by Nelson Yu, Head, Equities, AllianceBernstein

Despite narrow market concentration, we see opportunities in high-quality stocks that haven’t yet been rewarded.

Global stocks posted healthy gains in the first half of 2024, although second-quarter performance moderated from the previous quarter’s breakneck pace. With inflation still sticky and equity returns concentrated, the time may be right for investors to broaden their horizons.

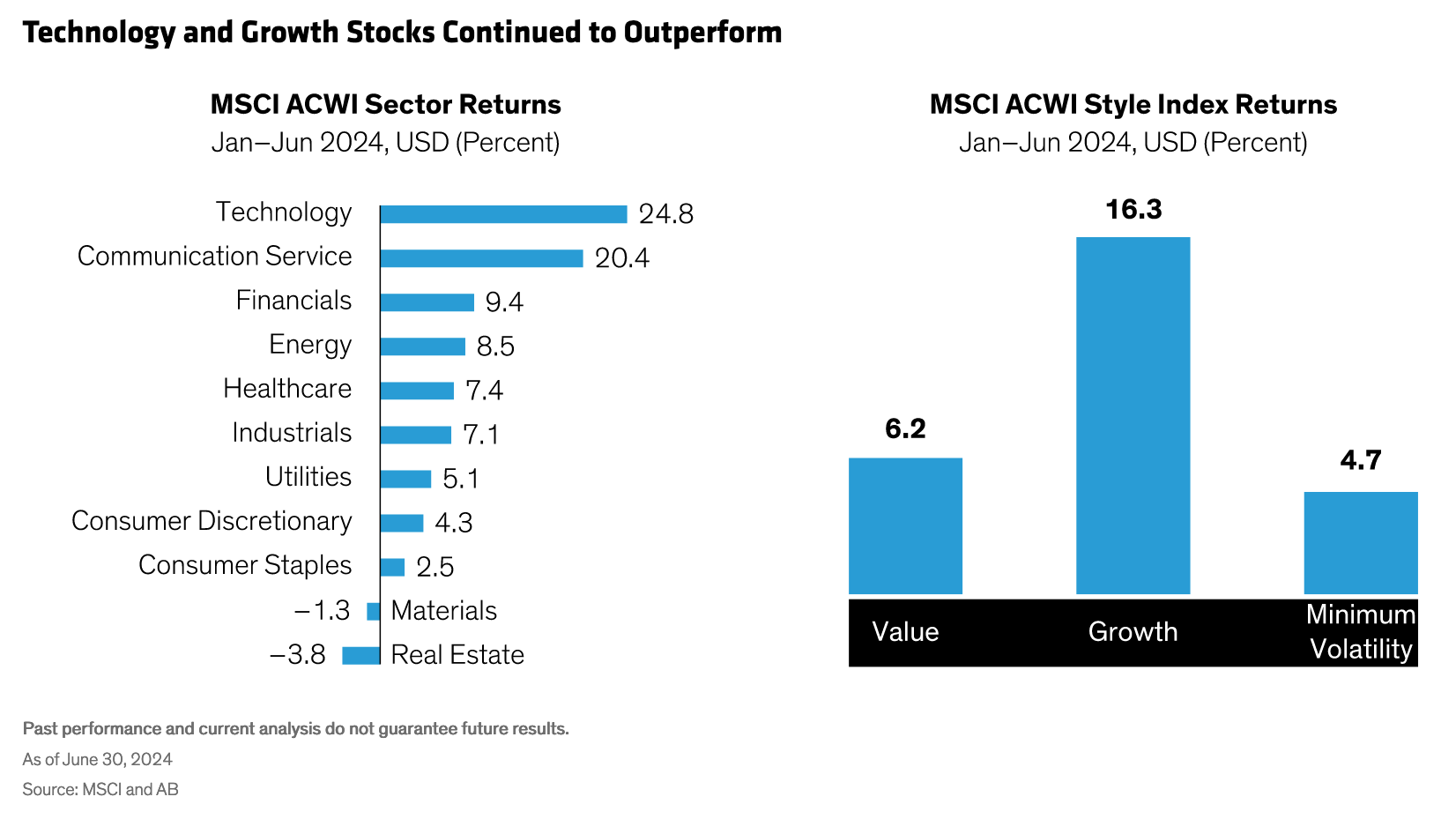

The MSCI ACWI advanced 11.3% during the half in US-dollar terms, with most of that coming in the first quarter (Display). Japanese equities—while continuing to perform strongly in local currency—came back to earth in the second quarter in US-dollar terms, as the yen continued to weaken. Emerging-market equities rose by 7.5% in the first half of the year but still lagged developed markets. US large-caps led global gains in the first half, even after losing momentum in the second quarter.

In a trend that has become familiar to equity investors, large-cap market breadth was again highly concentrated, with a good share of the S&P 500’s gains coming from a disproportionately small number of large technology companies. Technology and communication services set the pace, while healthcare stocks were aided by an uptake in GLP-1 drugs for weight loss. The real estate and materials sectors delivered the weakest performance (Display). Globally, growth stocks outpaced value stocks, which sputtered in the second quarter.

Inflation: Higher for Longer

As the third quarter begins, inflation remains top of mind for global investors. In Europe, price increases moderated enough for the European Central Bank (ECB) to cut its primary interest rate from 4% to 3.75% in early June, but inflation is still hovering above the ECB’s long-range goal of 2%. The ECB joined Canada and the Swiss National Bank in easing monetary policy. To be sure, there are still some notable outliers in the struggle against inflation, such as China, where policymakers are more focused on kick-starting the struggling economy.

In the US, the Federal Reserve has stayed on the sidelines, largely because inflation has periodically surprised to the upside. Most recently, the Consumer Price Index cooled to 0.16% in May on a month-over-month basis—largely the result of falling energy prices and declines in transportation services. But with inflation still running above the Fed’s target, investors have done an about-face on expectations for multiple rate cuts in 2024. AB’s economists anticipate a soft landing for the global economy this year, with the Fed likely to hold off on monetary easing until the fourth quarter, barring a meaningful deterioration in the labor market.

