by Avi Lavi, Chief Investment Officer—Global and International Value Equities, AllianceBernstein

Value stocks have bounced back with gusto outside the US. But can it last?

While the AI-driven rally in US mega-cap growth stocks grabbed attention in 2025, a very different story was unfolding far from Wall Street. Outside the US, from Europe to Japan, value stocks shed their perennial underdog status to stage a dramatic recovery—one that we think may just be getting started.

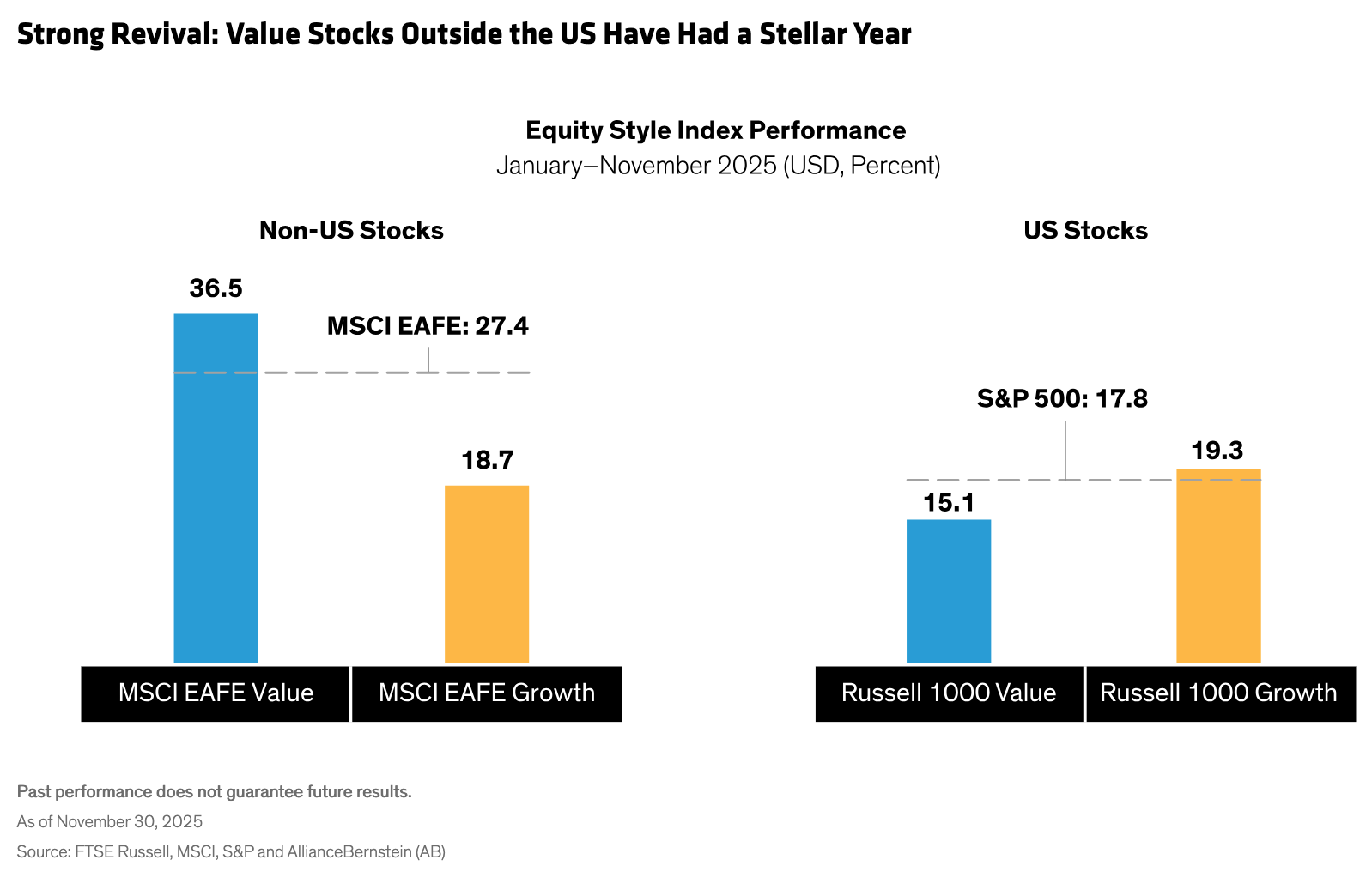

Global equity markets were full of surprises this year. Japanese and European stocks outpaced US peers. The MSCI EAFE Value Index of non-US equities surged by 36.5% through November (Display) in US-dollar terms, outperforming the MSCI EAFE Growth and the broad index. It was a mirror image of the US market, where growth stocks remained on top.

