We review the key themes of the first half of a busy year.

by Carl Tannenbaum, Vaibhav Tandon, and Ryan Boyle, Northern Trust

Editor’s Note: We pause at halftime to recap the highlights of this important year.

Higher for Longer

In logistics, the “last mile problem” refers to the challenge of getting shipments to their ultimate destinations. After moving smoothly along highways, local impediments create resistance as the process nears its completion.

After moving smoothly downward during the latter half of last year, inflation has encountered resistance as it nears the desired destination. Localized impediments to progress will need to be cleared before interest rates return to more moderate levels.

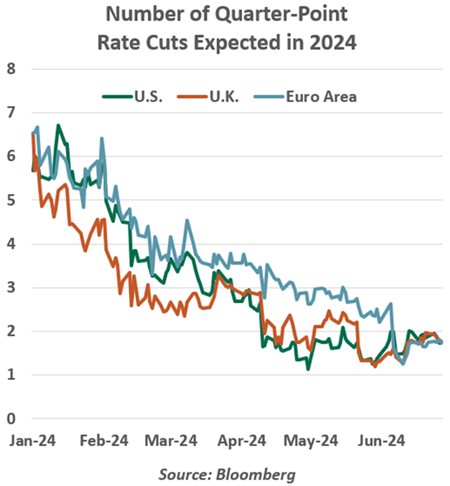

As we began the year, easier monetary policy seemed close at hand. Moderation during the second half of 2023 placed targeted inflation levels within sight. Markets implied 6 or 7 rate cuts this year from the Fed, the Bank of England and the European Central Bank (ECB).

But disinflation slowed, anchored by price developments for services and shelter. There remain important imbalances in corners of the labor market: the recovery of immigration to (and beyond) pre-pandemic levels should eventually help, but will take some time to gain traction.

Stalled progress on inflation led central banks back to a “higher for longer” strategy. The change of tack hindered growth in Europe more than in America; the prevalence of variable rate mortgages in Europe exposed households to the sting of higher interest rates.

With European economies struggling, the ECB reduced interest rates this month and many think that the Bank of England will follow before the summer is out. Both, however, have signaled lingering caution that will make easing a slow process.

The Fed will bring up the rear. Many forecasters (including ourselves) see a first move in September, but the inflation data will have to be exceptionally well-behaved between now and then. Some analysts see signs of weakening in the American economic data, but the risk of recession seems very low.

Runners often encounter a last mile problem. I certainly do, when I attempt to run…well, a mile. The last few steps always seem to be uphill, but it’s wonderful to ease off once the goal has been reached. Staying focused on the finish is critical.

Up, Up and Away

In the early months of the pandemic, public health policy advanced the goal of “bending the curve” of COVID infections. The process was slow, with disappointing surges along the way. But the curve did eventually flatten and decline.

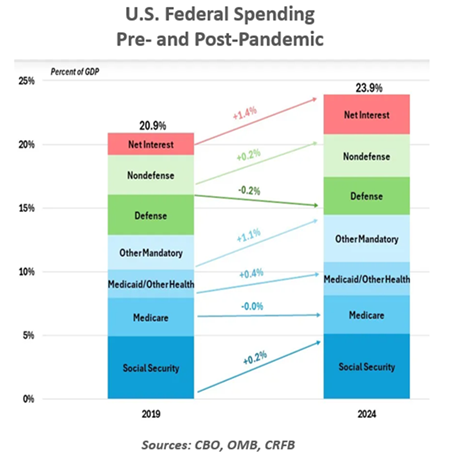

The next curve we hoped to see turn downward was the arc of sovereign debt. Pandemic stimulus was expensive, but it prevented a great deal of economic scarring. While government spending in many economies slowed thereafter, U.S. federal spending remained elevated. America’s debt and deficits are rising at a frightening pace.

A review of the budget offers many explanations and few remedies. The Baby Boom generation is entering retirement, raising obligations for Medicare and Social Security. Amid heightened geopolitical risk, cutting back on defense does not seem prudent.

The Congressional Budget Office now expects a deficit of $1.9 trillion (6.7% of gross domestic product) in the current fiscal year, growing to $2.9 trillion in ten years. Interest costs have more than doubled since 2020 and now total more than either defense or Medicare expenditures.

This kind of trajectory could evoke a market reaction, but Treasury yields have been well-behaved. Despite downgrades, the U.S. remains the world’s risk-free benchmark. Auctions of new debt have shown some initial signs of saturation, but demand for Treasuries remains solid. The U.S. dollar continues to show strength.

Markets may be sanguine because the U.S. fiscal imbalance is hardly a novel risk, but patience may be running out. The November election is likely to yield a divided legislature, with neither party advocating significant spending reductions. The debt ceiling suspension will end on January 2, 2025, taking force at the level reflecting all borrowing through 2024. Extraordinary measures to postpone a default could be underway as the next president takes the oath of office.

