by Edward D. Perks, CFA, Chief Investment Officer, Franklin Income Investors

Despite the US Federal Reserve’s cautious stance on interest rates and the shifting dynamics of the equity and fixed income markets, Franklin Income Investors CIO Ed Perks believes conditions are favorable for investing in these asset classes. This article provides an analysis of the latest economic and market trends and explores strategic opportunities to navigate through the current uncertain environment.

Key takeaways:

- The Fed continues to hold interest rates steady as it focuses on the totality of economic data before it begins to cut rates. Meanwhile, the markets now expect the Fed to cut rates only once toward the latter part of this year.

- Corporate bond spreads have tightened as the probability of a US recession has declined compared to a year ago.

- As the Fed eventually lowers interest rates, we believe corporate bonds, especially investment grade, could offer opportunities for both income and total return.

- While the broader equity market has been somewhat resilient, it has been fairly range-bound as many companies in different sectors have failed to meet earnings expectations.

- In our analysis, there are interesting opportunities in equities as the market overreacts to the short-term disappointments of high-quality companies we believe have longer-term potential.

Evolving inflation and interest-rate expectations

Looking back at these past six months, hotter-than-expected inflation data has shifted market expectations for interest-rate cuts in 2024. Going into the most recent Federal Open Market Committee Meeting (FOMC) meeting, some market participants were actually concerned we might see a hawkish Federal Reserve (Fed) and some talk of fed funds rate hikes coming. However, Fed Chairman Jerome Powell put these worries to rest and stressed that policymakers are looking at the totality of data and not just pieces of economic data that might not be pointing in the same direction.