What’s Fueled the Value Recovery?

Several catalysts helped awaken value stocks, which began the year with exceptionally cheap valuations: First, companies in the value universe generally delivered earnings growth above expectation. Second, key value-oriented industries performed especially well, including European banks—as a steep yield curve buoyed profitability—and defense. Third, Asian corporate governance reforms are gaining traction.

In Europe, regional defense spending has increased amid heightened geopolitical tensions related to the Russia-Ukraine war and uncertainty over the US defense umbrella. EU defense spending rose by 19% in 2024 to €343 billion, or 1.9% of GDP, according to the European Council. The North Atlantic Treaty Organization is pressing its members to allocate at least 3% of GDP for defense budgets over the coming years, which could add another €220 billion a year to European military spending.

That translates to a big business boost for large, regional defense contractors, which can support stable cash flows and dividend payouts. These companies are prominent members of the value cohort.

Asia’s Corporate Governance Catalyst

Meanwhile, a new culture of corporate governance reform is taking root across Asia. China, South Korea and Japan are pushing reforms to boost shareholder value. In Japan, regulators are encouraging companies to reduce cross-shareholdings and deploy hoarded cash to boost operating leverage and streamline balance sheets. These moves could prompt a recovery in select Japanese companies with attractive valuations and a clear path to improve profitability.

China, too, is pressing companies to improve governance via the 2024 nine-point guidelines. These moves have helped lift profitability, dividends and buybacks to record highs. South Korean initiatives are in full swing through the “value up” program, which aims to incentivize improved capital management and operating performance. The goal: to boost valuations in a South Korean market that has had an exceptionally high proportion of cheaply valued stocks for years.

Is There More Room to Run?

After such a strong year, it’s natural for investors to question the staying power of non-US value stocks. We think there are good reasons to believe that the trend can continue.

First, the catalysts above are long-term trends that should continue to evolve. Defense spending in Europe is being driven by seismic geopolitical shifts that aren’t going away. Corporate governance reform is a multi-year process; while policy-driven changes can be erratic, we expect developments in Asia to create a virtuous circle, as more companies discover the benefits of cleaning up their businesses for shareholders.

Second, we’re seeing signs of other value-friendly themes developing. Examples include rising demand for commercial aircraft, a recovery in depressed agricultural commodity prices and the recovery of healthcare R&D spending from post-pandemic pressures. These trends support select opportunities in value-oriented companies with healthier businesses than perceived.

Third, new forces could propel value market segments that haven’t yet rebounded. For example, a continued weakening of the US dollar could support emerging-market stocks, which have not yet fully participated in the value rally.