Unfortunately, there is no vaccine against fiscal recklessness. And so, the debt pandemic continues.

High and Dry

After an ascent spanning three decades, China is no longer the high flying economy it used to be.

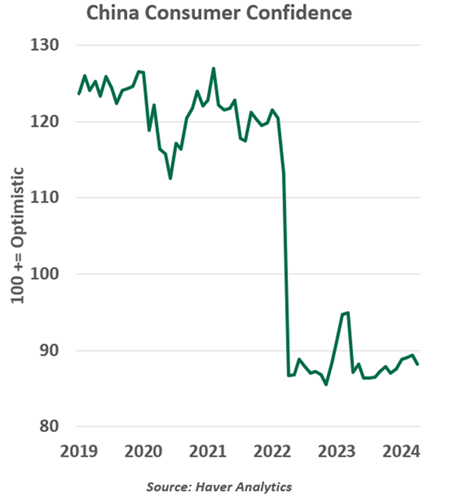

Optimism about the future of the Chinese economy collapsed during the pandemic and hasn’t returned. Growth has remained weak, with the old export and infrastructure investment-driven model crumbling. The boom in the real estate sector, which accounted for almost a quarter of China’s gross domestic product (GDP) in some years, came to a halt in 2020 as easy credit to developers was reined in.

China’s total debt exceeds 300% of its GDP. A sizeable chunk of that debt is held by the local governments, whose tax revenues have taken a hit from lower land sales. Relationships between local developers, local banks and local governments are dragging all three down.

With a large share of household wealth parked in the property market, the real estate downturn is weighing on confidence, forcing consumers to cut spending. A host of measures aimed at providing a floor to the property market haven’t yielded any positive results. Though consumption improved last year, the saving rate remains above its pre-pandemic levels, a sign of continued caution among households.

Slow activity raises the threat of deflation and the specter of “Japanification” for the Chinese economy. Faced with weak demand, industries are coping with an excess capacity problem, denting investment and hiring prospects.

China can no longer export its way out of trouble. Trade frictions with the West and increasing adoption of the China plus one business model will limit any gains in this area. Investors are taking flight, reflected in elevated capital outflows. Chinese equities have fallen out of favor in recent years. The Chinese yuan, an indicator of confidence in the economy, is under pressure.

Traditionally, China responded to economic setbacks by boosting government spending on infrastructure projects. But these opportunities have mostly played out. A shrinking population will further complicate the goal of sustaining economic growth.

With the challenges multiplying, policymakers are struggling to find the right options for stimulus to provide a lift-off to the economy. China looks set for much weaker growth in the years ahead.

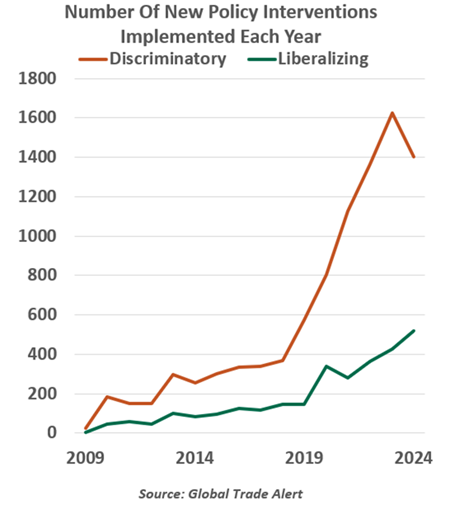

The New World Disorder

The geopolitical environment remains very challenging. Hot and cold wars, along with economic fragmentation, are the order of the day.

The realignment away from an efficiency-based model of cross-border commerce has accelerated in 2024. Trade and investment dynamics around the world are increasingly being pushed and pulled by geopolitical alliances, altering the business landscape. Public support for economic openness and free markets is in decline.

Buzz words like reshoring, nearshoring, friendshoring and deglobalization are increasingly mentioned on firms’ earnings’ calls. Tensions between the world’s largest economies are prompting new tariffs. Foreign investment flows are segmenting along geopolitical lines. The post-pandemic era has also been characterized by the broader application of industrial policy to achieve geopolitical objectives.

According to the International Monetary Fund, trade between blocs has slowed much more than trade between geopolitically aligned nations since the start of the Ukraine war. Owing to increased economic interdependence between economies since the Cold War days, the costs of fragmentation are going to be immense. According to the IMF, the decline of global commerce could create costs equal to a whopping 7% of global gross domestic product (GDP). Fragmentation also threatens the existence of the multilateral institutions, responsible for preserving the global order.

Weakened alliances will diminish the world’s economy and its ability to respond to a growing array of threats. Tail risks are rising, and will need to be monitored.

