by Vaibhav Tandon, Senior Economist, Northern Trust

The U.S. is watching Beijing’s growing maritime power.

An "end-to-end" approach in process management means handling a task or product from its initial planning stages to the finishing point or delivery, without relying on intermediaries for specific steps. No nation does this better than China.

China’s progress in establishing itself as the world’s factory is well understood. But as they developed their manufacturing prowess, China also worked its way up to become a world leader in getting all those products to customers around the world.

With more than 75% of global trade relying on the sea, building shipping networks has been central to China’s export-led growth strategy. Today, China stands as the dominant player in the global commercial maritime business, with world-leading positions in shipbuilding, port infrastructure, and sea logistics.

China is a global powerhouse in the shipping business.

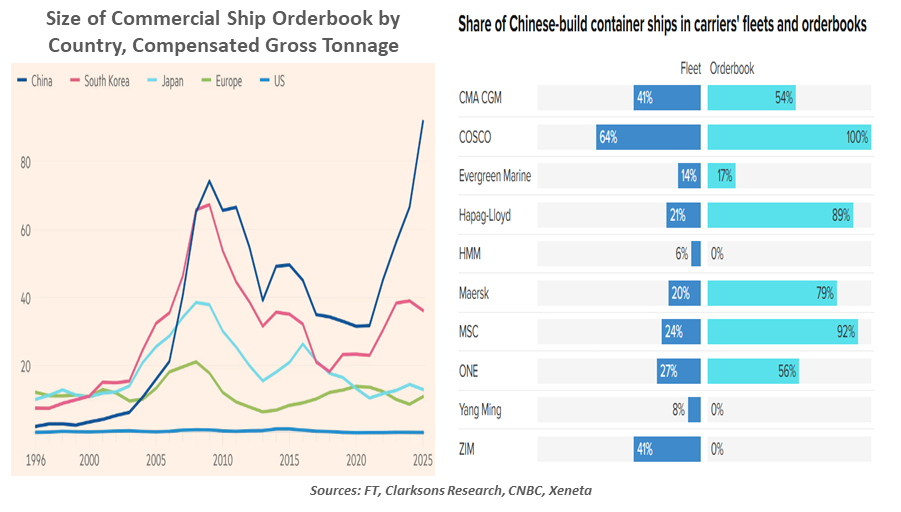

China’s capability in shipbuilding is unmatched. The country’s share of the commercial vessel market has grown from below 5% in the late 1990s to over 50% in 2023. By contrast, the U.S. shipbuilding industry has seen its rank drop from first to 19th place over the past five decades. Chinese shipyards are producing over 1,000 ocean-going vessels a year; the U.S. builds fewer than 10. South Korea and Japan, the next leading markets, are far behind China’s scale.

Once christened, those ships need to be filled. China also holds a near-monopoly in shipping container production, accounting for 95% of global output. China alone owns almost one-fifth of the global commercial ship fleet and almost three-quarters of the world’s shipbuilding orders. Over 20% of all U.S. trade imported into America last year arrived on Chinese-built vessels.

Like other industrial sectors, state backing has supported a rapid expansion of China’s shipbuilding capability. But it has also created excess capacity, stifling global prices and competition.

Beijing’s state-owned enterprises also have gained a considerable amount of influence in managing trade corridors across the globe. According to CFR Research, 129 ports outside of the mainland have Chinese investment. China owns a majority share in 17 projects. Over one-fourth of global container trade in 2023 passed through terminals where Chinese and Hong Kong–based companies held direct stakes.

The U.S. lags China in port control as well as shipping infrastructure capacity. The U.S. does not own or manage any commercial ports outside its borders. None of the world’s top ten shipping companies or seaport operators are from the United States. All of this highlights the potential leverage China holds over international maritime routes.

Beijing’s growing dominance, especially in port infrastructure, has prompted concerns among U.S. policymakers. The recent Panama Canal deal saw a Hong Kong-based company agree to sell shares of its facilities to a consortium led by a major American firm, underscoring the United States’ intent of pushing back on Beijing’s maritime power. The potential dual use of Chinese-owned ports for commercial and strategic purposes is one of the primary concerns in Washington.

The Office of the United States Trade Representative has proposed measures to reduce reliance on China’s maritime logistics and bring more ship manufacturing back to the U.S. These include imposing port service fees on vessels that are owned or operated by China-linked entities, and new requirements for the percentage of American goods to be transported on U.S.-flagged vessels to reach 15% over seven years.

As America seeks to reduce dependence on China’s commercial shipping industry, supply chains are at risk of getting caught deep into troubled waters. With Washington threatening a broadside against Beijing, the anchor is unlikely to drop anytime soon.

Copyright © Northern Trust