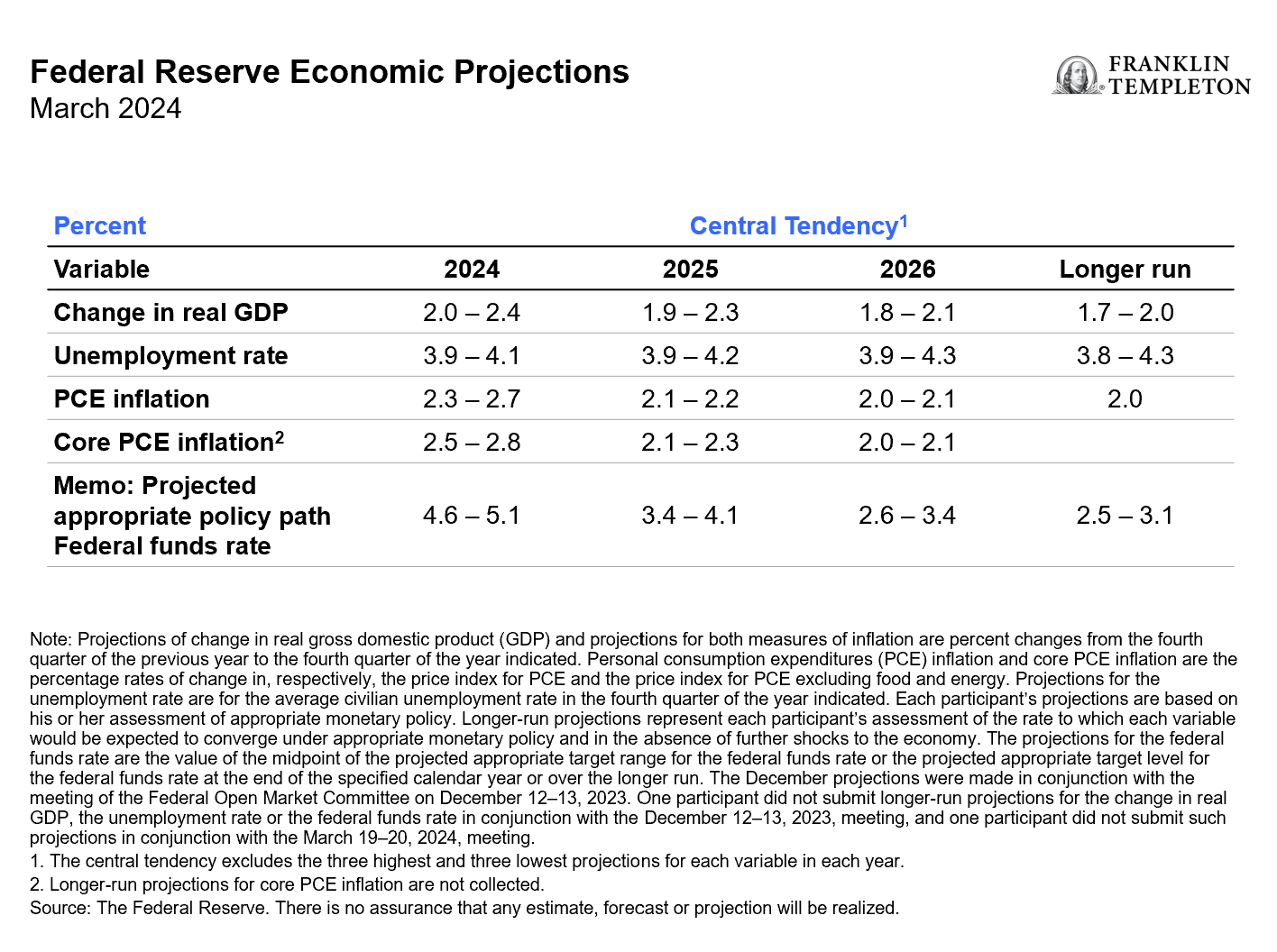

In our opinion, the Fed’s March summary of economic projections, as shown in Exhibit 1, is about as good as it gets. The Fed expects gross domestic product (GDP) growth to remain resilient and maintain a level above longer-term expectations. Similarly, Fed policymakers do not foresee unemployment rising materially over the next several years despite the tightening they put in place. In our opinion, with initial jobless claims increasing to the highest level in quite some time, comprehensive labor market surveys may be overstating job growth. Thus, the labor market will be a key focal point for us in the near term.

Exhibit 1: FOMC Summary of Economic Projections (right click on chart to enlarge)

Turning to inflation, the latest reading of the year-over-year Core Personal Consumption Expenditure Index (PCE) was around 2.8%, which is at the upper end of the Fed’s projections and within reach of its 2.6% median. The Fed expects core PCE to go down to its target at which point it will gradually normalize the fed funds rate over the next several years. The Fed’s projected fed funds rate by year-end is 4.6%–5.1%.1 We will certainly watch how the Fed’s projections will change—the next release is in June—and what these will tell us about monetary policy going forward.

As of now, we believe the Fed will likely stay on hold through the end of the summer and possibly start cutting rates thereafter. The market, which was pricing in three—and even as high as six or seven—rate cuts through the end of 2024, is currently pricing only one cut this year.