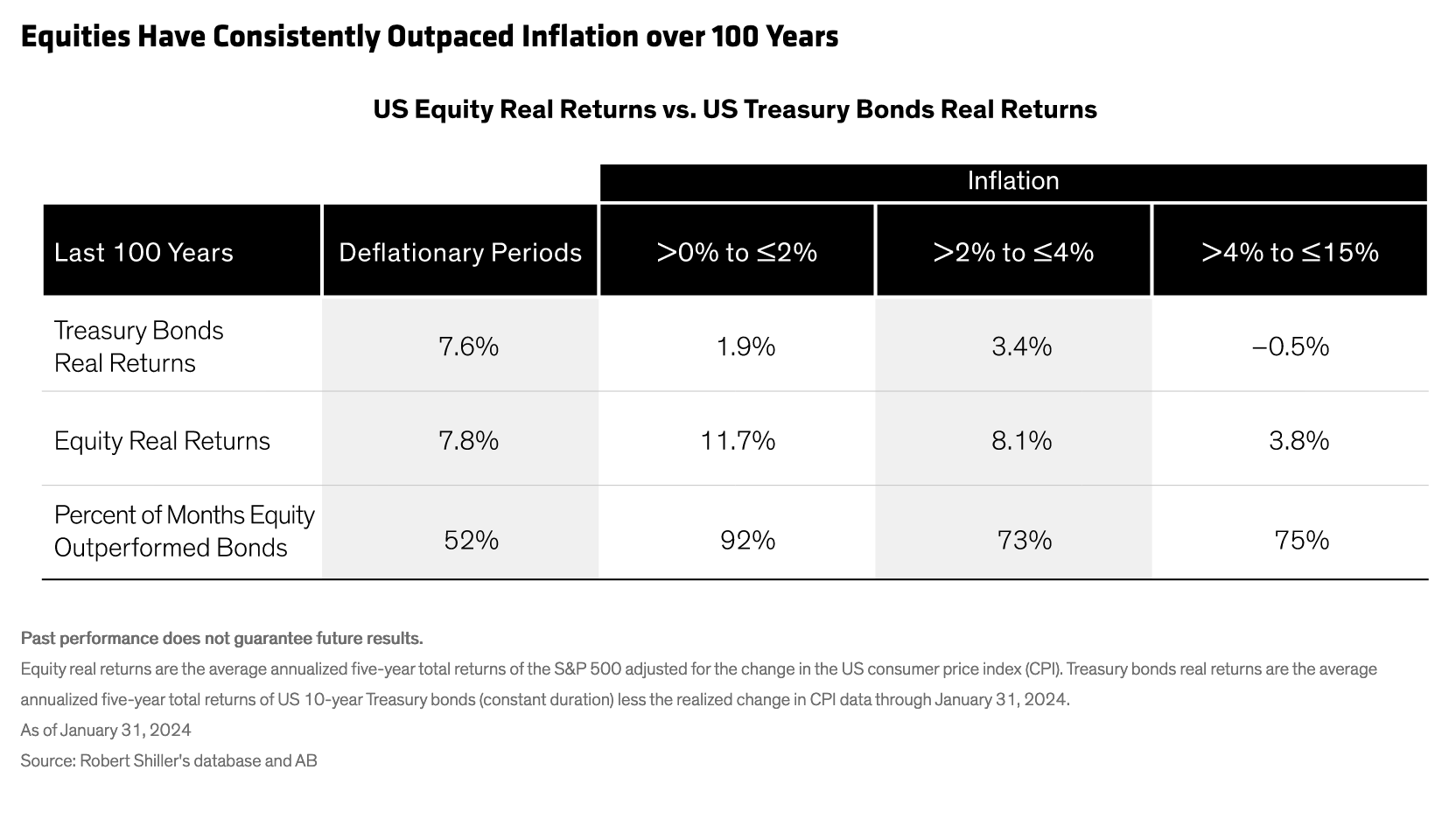

With inflation elevated in the US and Europe, we believe equities deserve a prominent place in investors’ portfolios—particularly since pre-pandemic inflation rates may be a thing of the past. Historically, stocks have been an effective hedge against price increases, and they’ve consistently outpaced inflation over the past 100 years. In fact, when inflation has run between 2% and 4%—the current scenario in much of the developed world—equities have averaged annualized real returns of more than 8% on a rolling five-year basis (Display).

Geopolitical tensions and supply shocks could muddy the inflationary outlook. Still, in a higher-for-longer environment that has the world’s central banks wary of easing monetary policy too quickly, we believe equities are an integral component of long-term investment allocations.

Signs of a Broadening Market?

While equities may be well-positioned, gains have so far been inequitable. Just how concentrated has the market been? The top 10 stocks in the S&P 500 now comprise more than 35% of the index by market capitalization. That means that just 2% of companies in the S&P 500 are driving broader market performance.

Some of the world’s largest technology firms have been the primary beneficiaries of ballooning market capitalizations. Colloquially known as the Magnificent Seven—Alphabet (Google), Amazon.com, Apple, Meta Platforms, Microsoft, NVIDIA and Tesla—most of these companies have been riding the wave of a generative artificial intelligence (AI) revolution.

