by Craig Basinger, Chief Market Strategist, Purpose Investments Inc.

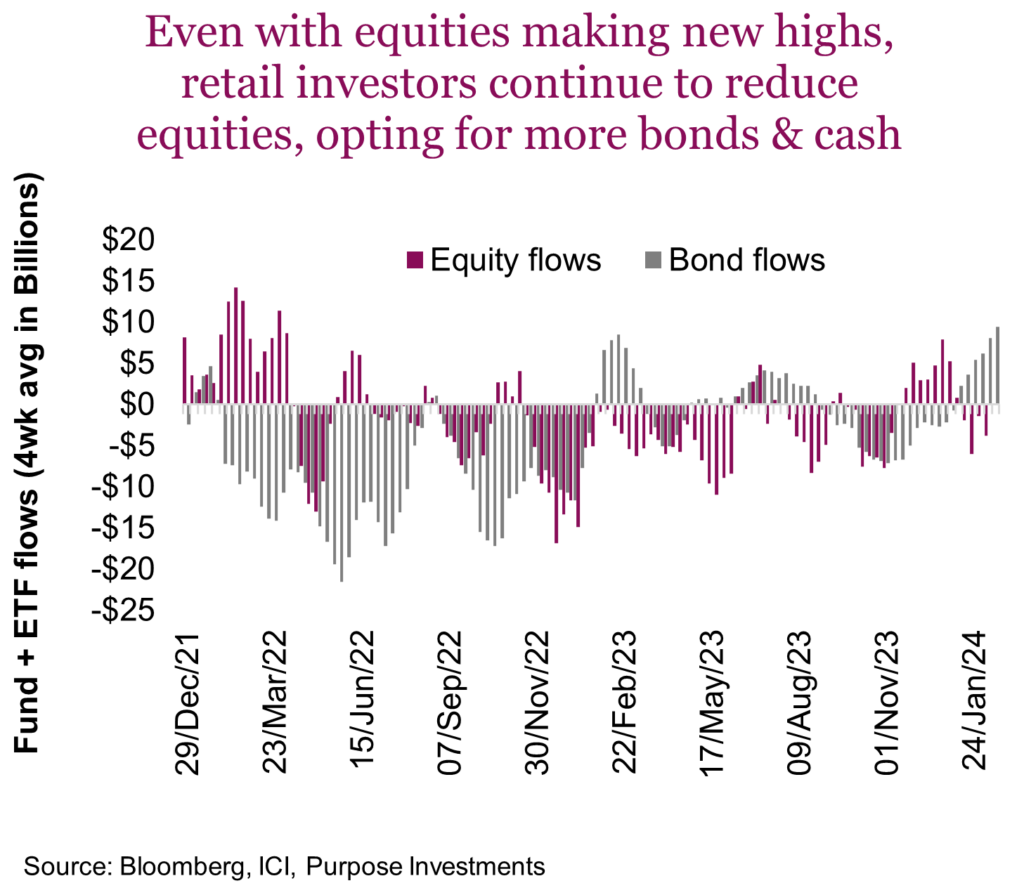

So far this year, investors have been piling into cash, adding to bonds, and sucking money out of equities. Apologies, we are going to use U.S. listed data here, for convenience and because larger numbers are more fun. Based on Investment Company Institute (ICI) data, investors have sucked $25B out of equities, added $122 billion to cash and added $52 billion to bonds. The chart below is the rolling 4-week average flows into bonds and equities. Equities have remained sporadic over the past few years, with brief periods of inflows and outflows. In 2023, a solid year in the market, equity outflows were $133 billion, so the trend in 2024 remains much the same. Bonds, which experienced HUGE outflows in 2022 as yields rose, have been seeing more inflows of late.

While equity flows have been negative in aggregate, it does appear largely broad-based U.S. exposure is being reduced. International is up a little and if ETF flows are any indication, technology is attracting some flows. But we are going to pivot to cash and bonds. It shouldn’t be too surprising that the inflows to cash and bonds, with the most attractive yields in many years, is a strong lure.

