Sticky underlying price pressures could prevent a faster return to neutral monetary policy.

by Carl R. Tannenbaum, Chief Economist, Vaibhav Tandon, & Ryan Boyle, Northern Trust

A once-mythical soft landing is at hand for the world’s major economies. The global expansion has remained resilient, withstanding restrictive monetary policy along with a host of geopolitical frictions. Inflation has been retreating, and employment levels remain very high. Equity markets have been especially strong.

That said, the mythology surrounding the incoming American government is an important factor in the outlook. The unstable nature of ongoing regional conflicts and the uncertain future of international commerce under the Trump administration could threaten performance in major world economies. Inflationary policy changes could add to sticky underlying price pressures and prevent a faster return to neutral monetary policy.

Following are our thoughts on how top areas are faring.

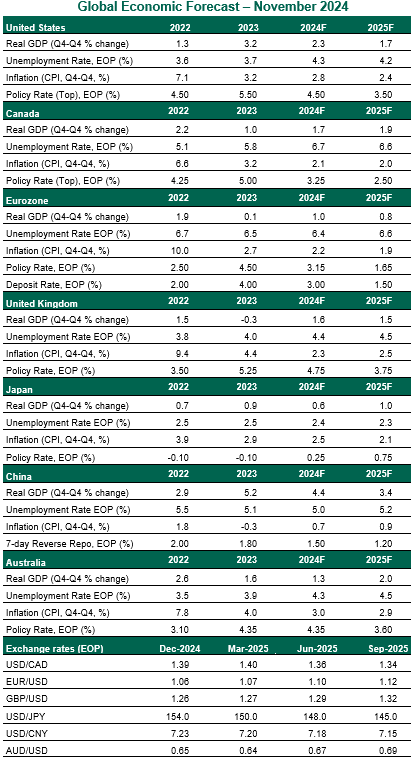

United States

- The U.S. economy performed well in the third quarter, with real gross domestic product (GDP) growing at 2.8% annualized pace. Consumers remain the main engine of growth. While much attention is focused on the economic consequences of the U.S. election, significantly altering our forecast at this time would be speculative. Inauguration is two months away; policies will take time to craft and enact; it may be a while before new measures become evident in the data. We believe the prospects for the soft landing are still favorable.

- The Fed’s policy rate remains sufficiently restrictive to justify continued interest rate cuts. But given the risks arising from tighter immigration policy, higher tariffs and the outlook for a prolonged fiscal imbalance, we now see the Fed taking a less urgent course of easing. The high level of interest rates may invite comment from the incoming administration, as it did prior to the pandemic.

Canada

- Though activity expanded at a moderate pace in the first half of the year, the Canadian economy is buckling under the weight of high interest rates. Consumer spending has been slowing amid higher-rate mortgage renewals and soft hiring. GDP growth will likely improve gradually in the coming quarters as policy becomes less restrictive. Next year’s elections, uncertainty around immigration policy and an evolving trade relationship with the U.S. are risks to the outlook.

- With economic slack increasing and inflation reaching 2%, the Bank of Canada (BoC) has pivoted towards more aggressive loosening of monetary policy. We expect the BoC to maintain the accelerated pace of easing in December and revert to 25 basis points cuts at every meeting thereafter, until reaching a neutral of 2.5%.

Eurozone

- The soft and hard economic data remain gloomy. Sentiment worsened in November, reflecting policy uncertainty under the incoming U.S. president. Industrial activity remains in the doldrums, with Purchasing Managers’ Indices still in contractionary territory.

The coming months will bring a number of political and fiscal headwinds. Germany will head to the polls early next year, with a changing of the guard likely. Several countries are under fiscal restrictions that will limit government spending. Wary of uncertainty, consumers have cut back on spending and increased savings. While growth will remain positive, the eurozone economy will continue to underperform its peers.

- Weak activity and continued disinflation imply more pressure on the European Central Bank to lower rates. We expect a sequence of 25 basis point reductions to a neutral deposit rate of 1.5% in late 2025. However, a growth disappointment could compel a more aggressive pace of easing early next year.

United Kingdom

- The U.K. economy slowed over the summer as real GDP growth moderated to 0.1% in the third quarter. We don’t see the softer headline GDP reading as a cause of concern: momentum remains intact with household consumption, government spending, and gross fixed capital formation all growing at a solid pace. Labor market conditions are also favorable. Private sector pay growth remained steady at a pace of 4.8% in September. The unemployment rate rose three-tenths to 4.3%, but we take the reading with a grain of salt due to methodological issues with the Labor Force Survey data.

- The Bank of England (BoE) cut rates by 25 basis points at this month’s meeting, while keeping forward guidance unchanged. Most Monetary Policy Committee members are of the view that the announcements from the Autumn budget will add to growth and inflation, reflected in upward revisions to BoE projections. This implies that the central bank will proceed with a gradual, quarterly pace of loosening.

Japan

- Japan's real GDP expanded 0.2% in the third quarter, down from a 0.5% increase in the second quarter. Consumption grew robustly, offsetting drags from business investment and net trade. A virtuous cycle between wages and prices is being formed. Stronger real wage growth and fiscal expansion will drive a private consumption recovery. But given the high reliance on trade, any tariffs on Japanese exports or a rise in protectionism will translate to a drag on growth.

- The Bank of Japan (BoJ) decided to keep the policy rate unchanged at 0.25% at its October meeting. Governor Ueda re-emphasized the central bank’s data-dependent approach, but signaled that rates may move higher in the coming months. While expectations of a hike at the December meeting have risen lately, the Governor’s speech this week offered no clear hint of further normalization. We retain our BoJ call of a rate hike to 0.50% early next year, but the impact of the weaker yen on prices could force the central bank to act sooner.

China

- It has been a rough year for China, with activity disappointing in almost all areas of the economy. Weak momentum pushed policymakers towards more forceful policy loosening in late September. Early signs of improvement are evident in the data, following a flurry of easing. In our view, the measures announced thus far are not enough to revive the ailing economy. With private demand weak and tariff risks looming, the Chinese economy could be in for a more stressful year.

- Policymakers will likely continue to use fiscal measures, complemented by monetary easing, to underpin growth. The Chinese economy needs more substantial demand-side policy support to counter the real estate downturn and fend off deflationary forces.

Australia

- Australian economic momentum was soft in the first half of the year, but green shoots are starting to appear. Households are becoming less frugal, as reflected in the improvement in retail sales. Tax cuts coupled with steady wage gains are boosting consumers’ purchasing power, giving households confidence even as monetary conditions remain tight.

Overall, growth will remain below trend, as restrictive monetary policy continues to exert pressure on household balance sheets. A key risk for Australia is getting caught in the crossfire of the U.S.-China trade war, as both nations are among its top three trading partners. Weaker demand for Chinese goods will have a spillover impact on demand for Australian commodities.

- While economic conditions in Australia may not differ that much from its advanced economy peers, the Reserve Bank of Australia (RBA) continues to be an outlier. The central bank held the policy rate steady at its November meeting, as underlying inflation is too high for the central bank to pivot. A short and shallow easing cycle is expected to commence in early 2025.

Copyright © Northern Trust