by John H. Fogarty, CFA, Co-Chief Investment Officer—US Growth Equities, Vincent Dupont, CFA| Director of Research—US Growth Equities, AllianceBernstein

What should equity investors look for to find companies with strong economic profits, backed by clear business advantages?

Equity investors typically seek companies with strong earnings growth. But not all earnings are created equal. Distinguishing between different types of profits can help investors avoid hot stocks of companies with unsustainable earnings—and focus on those more likely to deliver persistent growth over time.

Today’s market conditions highlight a timeless challenge for equity investors. Artificial intelligence (AI) may unlock productivity and profit gains, but not universally. And even clear AI winners might not succeed at delivering extremely high profitability for years to come. Long-term equity investing success always requires a clear view of business fundamentals, even when big themes are captivating the market.

Earnings Are Often Misunderstood

In complex market conditions, it’s helpful to revisit enduring investing principles. Most investors intuitively know that stock prices are determined by the profits (or earnings) that a firm is expected to make.

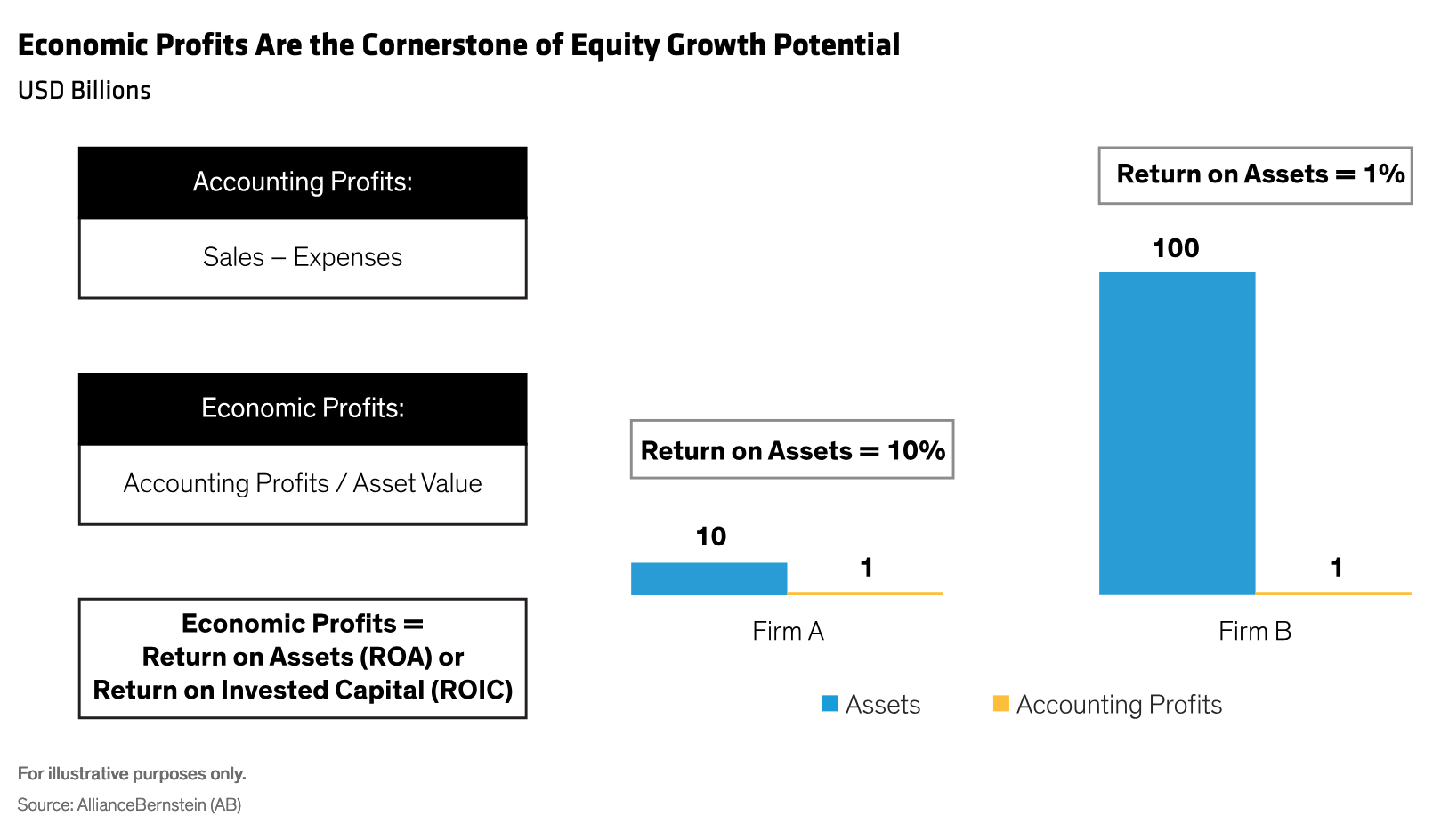

But what exactly is meant by “profits”? There are many measures, but two basic definitions: the accounting definition and the economic definition. Accounting profits are a company’s sales minus expenses such as raw material and labor. Economic profits are accounting profits after considering the assets required to generate those profits—the effective use of those assets is of key importance for equity investors, in our view. Economic profits are best illustrated by return on assets (ROA) or return on invested capital (ROIC).

Here’s why it matters. Consider two companies that each have accounting profits of $1 billion (Display). Firm A generates those profits from $10 billion in assets, while firm B makes the same profits from $100 billion in assets. Firm A is much more profitable and efficient in its use of assets, as illustrated by its ROA of 10% versus 1% for firm B.

Economic Profits Are the Cornerstone of Equity Growth PotentialUSD Billions

Economic profits are the most important guide for equity investors, in our view. That’s because assets are provided by investors, so the ROA—or the profits on these assets—represents the rate of return for the money they invested.