Tighter corporate bond spreads and still-elevated yields

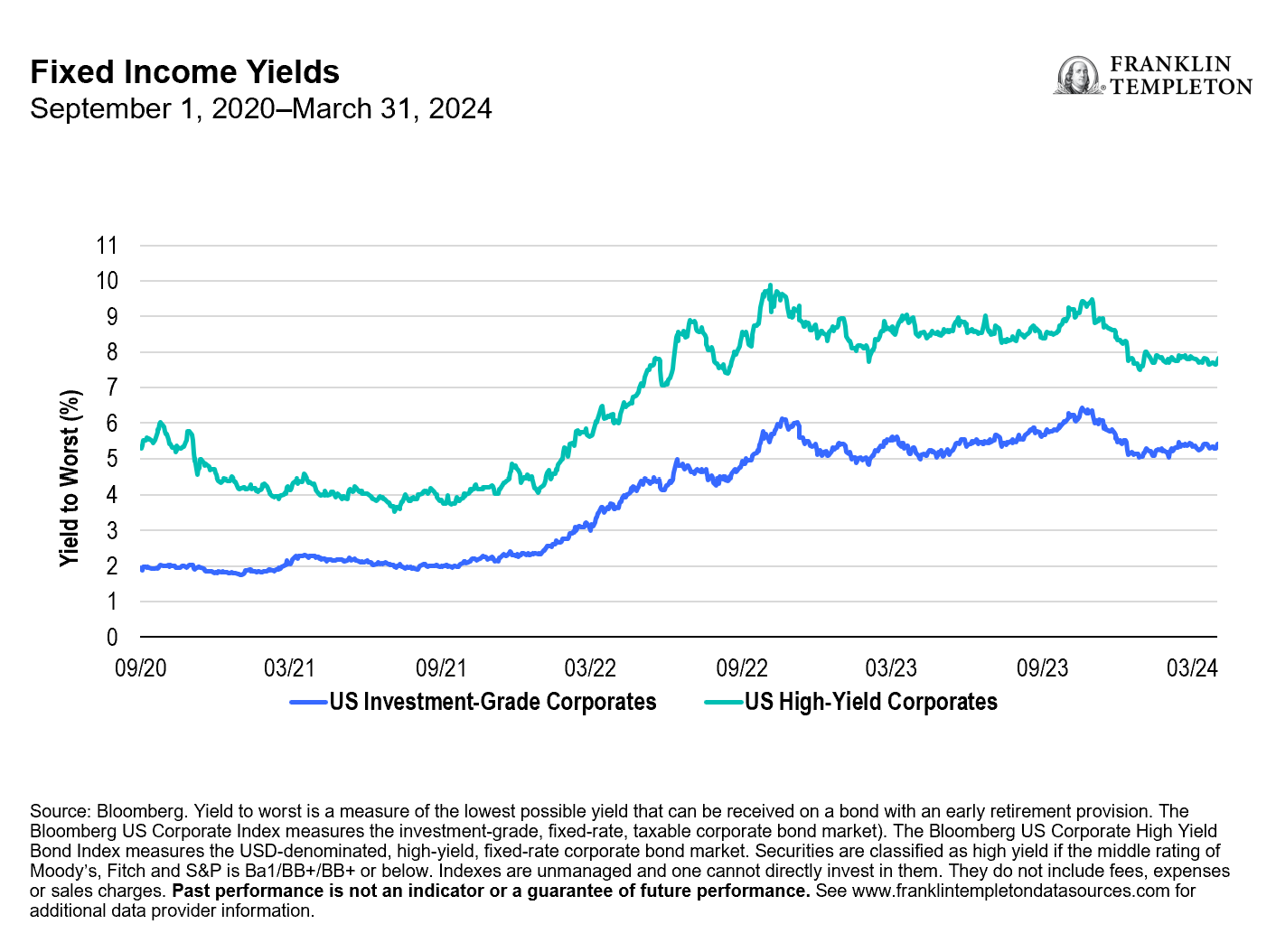

Relative to a year ago, we’ve seen a substantial spread contraction in both the investment-grade corporate bond (as measured by Bloomberg US Corporate Index) and the high-yield corporate bond (as measured by the Bloomberg US Corporate High Yield Bond Index) universes.2 Spreads were wider a year ago because the probability of a US recession was significantly higher then than it is today.3 This scenario gave us a nice opportunity in terms of yields. As the recession probability has declined and corporate fundamentals have remained resilient, we’ve seen spreads contract to levels that are closer to historical tight ranges. Investment-grade corporate bonds, which were around 150 basis points (bps) over comparable maturity US Treasuries a year ago, are down to around 100 bps. High-yield bonds, which were around 500 bps, are now down to around 300 bps.4 As long as corporate fundamentals remain intact, to us this isn’t cause for alarm as we’ve historically seen spreads stay at similar levels for extended periods of time. And, these yields are priced off of still-elevated US Treasury yields.

As shown in Exhibit 2, corporate bond yields declined to historical lows in 2020 (resulting in very high bond prices) and then yields rose to elevated levels in 2022 (resulting in bond prices falling precipitously). Since then, yields have been what we consider very attractive relative to what we’ve seen in the last decade and a half. For instance, coupons for investment-grade corporate bonds (currently our preferred sector within fixed income) have been around 5.5%.5 In our opinion, this could provide a good opportunity, particularly as we think about extending duration and potentially benefiting from a longer-term normalization in interest rates.

Exhibit 2: Yields are Attractive Despite Recent Rally (right click on chart to enlarge)

Right now, cash and short-term fixed income assets offer what we consider an attractive income level. However, as the Fed eventually lowers interest rates in the next 6-18 months, we believe the differential between shorter-term fixed income and longer-duration corporate securities will be substantial, in addition to the latter’s total return opportunity.

Additionally, as we look at these ranges of yields, especially combined with the average bond prices in each of these universes, they’re still around 8%–10% below par value.6 This presents the opportunity to buy bonds not only with attractive yields but also below their face value.

