by Anwiti Bahuguna, Ph.D., Portfolio Manager, Northern Trust

We’re adjusting our stance in response to rising risk while maintaining a disciplined view on long-term strategy.

- What it is - We’ve made measured adjustments across select asset classes in light of recent market moves and evolving trade-related pressures.

- Why it matters - Shifts in policy and market behavior can introduce new risks—and now considerations—for positioning and portfolio balance.

- Where it's going - We’re positioning more cautiously, with an eye toward flexibility, as policy developments and macro signals continue to shape the investment landscape.

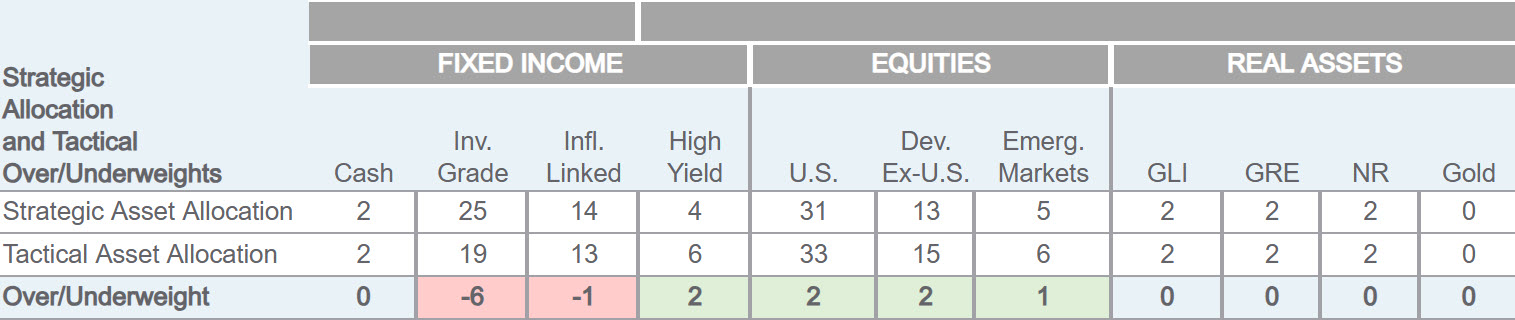

With U.S. tariff increases last week that exceeded expectations, our Tactical Asset Allocation Committee made several tactical allocation adjustments to our global policy model that guides portfolio allocation across Northern Trust.

We added 2% to developed ex-U.S. equities and 2% to cash, funded by a 1% reduction in each of U.S. equities, high yield bonds, global real estate and global listed infrastructure. This brings the tactical stance toward developed ex-U.S. equities to overweight, cash to equal-weight, real assets exposure to equal-weight, and slightly reduces the overweight to both U.S. equities and high yield (see table below).

Since February 19, the S&P 500 Index has corrected nearly 20%, with the speed of the market sell-off accelerating since “Liberation Day” on April 2. We do not want to overly de-risk after the correction. Sharp rallies are likely and markets remain highly susceptible to still-fluid policy announcements. We are working back toward neutral relative to strategic weights in what remains a highly uncertain environment.

GLOBAL POLICY MODEL

GLI = Global Listed Infrastructure; GRE = Global Real Estate; NR = Natural Resources

A Bigger Macro Shock to the U.S. Than Elsewhere

Absent a significant pivot in trade policy, we expect U.S. growth to meaningfully slow and inflation to move higher this year. This raises the likelihood of more forceful central bank easing, with the timing dependent on the speed at which growth slows. For the U.S., we view tariffs as a supply-side shock that reduces output while raising prices. The inflationary impulse will likely constrain the ability of the Federal Reserve to respond to the growth shock. If there is an economic downturn that occurs sooner and in a non-linear fashion, such that growth risks outweigh longer-term inflation concerns, we would expect earlier and more forceful Fed policy easing.

The disinflationary nature of the tariffs in non-U.S. regions positions other central banks and fiscal policymakers to better respond to the growth shock. In addition, European exports to the U.S. are around 2% of gross domestic product, while exports from Japan are about 4%. This suggests a notable growth shock, but one that should be manageable relative to the U.S.

Better Opportunities Outside the U.S.

Significant and broad-based tariffs that exceeded market expectations have led to a swift and negative reaction that has left the U.S. equity market almost 20% below recent highs. In recent days, cyclical-oriented sectors have underperformed defensives to a similar magnitude as during the Great Financial Crisis in 2008.

While we have downgraded our macro outlook for the U.S. vis-à-vis other regions, we do not want to significantly reduce U.S. equity exposure after these moves. Instead, we prefer to slightly reduce exposure, while also reducing U.S. exposure through a lower overweight to high yield. High yield would likely underperform in a U.S. recession, and it has held up very well year-to-date versus the drawdown in U.S. small cap stocks. Real assets have also performed well through the recent U.S. equity market correction. We sought to lock in outperformance from asset classes that have held up relatively well in order to fund increases in cash (building dry powder for opportunities) and developed ex-U.S. equities, given a better relative macro outlook and following a meaningful decline in equity markets.

Base Case Expectations

Supply Restraint (55% probability): Supply-side shocks from higher tariffs in addition to broader policy uncertainty weigh on consumer and corporate activity while halting the disinflationary process until a recession takes shape.

Central Bank Easing: Within our Supply Restraint scenario, the global growth shock leads to continued central bank rate cuts. The timing will depend on the speed of the growth slowdown, and could be more complicated for the Fed given a higher inflationary impulse from tariffs relative to non-U.S. regions.

Risk Case Scenarios

Soft Landing (35% probability): Global growth slows but remains positive via two potential paths: 1) tariff policy eases; 2) the U.S. economy is more resilient than expected and avoids a major deterioration in the consumer backdrop.

Reflation (10% probability): Policies of the U.S. administration have a net stimulative effect, leading to above-trend growth, persistent inflation and a pause in the Fed rate-cutting cycle.

Probabilities are based on views of Tactical Asset Allocation Committee members.

*****

Anwiti Bahuguna, Ph.D., Portfolio Manager

Anwiti Bahuguna, Ph.D., is chief investment officer of global asset allocation for Northern Trust Asset Management. She is responsible for managing investment performance, process and philosophy for multi-asset strategies globally. Anwiti leads NTAM’s strategic asset allocation, tactical asset allocation and capital market assumptions, and oversees the portfolio construction group and multi-manager business.

Copyright © Northern Trust