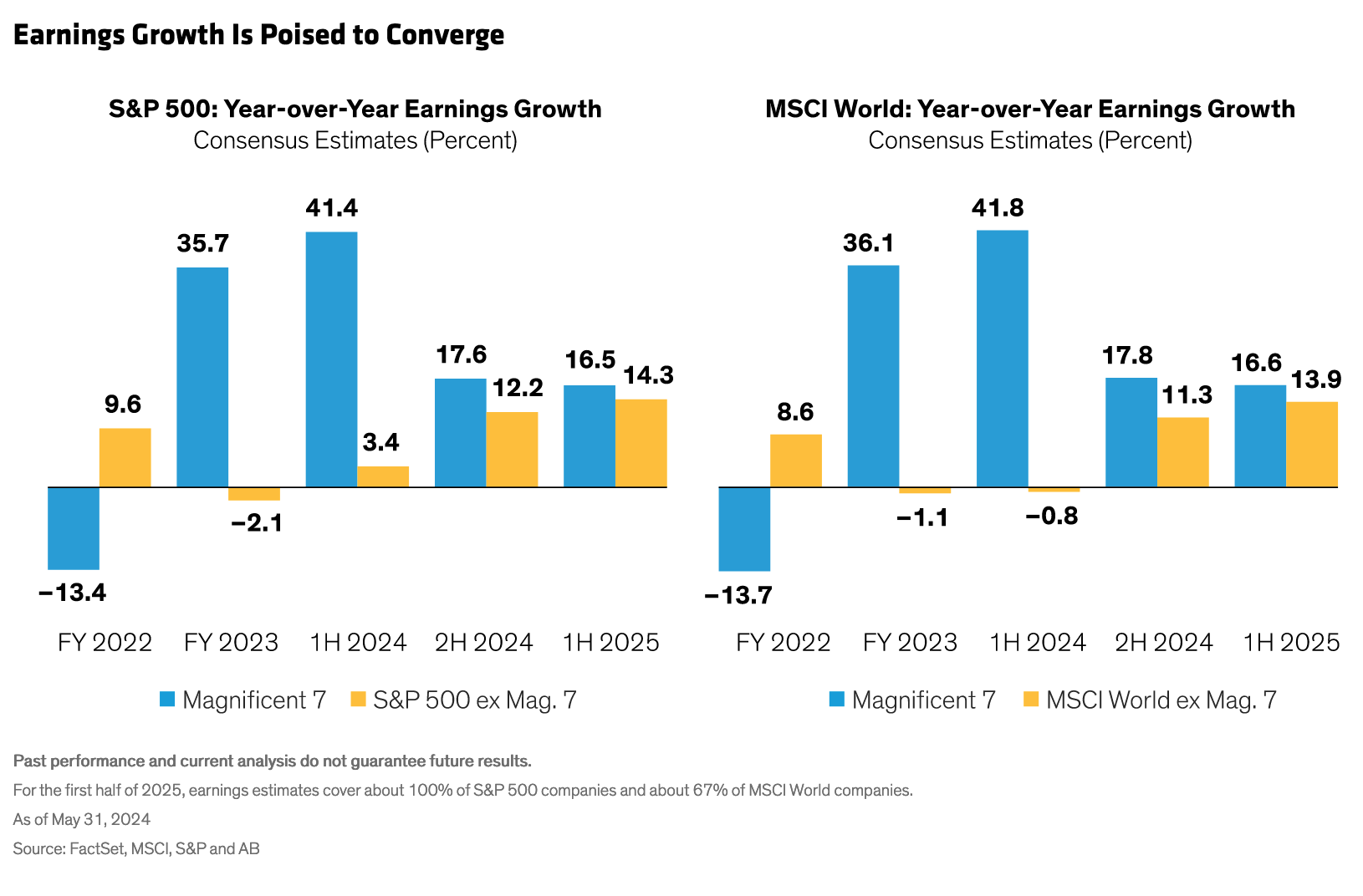

But change may be afoot. Some of the Magnificent Seven have faltered of late after earnings struggled to meet expectations. And within the group, the dispersion of returns between the best performers such as NVIDIA and Meta Platforms and the weaker names such as Tesla has continued to widen. There are also signs that market breadth is poised to widen. This is evidenced by a very low pairwise correlation of stocks, which indicates that individual names are trading more independently; our research suggests that this is a strong indicator of opportunity for active managers. In addition, earnings expectations for the broader global market are expected to converge toward the Magnificent Seven in the second half of 2024 and early 2025 (Display).

What About the “Magnificent Others”?

As market breadth widens, we see opportunities in what we call the “Magnificent Others.” These are firms that have sound balance sheets, consistent earnings streams and significant growth potential, but have not yet been rewarded by investors. Companies like these can be found across sectors and industries, including value segments and emerging markets, where many businesses aren’t tethered to local macroeconomic trends.