Broader opportunities in equities

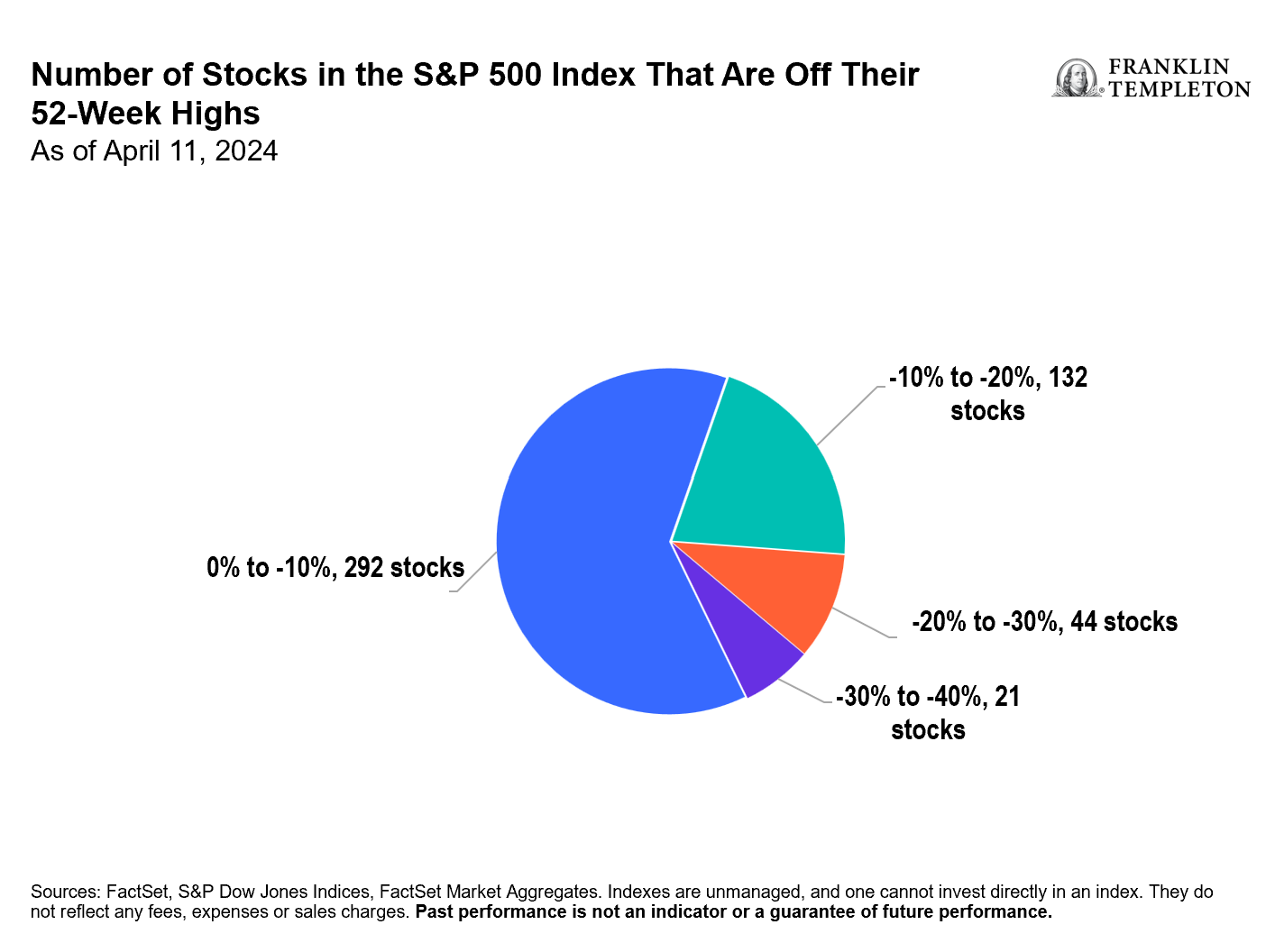

While the Magnificent Seven7 companies were an important driver in the equity market last year, there has been some broadening as well as some divergence so far this year. Based on the most recent earnings season that has largely wrapped up, many companies in different sectors have failed to meet expectations and thus, have been unable to move the broader indexes to a higher level. So, while the broader equity market has been somewhat resilient, it has been fairly range-bound. For instance, the Standard & Poor’s 500 Index has largely gone sideways from around 5100 in early March to 5200 in early May.

In our analysis, with overall market expectations still high for the rest of the year and into next year, underneath the surface more than 40% of the broader universe of stocks have declined (see Exhibit 3). These are the areas we believe we can find some interesting opportunities. In fact, we’ve been able to move some of our income strategies away from fixed income, particularly non-investment grade, toward some of these opportunities in equities.

Exhibit 3: Select Opportunities in Equities (right click on chart to enlarge)

Through the rest of this year, we expect to gradually pursue a bit more balance between equity and fixed income. Our equity focus is on companies with good long-term potential, and where we believe there are attractive valuations and income potential. This includes dividend-paying common stocks, convertibles, traditional preferred securities and equity-linked notes (ELNs).8

We believe it is important to maintain diversification across sectors. Within equities, we’ve moderated some of our exposure in financials as valuations in the bigger US banks have recovered. Conversely, we’ve increased our exposure to health care, energy and utilities. We’ve also found opportunities to participate in the artificial intelligence (AI) revolution through some technology companies’ ELNs, as more companies are adopting AI to improve their operations and as the energy and electric utilities sectors begin to benefit from AI’s increasing power usage.