Cost of Capital: The Invisible Hurdle to Tangible Returns

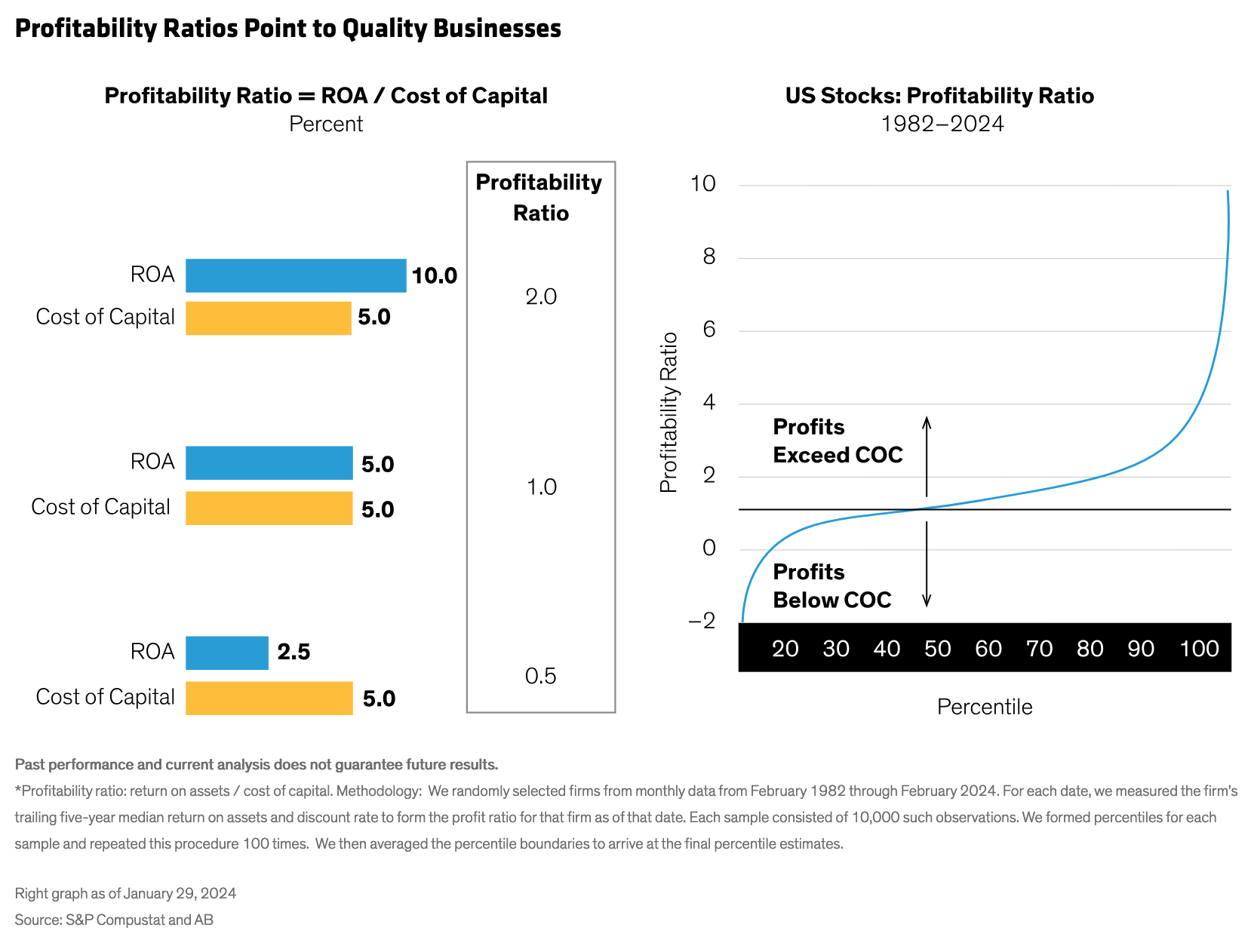

But how can we know whether a company’s ROA is attractive? For that, we need to know the company’s cost of capital (COC). The COC is the rate of return, or a hurdle that the market sets uniquely for each company. It tells the firm, “Here is the ROA you need to make to justify retaining earnings; if you can’t hit that return just pay us a dividend.”

There’s one problem: the COC is not directly observable; it must be statistically inferred. However, once investors have an estimate, they can define the profitability ratio for each firm as the ROA over the COC. In other words, a company with an ROA of 10% and a COC of 5% has a profitability ratio of 2.0 (Display).

Profitability Ratio Points to Quality Businesses

While this calculation might seem technical, it’s actually a very important indicator of business quality. That’s because companies that are expected to consistently show a profitability ratio well above 1.0 are often running their businesses in a way that delivers sustainable profits on their assets.

Economic theory suggests that in perfectly competitive markets profitability ratios would get reduced to 1.0. In other words, increased competition would reduce a company’s competitive advantages, and subsequently, its returns. In fact, real-world data confirm this is true. Our research indicates that the median profitability ratio over a very large sample of US companies from 1982 to 2024 was approximately 1.0 (Display, above).

Fundamental Research Can Identify Persistent Growth

Some firms do much better than that. Higher sustainable profitability ratios typically increase the value of the business for shareholders. Of course, many factors can influence stock prices over the near to medium term, even if a company has an attractive profit ratio. Still, we believe equity markets are inherently forward-looking, and always judge firms’ long-term profitability ratios. So even if short-term volatility pushes a stock off course, we think the shares of companies with higher profitability ratios will ultimately overcome market shocks and deliver long-term stock price returns aligned with their high-quality profits.

Judging the sustainability of profitability ratios is not simply a mathematical exercise. Deep fundamental research, based on company and industry expertise, is the key to understanding whether a company’s business can support persistently high profitability. Competitive advantages, pricing power, innovation and management skill all play a role in determining the underlying resilience of a business.