For example, in Europe, industrials make up nearly one-quarter of the MSCI Europe Growth Index—four times their weight in the comparable Russell 1000 Growth Index. Consensus earnings estimates for industrials in the MSCI Europe Growth Index are expected to increase to 15.9% by 2025—in line with estimates for the US technology sector. Many business models in the European industrials sector offer surprising sources of consistent growth, including companies that enable AI. While they may not make the GPU chips that power machine learning, some of these firms have earnings potential consistent with growth stocks.

The healthcare sector is also discovering how to use AI to unlock efficiencies and harness AI algorithms to create more effective drug candidates. Healthcare makes up 10% of global GDP—a structural tailwind that should gain momentum as developed-market populations age. These trends should help support solid long-term earnings growth among select companies with quality business models.

Punishing Misses, Yawning at Beats

Yet it’s clear that some high-quality companies aren’t getting the attention they deserve. Over the past decade, investors have shown a tendency to punish earnings misses, while brushing off companies that beat earnings forecasts.

This can be seen in the relative price responses following earnings releases. Our research shows that from a historical perspective, earnings beats are currently running higher than average, and yet high-performing firms haven’t been rewarded recently with subsequent price increases—in part due to the market dominance of a small number of mega-caps. By contrast, firms that have missed consensus earnings estimates have suffered blowback in the form of disproportionately large share-price hits (Display).

These asymmetric reactions could be one sign of an expensive market with little room for error. But they also underscore the case for active management, in our view. Given the high stakes of disappointing earnings growth—or, in some cases, downward revisions in earnings guidance—fundamental research can help separate successful firms from those at higher risk of earnings misses. At the same time, we believe it’s only a matter of time before companies with resilient business models and consistent earnings growth will be rewarded.

Investing Through a Period of Heightened Political Risk

As the third quarter progresses, we believe conditions are favorable for equities, but investors face uncertainty beyond just inflation and narrow market concentration—including changing political landscapes.

Wars in the Middle East and Ukraine continue to cast a shadow around the world, while US-China trade tensions simmer. After a big shift to the right in June’s European parliamentary elections, change could be coming to France and the UK, where elections will be decided in July. In emerging markets, recent elections in India, South Africa, Mexico and Argentina could lead to policy changes. And, of course, the world is anxiously awaiting the US elections in November.

But trying to make binary investment decisions based on political outcomes isn’t a prudent strategy for equity investors, in our view. History has shown that it’s notoriously difficult to forecast political results—often, the ultimate effect on economies, markets and companies is quite different than anticipated. It’s up to active managers to identify political risks and avoid companies exposed to acute risks that could overwhelm controllable financial results. The best antidote is to stay focused on business fundamentals and to identify companies that can overcome potential stresses from policy-driven decisions, such as tariffs.

If anything, we think heightened political and monetary policy risk reinforces the importance of active equities. Investors should seek to identify select companies that can consistently generate earnings above their cost of capital, which we view as a potent fundamental recipe for generating long-term returns. If investors can do this, they’ll be better able to assemble high-conviction portfolios that can withstand a range of exogenous challenges.

The MSCI data may not be further redistributed or used as a basis for other indices or any securities or financial products. This report is not approved, reviewed or produced by MSCI.

*****

About the Authors

Nelson Yu is a Senior Vice President, Head of Equities and a member of the firm’s Operating Committee. As Head of Equities, he is responsible for the management and strategic growth of AB’s equities business and investment decisions across the department. Since 1993, Yu has experience generating investment success in global equity markets by joining fundamental research with rigorous quantitative methods. He joined AB in 1997 as a programmer and analyst, and served as head of Quantitative Equity Research from 2014–2021. Since 2017, Yu also served as head of Multi-Style Core Equity strategies, with over $10 billion in assets. Most recently, he was CIO of Equities Investment Sciences and Insights, which brings together resources across Data Science, Quantitative Research, Advisory Services, Risk and Global Execution to deliver differentiated capabilities and insights to AB’s equities investment platform. Prior to joining AB, Yu was a supervising consultant at Grant Thornton. He holds a BSE in systems engineering from the University of Pennsylvania and a BS in Economics from the Wharton School at the University of Pennsylvania. Yu is a CFA charterholder. Location: New York

Copyright © AllianceBernstein