Heaven and Earth

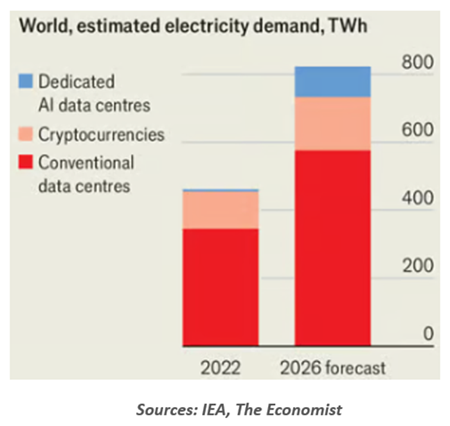

Artificial Intelligence (AI) has been a dominant theme during the first half of the year. The S&P 500 is up 15% this year; if you remove the “Magnificent 7” tech stocks, that return falls to 7%. Every week, it seems, AI conquers another significant challenge. The sky seems to be the limit.

But the natural world may ground these ethereal aspirations. As we detailed in our essay “Empowering AI,” the electricity needed to support artificial intelligence places it on a collision course with climate change. Data center construction is rising rapidly, and all of those servers will need to be powered and cooled.

The world has made some progress in promoting more environmentally-friendly fuels, but demand increases have deepened reliance on traditional sources. Bending the carbon curve remains an elusive goal.

Further, some of the infrastructure needed to support both AI and the green transition relies on basic minerals which are not easy to access. Mining, far from the world’s most glamorous industry, is critical to those on the cutting edge.

These impediments will need to be overcome. AI promises to increase productivity growth, which will be essential to offset less-favorable demographics. Productivity raises potential economic growth, which can make debt sustainable. We’ll need all the productivity we can get if we hope to deal with the mountains of debt currently borne by governments…and their citizens.

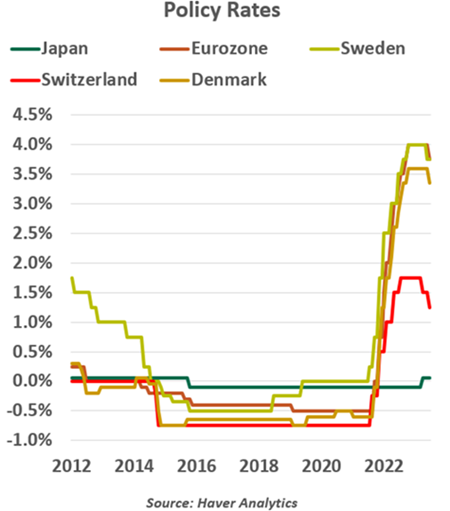

End Of An Era

Of the many measures large central banks undertook in the wake of the 2008 global financial crisis, negative interest rates were among the most controversial. The benefits of breaking the zero lower bound were unclear, but potential hazards were apparent.

The world’s 12-year experiment with negative interest rate policy (NIRP) came to end earlier this year when the last holdout, the Bank of Japan (BoJ), moved its policy rate back to zero. This provided an opportunity for reflection.

The first area of contemplation surrounded Japan itself. The country has struggled economically since 1990, at the hands of a property market crash and an aging demographic. Deflation set in and was difficult to unearth.

The BoJ was dogged in its determination to get the economy back on its feet. Apart from keeping overnight interest rates below zero, the Bank was one of the few that exercised “yield curve control,” targeting a range for longer term interest rates to keep them down. The BoJ also sustained the largest quantitative easing program in the world; according to Bloomberg, the Bank of Japan owns more than half of the stock of Japanese government bonds and about 7% of the Japanese equity market.

After a long period of frustration, price pressure produced by the pandemic finally broke the back of deflation. Rising costs led workers to demand higher wages; the government pressed for those wishes to be granted. Japan now has a welcome wage-price spiral that appears sustainable. Growth in Japan has improved, and its equity market set a new record high for the first time in 34 years.

While rates in Japan are now positive, the room for aggressive tightening is limited. Government finances are vulnerable to higher rates, as are around 70% of Japanese mortgages. Private sector firms are resilient thanks to large cash reserves, but much higher rates could generate stress.

The Bank of Japan will also be mindful of its past policy mistakes. Economists like Ben Bernanke had attributed Japan’s lost-decade malaise to “exceptionally poor monetary policymaking.” The BoJ declared victory over deflation prematurely on several occasions during the past two decades, only to see conditions deteriorate.

A retrospective on negative interest rates does not yield positive impressions. In theory, NIRP supports economic activity and inflation, but in practice, the policy failed to deliver results on either front. Negative rates may have also facilitated the buildup of debt and an exaggerated shift towards riskier assets. Seen as a signal of deflationary pressures, NIRP also faced criticism for undermining consumer and business confidence, making both more wary. Unconventional policy was no cure to lowflation, but some central banks still found it better than nothing.

It's nice to see Japan back on track. But it is unlikely that we will see negative interest rates come back anytime soon.

Copyright © Northern Trust