Conclusion

While there is some uncertainty on the forward path of the economy and monetary policy as well as the impact that the US elections could have as we get into the latter part of this year, our strategy is to maintain a highly diversified portfolio and employ a dynamic approach across all asset classes.

*****

WHAT ARE THE RISKS?

All investments involve risks, including possible loss of principal.

Equity securities are subject to price fluctuation and possible loss of principal. Dividends may fluctuate and are not guaranteed, and a company may reduce or eliminate its dividend at any time.

Convertible securities are subject to the risks of stocks when the underlying stock price is high relative to the conversion price and debt securities when the underlying stock price is low relative to the conversion price. Investments in equity-linked notes often have risks similar to their underlying securities, which could include management risk, market risk and, as applicable, foreign securities and currency risks.

Fixed income securities involve interest rate, credit, inflation and reinvestment risks, and possible loss of principal. As interest rates rise, the value of fixed income securities falls. Low-rated, high-yield bonds are subject to greater price volatility, illiquidity and possibility of default.

Investments in fast-growing industries like the technology and health care sector (which historically has been volatile) could result in increased price fluctuation, especially over the short term, due to the rapid pace of product change and development and changes in government regulation of companies emphasizing scientific or technological advancement or regulatory approval for new drugs and medical instruments.

Any companies and/or case studies referenced herein are used solely for illustrative purposes; any investment may or may not be currently held by any portfolio advised by Franklin Templeton. The information provided is not a recommendation or individual investment advice for any particular security, strategy, or investment product and is not an indication of the trading intent of any Franklin Templeton managed portfolio.

IMPORTANT LEGAL INFORMATION

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice. This material may not be reproduced, distributed or published without prior written permission from Franklin Templeton.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as at publication date and may change without notice. The underlying assumptions and these views are subject to change based on market and other conditions and may differ from other portfolio managers or of the firm as a whole. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market. There is no assurance that any prediction, projection or forecast on the economy, stock market, bond market or the economic trends of the markets will be realized. The value of investments and the income from them can go down as well as up and you may not get back the full amount that you invested. Past performance is not necessarily indicative nor a guarantee of future performance. All investments involve risks, including possible loss of principal.

Any research and analysis contained in this material has been procured by Franklin Templeton for its own purposes and may be acted upon in that connection and, as such, is provided to you incidentally. Data from third party sources may have been used in the preparation of this material and Franklin Templeton (“FT”) has not independently verified, validated or audited such data. Although information has been obtained from sources that Franklin Templeton believes to be reliable, no guarantee can be given as to its accuracy and such information may be incomplete or condensed and may be subject to change at any time without notice. The mention of any individual securities should neither constitute nor be construed as a recommendation to purchase, hold or sell any securities, and the information provided regarding such individual securities (if any) is not a sufficient basis upon which to make an investment decision. FT accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FT affiliates and/or their distributors as local laws and regulation permits. Please consult your own financial professional or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

Please visit www.franklinresources.com to be directed to your local Franklin Templeton website.

CFA® and Chartered Financial Analyst® are trademarks owned by CFA Institute.

__________

1. There is no assurance that any estimate, forecast or projection will be realized.

2. Source: Bloomberg. As of March 31, 2024. The Bloomberg US Corporate Index measures the investment-grade, fixed-rate, taxable corporate bond market). The Bloomberg US Corporate High Yield Bond Index measures the USD-denominated, high-yield, fixed-rate corporate bond market. Securities are classified as high yield if the middle rating of Moody’s, Fitch and S&P is Ba1/BB+/BB+ or below. Indexes are unmanaged and one cannot directly invest in them. They do not include fees, expenses or sales charges. Past performance is not an indicator or a guarantee of future performance. See www.franklintempletondatasources.com for additional data provider information.

3. Source: Bloomberg. As of March 31, 2024. The ICE BofA Option-Adjusted Spreads (OASs) are the calculated spreads between a computed OAS index of all bonds in a given rating category and a spot Treasury curve. Indexes are unmanaged and one cannot directly invest in them. They do not include fees, expenses or sales charges. Past performance is not an indicator or a guarantee of future performance. See www.franklintempletondatasources.com for additional data provider information.

4. Source: Bloomberg. As of March 31, 2024.

5. Ibid.

6. Ibid.

7. The “Magnificent Seven” are Alphabet, Amazon, Apple, Meta, Microsoft, Nvidia and Tesla.

8. Equity-linked notes are hybrid securities, whose overall return is linked to the price performance of an underlying stock plus a coupon received, and which may provide income and capital appreciation opportunities, lower downside risk and an expanded investment universe.

Copyright © Franklin Income Investors