Valuations Are Still Attractive

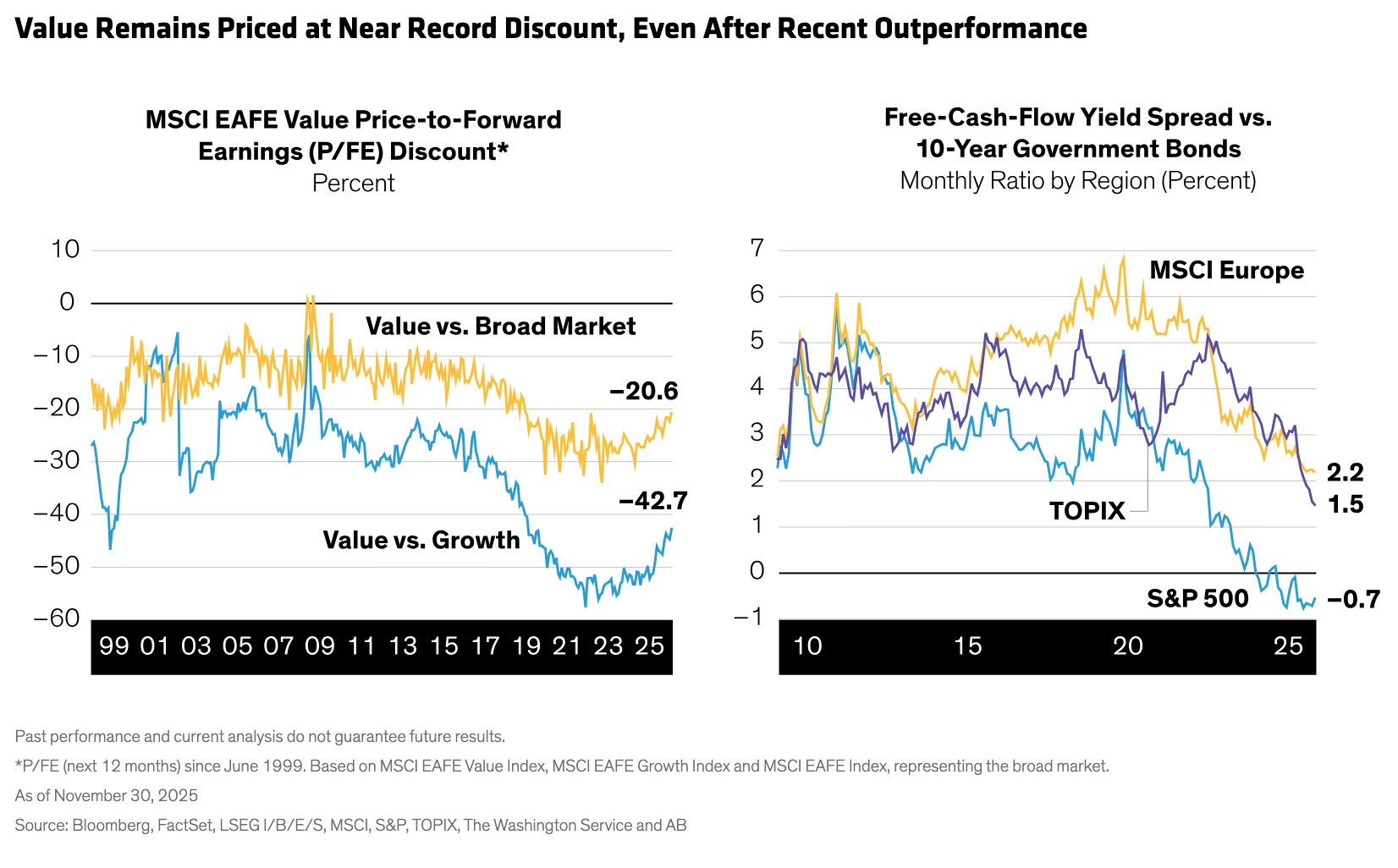

Even after this year’s rebound, ex-US value stocks still offer attractive discounts for investors by several measures. The MSCI EAFE Value’s price-to-forward-earnings ratio trades at a discount of 43% to growth stocks and 21% to the broader market (Display).

Free-cash-flow (FCF) yields also tell a compelling value story. We believe the FCF yield is an important indicator of whether a company is undervalued or overvalued based on its cash-generating ability. Our research shows a widening gap between FCF yields and government bond yields in the US versus Europe and Japan, indicating stronger compensation potential for risk-taking and better value opportunities. US equities have a negative real FCF yield spread versus Treasuries, signaling stretched valuations.

As we see it, the FCF yield analysis bolsters the case for allocating to value equities outside the US, particularly at a time of elevated market concentration in the US and increasing questions about the fragility of AI-driven market conditions.

Markets are fraught with risk as we enter 2026. That’s why a selective and risk-aware approach remains paramount. We think investors should search for value opportunities in three areas: companies undergoing positive changes, businesses with underappreciated sustainable competitive advantages and firms that benefit from improving industry competitive dynamics.

After years of unforgiving market conditions, disciplined value investing is starting to pay off. It’s not too late to diversify your equity allocation by increasing exposure to value stocks around the world with compelling recovery stories that represent powerful return potential.

The MSCI data may not be further redistributed or used as a basis for other indices or any securities or financial products. This report is not approved, reviewed or produced by MSCI.

About the Author

Avi Lavi was appointed Chief Investment Officer of Global and International Value Equities in March 2016 and has also been Portfolio Manager for Global Research Insights since May 2016. He has been a member of the Cross Border team since early 2012. Previously, Lavi served as co-CIO of Global Value Equities (since July 2014) and global director of Value Research (since early 2012). From 2006 to 2012, he was CIO of UK and European Value Equities, and director of research for UK and European Value Equities from 2000 to 2006, during which time he helped establish AB’s first research operation based outside the US. Lavi joined the firm in 1996 as a research associate for utilities and expanded his coverage in 1998 to include oil and gas, covering these industries on a global basis. He subsequently became a senior analyst and sector leader for energy research. Lavi was previously an assistant controller at the State of Israel Economic Offices in New York. Prior to that, he was an accountant with Kesselman & Kesselman, PwC’s Israeli affiliate. Lavi holds a BA in accounting and economics from Bar-Ilan University in Israel and an MBA from New York University. Location: London