by Vaibhav Tandon, Senior Economist, Northern Trust

Sanctions have not been as powerful as expected.

In many sports, the referee can call a penalty when a player commits a foul. In economics, when a country breaks the rules, it attracts penalties in the form of sanctions.

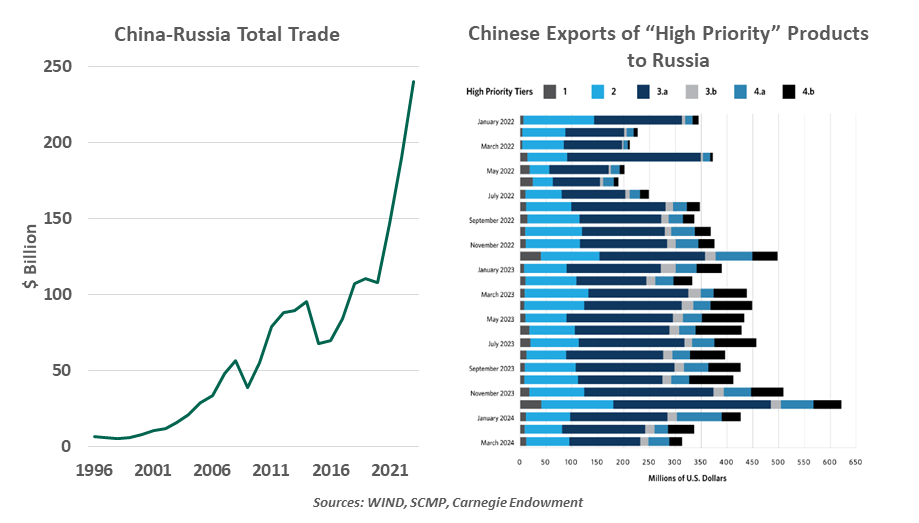

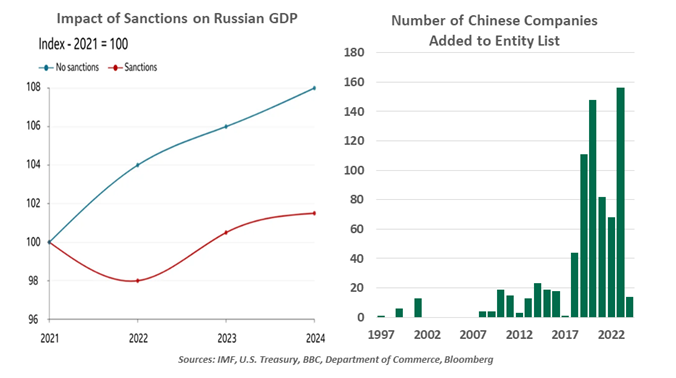

Last week, the U.S. unleashed a wave of nearly 300 new penalties aimed at disrupting Moscow’s military-industrial base amid the ongoing Ukraine war. Among those sanctioned are 20 Chinese companies. Russia’s trade with China has surged since the start of the Ukraine war, making it Beijing’s sixth-largest trading partner in 2023. Chinese exports to Russia have risen by more than 60% in the past two years; China is now the nation’s largest supplier of commercial goods.

It is the increasing supply of “high priority” or dual-use components that has drawn America’s ire. This category includes alumina, optical instruments and microelectronic components essential for manufacturing weaponry. China was responsible for about 90% of Russia’s imports of goods covered under the Group of Seven (G7) nation’s “high priority” export control list in 2023, up from one-third before the start of the war.

The imposition of sanctions covering Chinese entities represents a significant move that could further strain relations between the world’s two largest economies. And it has raised questions about the effectiveness of these penalties as a deterrent against bad actors.

Sanctions have been a key part of the U.S. policy toolkit, but are increasingly becoming easy to evade unless they have strong multilateral support. With over 16,000 sanctions against it, Russia was already the world’s most penalized country. These unprecedented measures were expected to impair the Russian economy and its military-industrial base. Instead, Russia adapted by turning to markets like China and India for its most important exports, allowing sustained economic growth. Russia remains one of the world's largest oil exporters, which is helping it fund military, social and other spending without stressing its finances.

Sanctions have brought some pain to the Russian economy. According to U.S. Treasury calculations, these measures have cut 5% from the economic growth it might have had over the past couple of years. Moscow has lost access to $300 billion of its foreign exchange reserves held by G7 nations, while its currency has lost almost a fifth of its value against the U.S. dollar. Russia’s industrial base has been crippled, which contributed to an inflationary environment.

The effectiveness of sanctions has eroded; not so for Russia’s military-industrial base.

The U.S. still has some powerful options at its disposal as it seeks to limit Russia. Among the most extreme measures would be weaponizing the dollar by removing Chinese financial institutions from the global financial system if they fail to curb support for Russia. But such a move would severely disrupt global trade, as China is a main trading partner for many nations. Further, cutting Chinese financial institutions off from the global financial network will only boost adoption of Beijing’s Cross-Border Interbank Payment System and the yuan in the longer run

These factors explain Washington’s measured response towards Chinese entities. By avoiding more punitive measures now, the U.S. is also likely seeking to preserve its leverage for future strategic contests with Beijing.

The West needs to focus on improving the enforcement of and compliance with economic sanctions as they become a tool of first resort. Only then will penalties lead to goals.