by Rich Mathieson, Senior Global Portfolio Manager, Systematic Equities, & Christopher DiPrimio, CAIA, Head of Americas Strategy, Systematic Equities, BlackRock

Key points

- The post-COVID era has seen increased market uncertainty and volatility, leading to a wider range of performance outcomes in stock and bond markets. Over this time, BlackRock’s Global Equity Market Neutral Fund (BDMIX) has consistently outperformed stocks and bonds whether markets were rising or falling.

- These results are driven in part by BDMIX’s ability to pursue uncorrelated alpha1 sources, benefit from higher interest rates, and remain nimble as market conditions continually evolve.

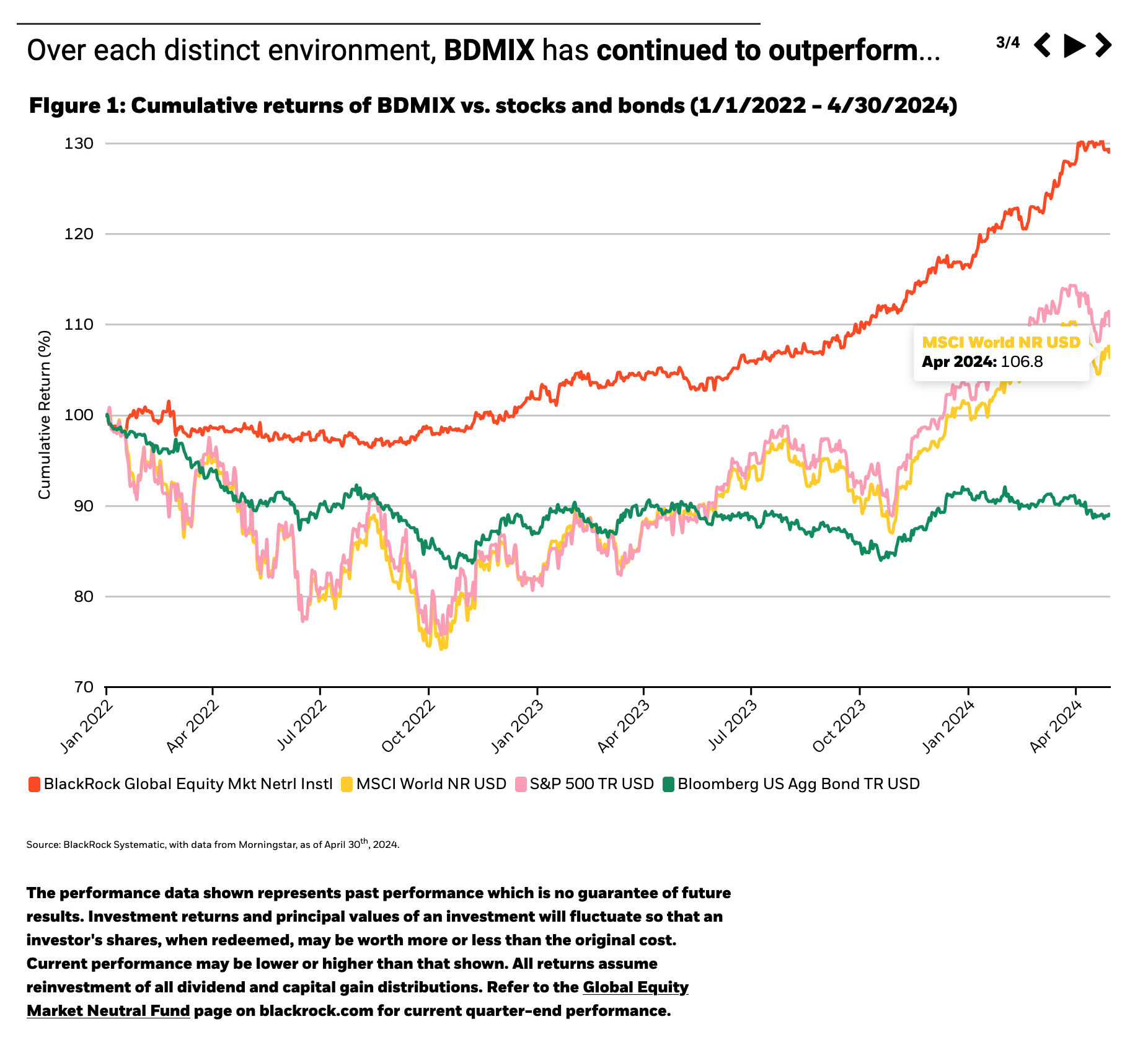

A defining feature of the post-COVID investment regime has been the persistence of elevated market uncertainty and volatility. The below visual highlights how this has led to a wider range of market performance outcomes, focusing in on the vast difference between the last two calendar years. Stock and bond markets delivered negative returns in 2022 amid high inflation and rapidly rising rates. In 2023, enthusiasm over artificial intelligence and growth opportunities largely boosted stock returns, followed by a sharp cross-asset rally as disinflation fueled expectations for a soft-landing.

Over the full two-year period and 2024 to date, the visual illustrates how BlackRock’s Global Equity Market Neutral Fund (BDMIX) consistently outperformed broad markets regardless of whether stocks and bonds were rising or falling. In a portfolio context, the strategy delivered equity-like returns with lower volatility and near-zero correlations to stock and bond markets.2 In this insight, we’ll explore the different dynamics underpinning these results, and the potential to help investors navigate continued uncertainty throughout 2024 and beyond.

Returns driven by dispersion, not market direction

The outperformance and low correlation of BDMIX returns to traditional assets has resulted in part from the strategy’s ability to benefit from cross-sectional dispersion in stock returns.

BDMIX seeks to take advantage of dispersion by investing in a relatively equal split of long and short positions across the global equity market. Compared to global indices or long-only equity strategies, the addition of short positions helps to offset directional market exposure. In this way, returns are primarily driven by manager skill in forecasting expected leaders (long holdings) and relative expected laggards (short positions) across markets.

