by Russ Koesterich, CFA, JD, Portfolio Manager, BlackRock

In this article, Russ Koesterich discusses resiliency in the tech sector and why he believes adding further to core positions in the space is justified.

Key Takeaways

- While the tech sector experienced weakness in 1Q25 in anticipation of a global trade war, the recent rebound in the second quarter proves that there is value in the sector’s longer-term secular trends, namely AI, software, semiconductors and power generation.

- As the U.S. economy proves resilient and names within the sector continue to trade within a reasonable range from a valuation standpoint, Russ advocates adding to select names in the space during late summer’s historical period of seasonal weakness.

Tech and the broader growth style had a rough first quarter. The weakness did not last. Since early April investors have, once again, reverted to a tech bias. On a one and three-month basis, technology is the top performing sector. I believe growth, tech and AI-related themes can continue to lead in the back-half of 2025.

I would focus on three reasons why tech and related names can continue to outperform: a supportive macro backdrop, elevated but not unreasonable valuations and earnings momentum.

From a top-down perspective the early spring sell-off hurt crowded positions, momentum and any stock that carried excess risk, i.e. high beta. In contrast it rewarded less volatile, slow growth, stable companies that were perceived to be more resilient in the event of a trade war. As we have gained more clarity on tariffs, and more importantly, more confidence in the economy’s resilience, investors have rotated back into longer-term secular themes, notably artificial intelligence (AI), software, semiconductors and power generation.

My assumption is that the market, while still vulnerable to trade-related headline risks, will operate in a somewhat calmer atmosphere during the second half. Growth is likely to slow but the U.S. should avoid a recession. At the same time, price pressures associated with tariffs have proved modest and inflation has, thus far, been (mostly) contained. This should help keep long-term rates range-bound, as they have been for most of the year. An environment of positive but slow growth and stable rates should support growth over value, which, by contrast, has historically tended to perform best during periods when growth is accelerating.

From a valuation standpoint, while tech is not cheap, valuations are within range. According to data from Bloomberg, the tech heavy Nasdaq 100 is trading at 25x FY1 estimates and 22x FY2. Based on price-to-earnings ratios, the Russell 1000 growth index trades for approximately 1.8x the value index. Relative valuations are right around the five-year average and down from the post-pandemic peak of 2x.

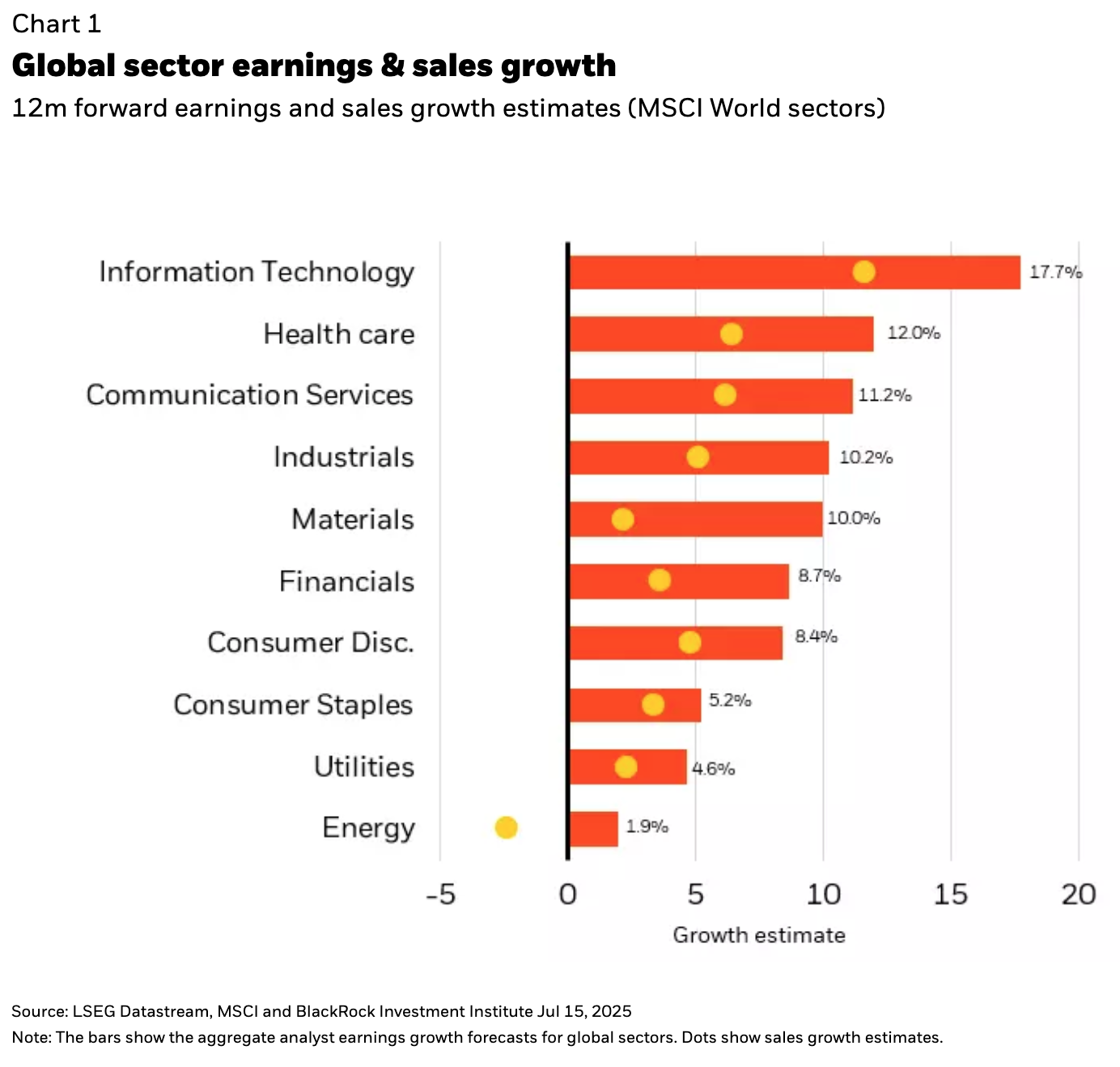

Elevated growth valuations are arguably justified based on profitability, margins and still stellar earning growth. We continue to live in a world in which mega-cap tech companies remain remarkably profitable, and despite large capital-spending plans, capable of driving strong earnings growth. On a global basis, the MSCI World tech sector is expected to lead the rest of the market in both earnings and sales growth (see Chart 1).

After a huge run, I doubt whether tech stocks are likely to move up in a straight line. Many of the top names are up 50% or more from the April lows. We are also entering a seasonally weaker period for stocks. That said, rather than trim excessively, I would use any late summer weakness to add to core positions in AI-related themes, software and communications. Looking out 6-12 months, I believe these names have the potential for further gains.

Copyright © BlackRock