Watch Out for Extremes and Mean Reversion

Even with a good grasp of profitability ratios, investors must avoid some common pitfalls. First, beware of mistaking a bad business for a good one. This may happen when investors chase hot trends without examining a company’s economic profitability.

Second, watch out for extremely high profitability ratios. Today, large-cap equity indices are highly concentrated in firms with exceptionally high profitability ratios—and not all will stand the test of time. Investors shouldn’t be seduced by suspiciously high profitability ratios; scrutinize the business fundamentals to evaluate whether this profitability is sustainable or at risk of mean reversion.

In hot and cold markets, we think active investors must search for profitable companies backed by quality businesses across sectors and industries. Staying focused on these attributes while being guided by economic profits and profitability ratios is a great recipe for capturing the equity return potential of companies with truly persistent growth power to weather dynamic market conditions.

About the Authors

John H. Fogarty is a Senior Vice President and Co-Chief Investment Officer for US Growth Equities. He rejoined the firm in 2006 as a fundamental research analyst covering consumer-discretionary stocks in the US, having previously spent nearly three years as a hedge fund manager at Dialectic Capital Management and Vardon Partners. Fogarty began his career at AB in 1988, performing quantitative research, and joined the US Large Cap Growth team as a generalist and quantitative analyst in 1995. He became a portfolio manager in 1997. Fogarty holds a BA in history from Columbia University and is a CFA charterholder. Location: New York

Vincent Dupont is a Senior Vice President and Director of Research for US Growth Equities. Before joining the US Growth team in 2009 as a portfolio manager, he spent 10 years as a fundamental research analyst covering semiconductors and semiconductor capital equipment. Prior to joining the firm in 1999, Dupont researched the Russian economy at the Council on Foreign Relations for a year and worked at the US State Department as an arms control official for six years. He holds a BA in political science from Northwestern University and a PhD in international affairs/Russian studies from Columbia University, and is a CFA charterholder. Location: New York