by Bob Elliott and Johann Colloredo-Mansfield, Unlimited Funds

Historically, 60/40 investors have relied on bonds to protect their equity positions and preserve capital through market down-turns. But over the past couple years, stocks and bonds have tended to move together more than they have in the past. In fact, the 12-month trailing stock-bond correlation reached as high as 70% in 2023 while it’s averaged -21% for the last 2 decades. In moments when bonds and stocks have sold off together, 60/40 investors might feel as if there is no place to hide. Fortunately, diversifying into gold, commodities, alpha strategies such as global macro and fixed income arbitrage can help mitigate the impact of extreme moves in the stock-bond correlation.

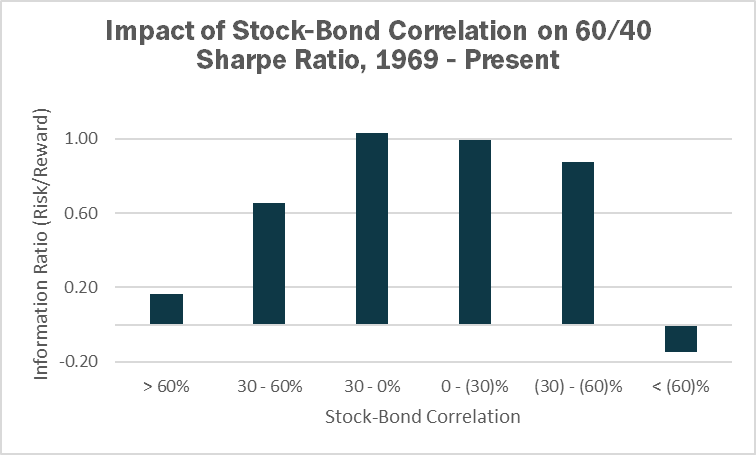

The figure below shows that a stock-bond portfolio offers a better risk-reward profile when correlations are bounded near 0. When correlations become either too negative or too positive, the Sharpe ratio of a stock-bond portfolio falls considerably. It would seem that the ‘magic’ of the 60/40 portfolio arises from the low average correlation of stocks and bonds, and not simply from the individual return characteristics of the two assets.

**Sources: FRED, Yahoo Finance, and Unlimited Calculations

The results depicted are aggregated results and do not represent returns that an investor attained. Past performance not indicative of future results.

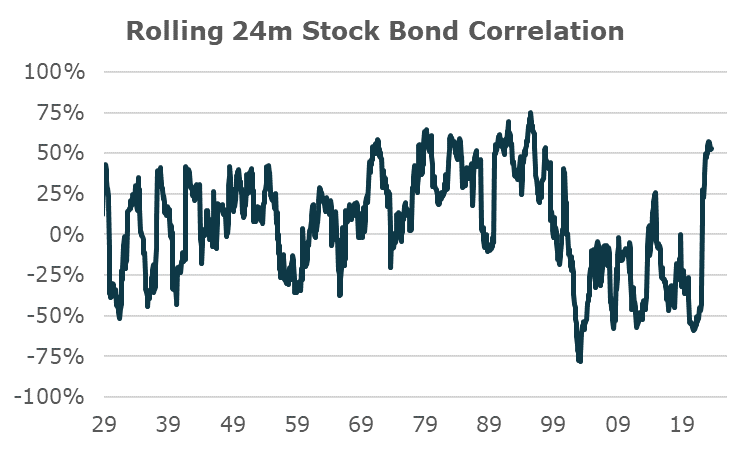

The correlation of any portfolio’s underlying strategies is a significant driver of overall risk-reward. So it should be a concern for investors that since 2021, the correlation between stocks and bonds – two major pillars of most portfolios – has increased precipitously. The figure below shows the rolling 24-month correlation between stocks and bonds since 1929. While the correlation was moderately positive through most history, it was largely negative since 2000, averaging -20%. This increase in correlations has reduced the diversification benefit bonds typically provide an equity portfolio.

**Sources: FRED, Yahoo Finance, and Unlimited Calculations

The results depicted are aggregated results and do not represent returns that an investor attained. Past performance not indicative of future results.

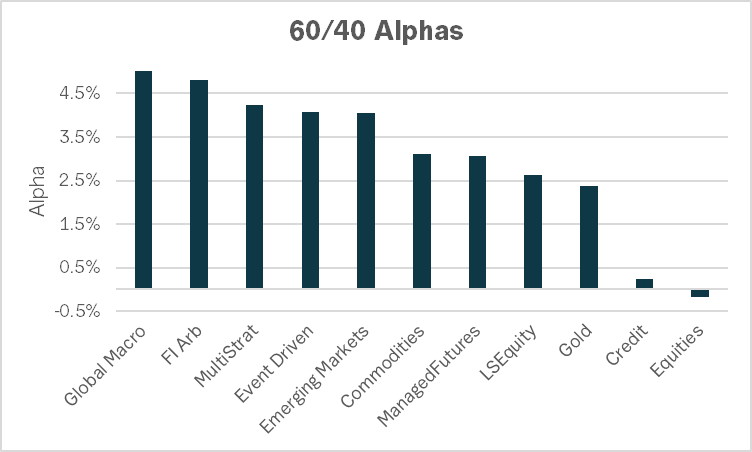

While the underlying dynamics are somewhat complicated, the headline news for 60/40 investors is clear: on days when stocks are down, bonds tend to be down too. A simple way to manage the risk posed by a changing stock-bond correlation is to look for other asset classes and alpha strategies that have had low historical correlations with the 60/40 portfolio. Using the average 12-month beta to the 60/40 portfolio since 1969 we calculate the alphas to gold, credit, equities, and commodities. Of these assets, commodities offer the largest 60/40 alpha at 3.0%. With the same approach we calculate the average 12-month beta to the 60/40 portfolio since 2002 for a panel of alpha strategies. Of these strategies, global macro offers the largest 60/40 alpha at 5%. Of course when thinking about alphas it’s important to consider how much you are paying for them, because this alpha can be eaten up by fees.

**Source: HFR, Barclayhedge, Credit Suisse, Bloomberg, FRED, Yahoo Finance, and Unlimited Calculations

The results depicted are aggregated results and do not represent returns that an investor attained. Past performance not indicative of future results.

If it seems like we at Unlimited make a big deal out of portfolio diversification, it’s because the data show that it works. Whether it’s managing market-timing, as we wrote about recently, or correlation risk, diversification can help counteract many of the forces that might dampen risk-reward in a portfolio setting. Gold, commodities, and alpha strategies can all play a part in controlling the uncertainty wrought by markets and changing macroeconomic conditions.

For informational and educational purposes only and should not be construed as investment advice. It does not constitute an offer to sell or a solicitation of an offer to buy any security. Opinions expressed are our present opinions only. No Representation is being made that any investment will or is likely to achieve profits or losses similar to those shown herein. No investment strategy or risk management technique can guarantee return or eliminate risk in any market environment. The material is based upon information which we consider reliable, but we do not represent that such information is accurate or complete, and it should not be relied upon as such. The historical analysis should not be construed as an indicator of the future performance of any investment vehicle that Unlimited manages.

Copyright © Unlimited Funds