by Jared Franz, Richmond Wolf, Chitrang Purani, Capital Group

One month into President Trump’s second term, investors are spinning from one news cycle to the next. From higher tariffs to massive cost cutting and other sweeping initiatives, Trump’s policy goals come with significant investment implications.

Centre stage are executive orders that will impact companies in a broad range of industries, from aerospace and defence to industrials and banking. Waiting in the wings are year-end expirations of major provisions of the Tax Cuts and Jobs Act and expanded funding under the U.S. Affordable Care Act.

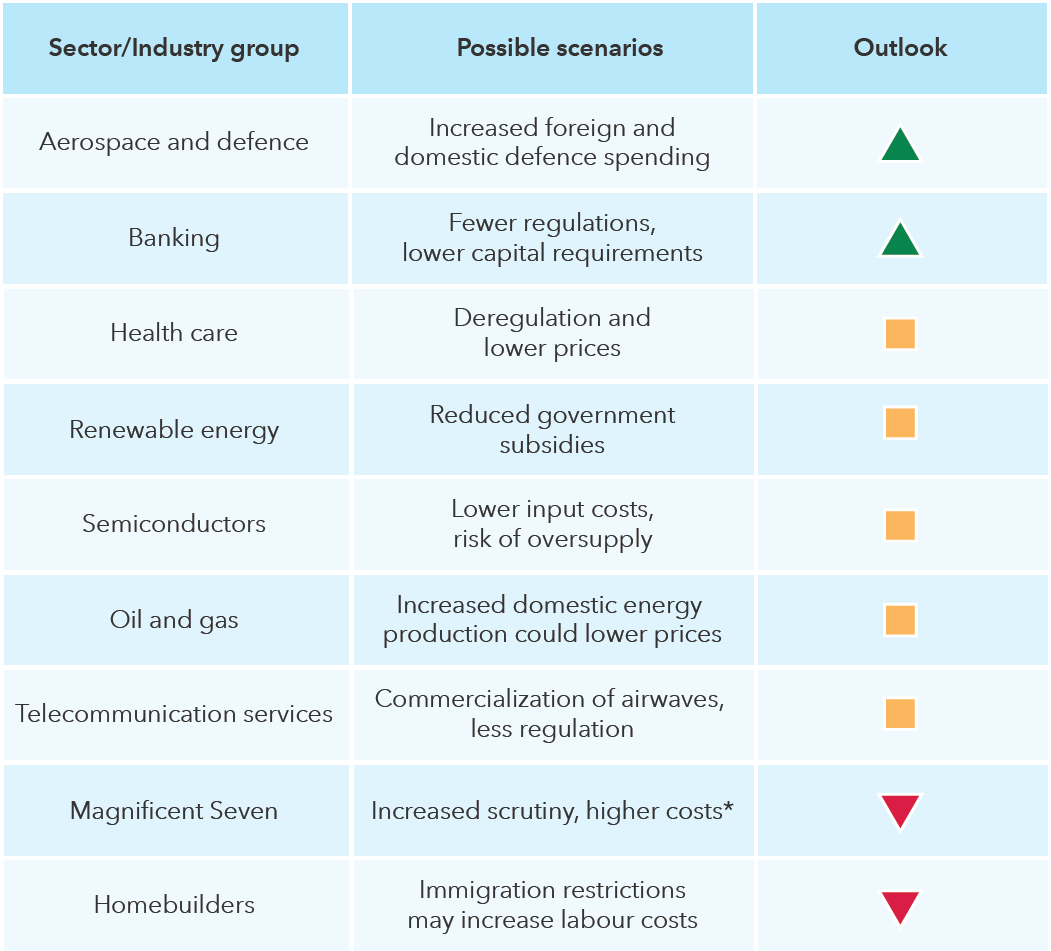

Which sectors could rise or fall under Trump 2.0?

Source: Capital Group. As of November 8, 2024. *Higher costs may occur if certain companies are required to pay into the U.S. Federal Communications Commission’s Universal Service Fund. For illustrative purposes only. Outlooks of individual investment analysts and portfolio managers may differ.

The ultimate winners of Trump 2.0 are likely companies that can successfully navigate policy and technology shifts, and a bottoms-up analysis can help separate the long-term winners. Three Capital Group investment professionals offer their take on opportunities and vulnerabilities as the Trump administration seeks to drastically reshape foreign and domestic policy.