Dispersion in security returns can in turn be linked back to dispersion in company earnings and cash flows. Post-COVID dynamics such as structurally higher inflation and nominal economic growth have contributed to more divergent company results. As a result, the strategy has enjoyed a richer opportunity set over the last two years than observed in the pre-COVID period. During this earlier period, secular disinflationary forces led to contracting dispersion in fundamentals across global stocks. For long/short investors with a clear edge in security selection, today’s higher dispersion environment enhances the opportunity to generate uncorrelated, diversifying alpha.

Higher interest rates boost total return potential

In addition to this enhanced alpha opportunity, BDMIX has also benefited from the higher interest rate backdrop that has prevailed over the last two years. The strategy employs active stock selection using derivatives3 that are highly liquid and capital efficient. This synthetic equity exposure is supported by the physical assets of the fund which are invested in short-term money market instruments such as treasury bills. The total return of the fund can therefore be analyzed as alpha on top of the yield generated on short-term cash.

A higher for longer interest rate environment creates a higher bar for traditional asset classes to outperform cash. In this environment, the ability of BDMIX to add alpha on top of current cash rates should continue to support total return potential and consistency.

Navigating highly changeable markets to identify new opportunities for alpha

From lockdown, to re-opening, to inflation, to soft-landing, and emergent themes such as banking stress and artificial intelligence, the post-COVID market regime has been characterized by highly changeable market dynamics. Static portfolio exposures and insights geared towards longer time horizons have typically struggled against the sharp rotations in leadership and styles.

In contrast, the strong emphasis placed on research and innovation within the investment process driving BDMIX has enabled the fund to effectively seek out the new opportunities for alpha arising from this changeable environment in real-time.

Each day, the data-driven analysis driven by this research is scaled across the full breadth of the global equity market—informing real-time forecasts for approximately 7,000 stocks. The strategy’s nimble, systematic implementation allows positioning to continually evolve and recalibrate to changing market drivers.

Putting it all together

The last two calendar years highlight the vastly different market environments unfolding in the post-COVID regime. As uncertainty presents persistent investment challenges, investors may want to consider complementing existing portfolio allocations with diversifying, uncorrelated alpha sources like BDMIX. The strategy has the potential to benefit from the current backdrop of increased dispersion and higher interest rates that is likely to persist—while maintaining a nimble approach to harnessing opportunities across changing markets.

Copyright © BlackRock