by Ryan Boyle, Senior Economist, Northern Trust

Owning a home has many virtues: it creates stability for a family, supports longer-lasting connections in a community and is a store of wealth for the home owner. For these reasons, home purchases have been both a personal aspiration and a policy priority for generations.

Today, these preferences have led to a fundamental imbalance. Potential buyers are finding a paucity of homes available for purchase.

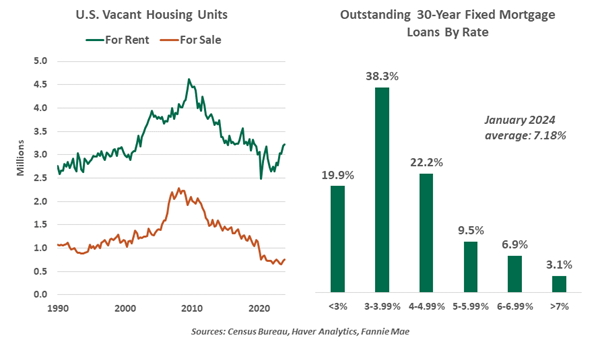

The stock of homes for sale in the U.S. has fallen to levels last seen in the mid-1990s. Data provider Redfin observes the inventory of homes on the market holding in a range consistently more than a third lower than its pre-pandemic norms. Housing stock has not kept pace with population growth in many parts of the country. Higher interest rates were expected to cool the market, but with supply so constrained, house prices have continued to climb.

We can now look back on the pre-pandemic economic cycle and say that housing was under-built. After a housing bubble ignited a global financial crisis, caution from home builders was understandable. Residential investors were once bitten, twice shy. However, the steady recovery has equipped more consumers to step into home ownership; Millennials are ready to buy.

And then the stay-at-home urgency of the pandemic further distorted housing markets. The need for home office space prompted a rush to purchase homes and/or relocate in 2020 and 2021, leaving inventories depleted.

Supplies got tighter from there. Those who still carried mortgage debt were able to refinance into new loans at very low rates. But as mortgage costs rose in 2022 and 2023, yesterday’s bargain became today’s albatross. Trading up to a new property entails not only paying a large sticker price, but a reset to a substantially higher mortgage interest rate. Some homeowners are therefore opting to stay put as long as possible.

The logjam is not solely caused by mortgagors. Those who own their property free and clear have strong incentives to keep them. While cashing out a home’s elevated equity is tempting, the rent or purchase price of a new property would consume much of the gains from sale. And the cost of living would creep higher; properties sold long ago usually benefit from relatively low property taxes in many locations.

Homeowners without mortgages skew older, and a growing share of this cohort is choosing to age in place. A 2021 survey by the American Advisors Group (AAG) found more than 80% of seniors intend to spend the remainder of their lives in their current homes.

High demand for housing is a good economic sign, but low supply is limiting sales.

Residential property is the most valuable asset of most households. Older homeowners desire to protect that nest egg for their children, or value the security of being able to borrow against it in an emergency. The limited building activity in recent cycles has constrained the inventory of smaller residences, like condominiums and townhomes, that may be better for empty nesters.

Emotionally, occupants grow attached to familiar surroundings, even if that means staying in a mostly empty residence. The AAG survey found clear majorities of respondents not only regard their homes as the best financial decision they ever made, but as very safe space.

The choice to stay in a home that is too large for an individual’s needs may be individually defensible, but it adds to the distorted supply in the market. The best remedy we can see is to build more housing, for younger and older buyers alike—but this may require difficult reforms to restrictive local land use and preservation policies. Multi-generational living arrangements are on the rise, with financial issues representing the top reason for adults to combine households, followed by caregiving.

Stepping into homeownership is an important investment and milestone. Some additional supply will help give more families an opportunity to achieve the American dream.

Copyright © Northern Trust