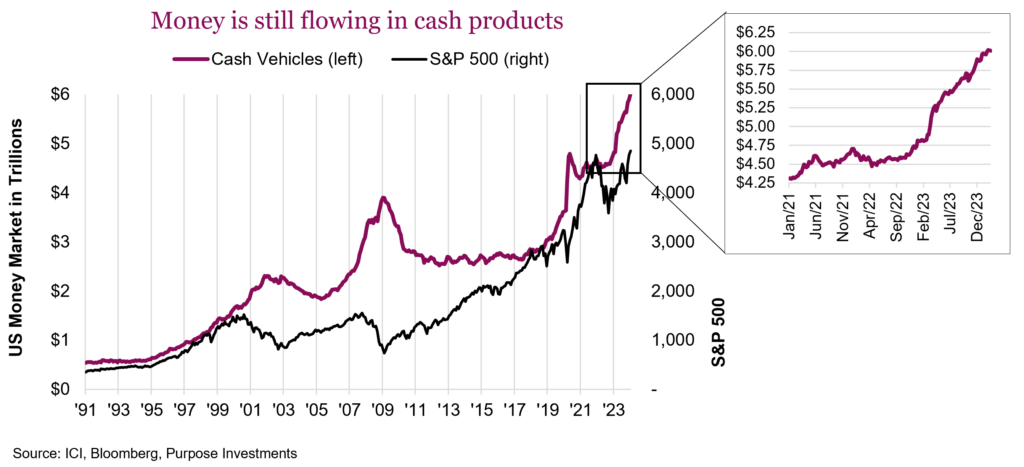

The flow into cash vehicles has been incredible. Even more incredible is that cash inflows have historically coincided with periods of market weakness (see 2001, 2008, 2020 in chart below). Yet these current inflows are more about capital being attracted by a decent yield as opposed to capital fleeing equity markets looking for a place to hide. More of a pull than a push. It is also important to differentiate where the dollars are coming from. If simply moving from a bank account that pays very little to a higher yield vehicle, it is possible that money will never move into more risk assets such as stocks or bonds. But some will and that is one pile of cash sitting there.

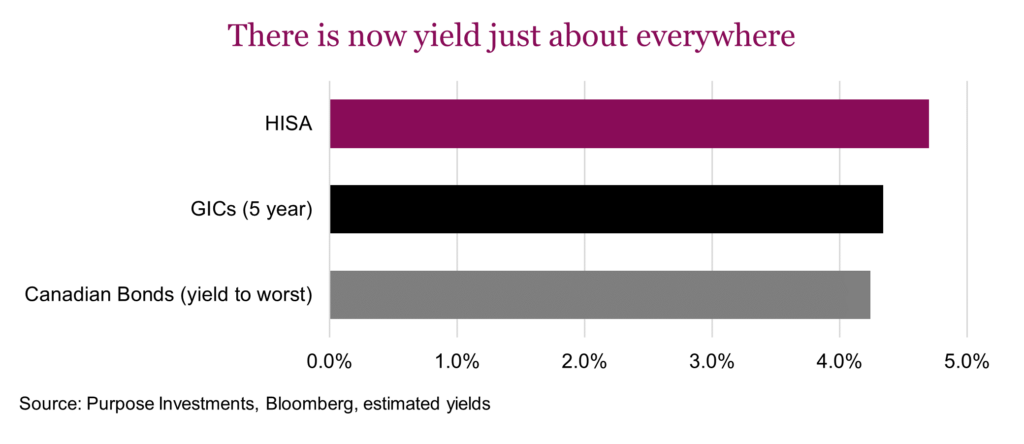

Higher yields everywhere from cash, to GICs, to bonds, even to dividend-paying equities has created perhaps one of the most recurring questions of the past year – which is best between cash, GICs and bonds? We will tackle the dividend equities in another instalment.

