S&P 500 was up 16% in 2025, and many overseas exchanges saw gains of more than 25%. Bond prices rose, and most housing markets held onto high values. There were even some signs of recovery in commercial real estate.

This has generated a lot of wealth, and a lot of what economists call wealth effects. The concept is simple: people whose net worth is rising tend to spend more. Calculations from Moody’s suggest that U.S. consumers will spend an extra five cents for every incremental dollar of equity gain, and an extra seven cents for every dollar of appreciation in the price of their home.

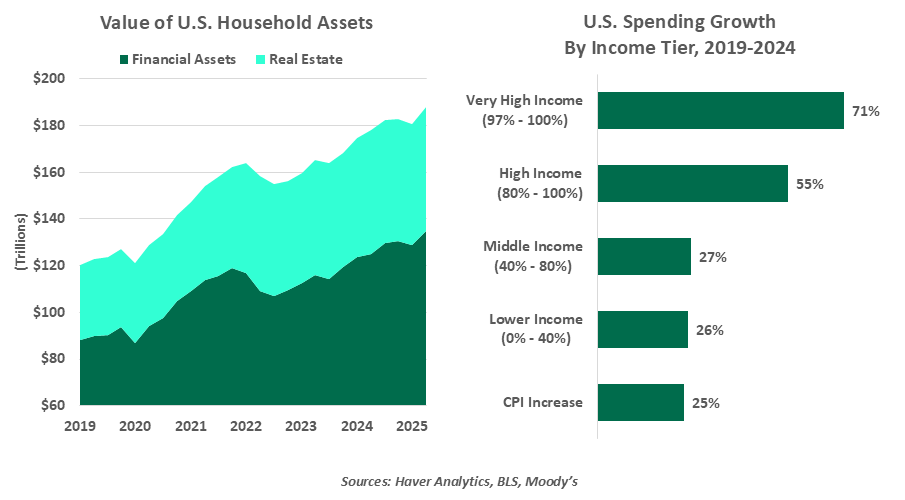

Over the past two years, U.S. households have seen their financial assets rise by $19 trillion and their home values increase by $4 trillion. Applying the wealth effects cited above, these conditions would increase personal consumption by more than $1 trillion. This would be enough to boost U.S. economic growth by 0.5% per year, a substantial increment.

Market gains have been an important foundation for economic gains.

American consumers also aid global growth through their consumption of imports. With household spending in many other parts of the world limited, demand from the U.S. has been an important source of support for overseas economies.

Because upper-income households are more likely to own stocks and property, they have generated more wealth effects than lower-income households. This is among the factors in the growing divergence in spending gains that can be clearly seen in data from retailers and credit card providers.

With the U.S. labor market losing steam, growth in wages is likely to diminish. This makes consumption more dependent on wealth effects derived from investments.

Last year’s equity gains have raised concerns that some stocks are at the upper edges of their valuation ranges. Some observers have suggested that bubble-like conditions are forming. Any correction in asset prices would reduce spending by the cohorts whose consumption has been critical to sustaining economic growth. In this way, the ability of AI-related investments to hold their values may be critical to staying out of recession.

Economic developments have an important influence on markets, but the same is true in reverse. Sustaining wealth, and wealth effects, may be critical to continued expansion.