1. America first approach brings manufacturing to the fore

President Trump's term may signal a philosophical pivot from free trade to protectionism. That means tariffs and other trade barriers are likely here to stay.

An “America first” policy aims to increase manufacturing jobs. “There’s an urge to regrow the manufacturing base the United States established in the 1950s and 1960s,” says economist Jared Franz. Beneficiaries may include construction and industrial companies tied to the build-out of data centres, autos and pharmaceuticals. For example, Caterpillar could see an increase in demand for its construction equipment, and Carrier Global’s heating and cooling systems, could also benefit.

It’s not just companies based in the U.S. that are taking part in this industrial renaissance. Looking forward, more companies may emulate Taiwan Semiconductor Manufacturing Company and Siemens by establishing operations in the United States to access the U.S. market.

Manufacturing could get a boost under an “America first” agenda

Sources: Capital Group, Bureau of Labor Statistics, U.S. Department of Labor. Figures are based on non-farm payrolls and are seasonally adjusted. As of December 31, 2024.

Franz notes that the United States’s enviable economy could likely withstand some bumps in the road related to tariffs and immigration as many of the impacts are targeted and hyper-local to a region or industry. For example, certain industries that rely heavily on immigration, such as homebuilders, could face labour shortages, which would lead to higher costs.

2. Deregulation could accelerate innovation

A new era of deregulation is expected to have sweeping impacts on the economy. Valuations are likely to rise and fall as investors digest the sometimes contradictory signals of tariffs and a looser regulatory environment.

Trump policies could accelerate innovation across artificial intelligence and possibly even pockets of health care, such as stem cell research which is of interest to the new Secretary of Health and Human Services, says portfolio manager Rich Wolf. Within AI, society could soon see a significant increase in robotics across commercial, residential and consumer sectors. Boston Dynamics, for example, creates robots for military, commercial and research applications.

Investors tend to underestimate the long-term impact of new technology

Sources: Morgan Stanley AI Guidebook: Fourth Edition, January 23, 2024; Next Move Strategy Consulting, Statista. Initial forecast dates were February 1996 for PC and internet users; January 2010 for smartphone shipments; March 2017 for cloud revenue; and January 2023 for AI market size.

Once a novelty, Waymo’s autonomous vehicles are now widespread throughout San Francisco and Los Angeles. The company is owned by Alphabet. Going forward, the key for the industry will be to scale profitability while maintaining the safety focus that builds trust with the public.

Many health care stocks remain under pressure as subsidies tied to the U.S. Affordable Care Act come under scrutiny. “Health care is a big lightning rod, but valuations are attractive for some companies within the sector,” Wolf says. For example, cell therapy companies and medical technology companies have largely sidestepped regulatory concerns. Medical technology companies developing products for robotic surgery include Intuitive Surgical and Stryker.

Trump has also pushed for a broad increase in defence spending among NATO members, which could benefit European-exposed aerospace and defence companies. Overall defence spending in the U.S. is unlikely to change, though budgets may move to newer technology like cyber, space and robotics.

3. Look to high-grade bonds for stable income opportunities

Inflation and an evolving mix of tariff and immigration policies have created market uncertainty. Given the strength of the U.S. economy, confidence that the Federal Reserve will lower interest rates this year has declined.

Absent a growth or inflation shock, interest rates are likely to remain near current levels, says fixed income portfolio manager Chitrang Purani.

The U.S. Consumer Price Index (CPI) hit 3% in January, up from its recent trough of 2.4% in September. Core CPI, which strips out food and energy, was 3.3%. Purani thinks inflation will gradually decline close to the Fed’s 2% target, but it may take longer than expected — especially if Trump’s more aggressive trade policies are implemented.

