by Vaibhav Tandon, Senior Economist, Northern Trust

Slower spending is a part of the return to normal economic conditions.

When my wife gets anxious about the cost of going out for an elaborate dinner, I remind her of what American political satirist P. J. O'Rourke wrote: “Better to spend money like there’s no tomorrow than to spend tonight like there’s no money.”

Deep down, I know that’s not sustainable advice. And more American consumers are waking up to that reality. Tomorrow has arrived, and some reckoning is in order. But reckoning is not retreat.

Flush with cash generated by pandemic-era support programs, American consumers splurged on goods during the lockdown and on services during the reopening phase. Resilient household spending has been one of the main reasons the U.S. economy has avoided a recession and outperformed its peers.

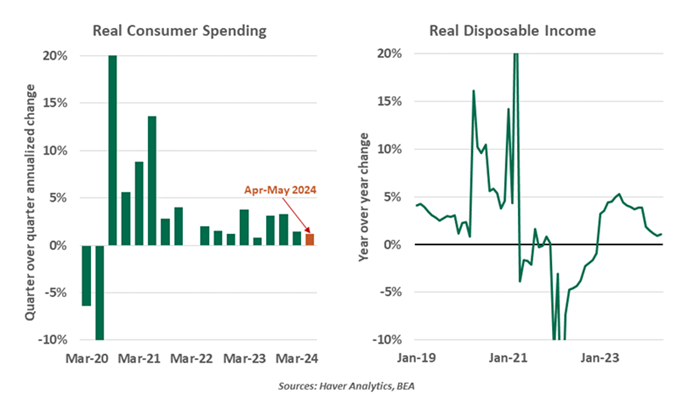

But the days of splurging have come to an end. Real consumption growth has slowed to an annualized rate of 1.4% in the first half of 2024, down from a pace of over 3% in the last two quarters of 2023. The overall path for goods spending this year has been weak; a slowdown in auto sales suggests some hesitation to make major purchases. According to research firm NielsenIQ, customers are still visiting stores regularly, but are buying fewer items at each trip..

Expenditures on services have also been relatively soft this year. Spending at restaurants fell to its lowest level in seven months in May, according to the National Restaurant Association.

Forward-looking indicators are pointing towards further softening in demand. The University of Michigan Consumer Sentiment Index dropped to an eight-month low in July, remaining far below its pre-pandemic levels. Consumers in the bottom third of the income distribution are more downbeat than the rest, but higher earners are also growing cautious. More and more companies have been calling out spending weakness. Consumers are making “tough choices with their budgets,” said the chief executive officer of a major U.S. retailer on a first-quarter earnings call. With shoppers becoming more price sensitive and sales declining, retailers are returning to offering discounts.

One root cause can be found in the data on earnings. Real disposable income growth has averaged just 1.3% year over year in the first five months of 2024, compared to an average annual increase of 4.1% in 2023 and 3.3% in the year before COVID. Those earning less than $45,000 a year have witnessed a notable deterioration in their finances, which contrasts with resilience among affluent consumers.

An increasing number of Americans have seen their savings dwindle as elevated inflation and interest rates continue to squeeze household finances. Excess savings, which ballooned to $2.1 trillion in August 2021, have been fully exhausted, according to San Francisco Fed estimates. Since early 2022, American households are saving less than 5% of disposable income.

Consumers are pulling back, but not collapsing.

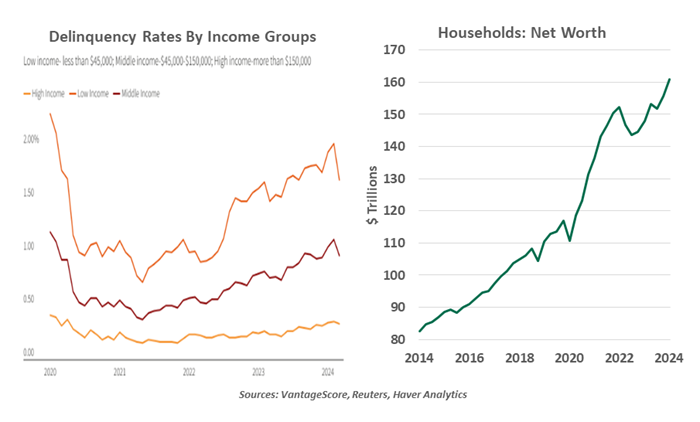

As incomes decline and savings are exhausted, an increasing number of households have turned to debt to support outlays. Outstanding credit-card balances have risen to $1.33 trillion, up from a pandemic-era low of $970 billion in April 2021.

Younger and lower-income borrowers are falling behind on payments. Data from the New York Federal Reserve shows that about 9% of credit card balances transitioned into delinquency in the first quarter of 2024, the highest rate in a decade. Auto loans, the second-largest debt category behind mortgages, are experiencing their highest delinquency levels since 2010.

While there are pockets of concern, the perception that consumers are exhausted is not accurate. Overall, household balance sheets remain healthy: though excess savings have been depleted, households have more financial resources to draw on during a rainy day. Household net worth has surged by a whopping $44 trillion in the last five years, boosted by rising home values and strong stock market returns.

Interest costs associated with consumer debt have increased, but households are still spending about the same percentage of their incomes to service debt as they did before the pandemic.

The labor market is loosening, but businesses are still hiring and incomes still growing. Jobless claims have not risen much, and layoffs remain low. No longer overheated, this is a labor market that is starting to resemble conditions before the pandemic.

That said, lower-income households are not enjoying wealth effects from high house prices and the equity rally, with fewer resources to contend with a higher cost of living. Combined with rising consumer credit delinquency, signs of a K-shaped recovery are accumulating: the divergence between households prospering and struggling is increasing.

In our view, broad trends are signaling a return to a normal pace of consumption, as opposed to foreshadowing recession. Nonetheless, Americans are spending less enthusiastically. Showing some discipline tonight will help households to be in better financial shape tomorrow.

U.S. consumers are sound overall, but there is some divergence of fortune.

Copyright © Northern Trust