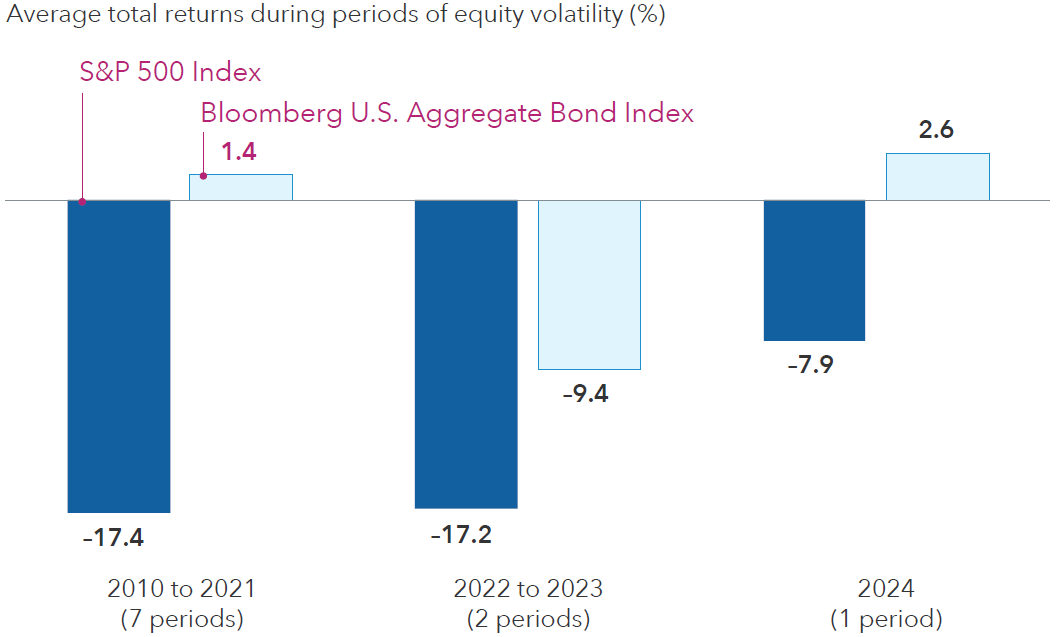

Diversification from equities appears to have returned for quality bonds

Sources: Capital Group, Morningstar. Periods of equity volatility from 2010 to 2023 are based on price declines of 10% or more (without dividends reinvested) in the S&P 500 with at least 75% recovery. The period of volatility during 2024 refers to July 15, 2024, through August 4, 2024. Returns are in USD.

“Identifying the winners and losers across sectors and issuers is more important than ever in this environment,” says Purani, who favours high-quality bonds over riskier, lower rated peers when constructing a core bond portfolio. That’s largely because credit valuations are tight across markets as investors have mostly priced in an optimistic growth scenario. Higher U.S. Treasury yields also translate to solid income potential, so investors don’t have to sacrifice quality. “Fortify your portfolios by improving quality in case we don’t get the growth outcome we expect — because it doesn’t cost a lot in terms of yields to do so.”

Bonds are also a compelling diversifier relative to cash and equities, Purani says. “Short and intermediate maturity Treasuries currently have attractive yields that largely price in the potential for stickier inflation and higher federal fund rates for longer. They also offer upside potential if we enter an environment where growth disappoints” In that scenario, Treasury yields may begin to fall, which would boost bond prices.

What’s next for investors

President Trump has implemented several policy changes that are likely to have lasting and complicated impacts on society and businesses. There is a risk these policies could have unintended consequences, and investors should be mindful of valuations amid the potential for heightened volatility.

Given high valuations and big gains in stocks over the past two years, it’s worth checking your risk tolerance against your portfolio holdings. “The investing world of the last few decades is fundamentally changing, but that doesn’t make things better or worse, it just raises uncertainty. If there’s one thing I’m reminded of though, it’s that markets and economies have shown resilience and continue to evolve and adapt,” Franz says.

Jared Franz is an economist with 19 years of investment industry experience (as of 12/31/2024). He holds a PhD in economics from the University of Illinois at Chicago and a bachelor’s degree in mathematics from Northwestern University.

Richmond Wolf is an equity portfolio manager with 19 years of investment experience (as of 12/31/2024). He also covers U.S. medical technology companies and REITs as an equity investment analyst. He holds a PhD from the California Institute of Technology and a bachelor's from Princeton.

Chitrang Purani is a fixed income portfolio manager with 21 years of investment industry experience (as of 12/31/2024). He holds an MBA from the University of Chicago and a bachelor's in finance from Northern Illinois University. He also holds the Chartered Financial Analyst® designation