Cash, GICs or bonds?

There is no simple answer as much depends on the purpose of the capital and what happens next in these markets. For simplicity, we will reference High Interest Savings Accounts for cash, and we pulled a preferred GIC offering as our proxy for GICs. Naturally, these are just estimates or approximations.

The really interesting aspect today is how similar yields have become across the three options. HISAs, even after the changing legislations, are carrying a yield between 4.5-5%. GICs are a bit lower, above the 4% level. And bonds, which do carry a lower current yield in the 3-3.5% range, have a baked-in gain given most are trading at a discount to par, which brings the yield to worst up to around 4.2%. So really, they are all kind of clustered together offering some decent yields.

Each of the three options does offer rather different characteristics that will behave differently depending on what markets and rates do in the coming quarters or years. The table below really tries to capture some of the more pertinent characteristics of each.

It really depends on what happens next. Here are three simplistic scenarios, with who wins or loses test among HISA vs GICs vs bonds.

These are very simple scenarios but clearly demonstrate some of the pros and cons of each option. Yet there are some even more important considerations. If the capital is just looking for a higher rate from say a chequing account, just lock in with GIC or go variable with a HISA. However, if the capital is part of an overall portfolio, it’s a bit more complicated.

Bonds tend to do well when the market goes risk-off (aka equities lower) – This is the reflexive nature of bonds and equities. While it doesn’t always work, like in 2022, it does work most of the time. Bonds provide a ballast for the portfolio and often will move in the opposite direction, especially when equities are falling. HISA and GICs offer price stability but not this reflexive behavior.

Optionality – What if equities fall 20 or 30%? The ability to rebalance during more volatile periods in the market is a very important process that adds value over time. If too much capital is locked in, this reduces the ability to rebalance. Bonds and HISAs offer optionality.

Final thoughts

There is no right or wrong answer to the original question, in fact much depends on the purpose of the capital and what happens next in the market. And while that may complicate the process, at least today there are many choices and options to find yield. A few years ago, the demand for cash, GICs and even bonds were far less than today. It’s nice to have choices.

Sign up here to receive the Market Ethos by email.

Source: Charts are sourced to Bloomberg L.P., Purpose Investments Inc., and Richardson Wealth unless otherwise noted.

The contents of this publication were researched, written and produced by Purpose Investments Inc. and are used by Richardson Wealth Limited for information purposes only.

*This report is authored by Craig Basinger, Chief Market Strategist at Purpose Investments Inc. Effective September 1, 2021, Craig Basinger has transitioned to Purpose Investments Inc.

Disclaimers

Richardson Wealth Limited

The opinions expressed in this report are the opinions of the author and readers should not assume they reflect the opinions or recommendations of Richardson Wealth Limited or its affiliates. Assumptions, opinions and estimates constitute the author’s judgment as of the date of this material and are subject to change without notice. We do not warrant the completeness or accuracy of this material, and it should not be relied upon as such. Before acting on any recommendation, you should consider whether it is suitable for your particular circumstances and, if necessary, seek professional advice. Past performance is not indicative of future results. The comments contained herein are general in nature and are not intended to be, nor should be construed to be, legal or tax advice to any particular individual. Accordingly, individuals should consult their own legal or tax advisors for advice with respect to the tax consequences to them.

Richardson Wealth is a trademark of James Richardson & Sons, Limited used under license.

Purpose Investments Inc.

Purpose Investments Inc. is a registered securities entity. Commissions, trailing commissions, management fees and expenses all may be associated with investment funds. Please read the prospectus before investing. If the securities are purchased or sold on a stock exchange, you may pay more or receive less than the current net asset value. Investment funds are not guaranteed, their values change frequently and past performance may not be repeated.

Forward Looking Statements

Forward-looking statements are based on current expectations, estimates, forecasts and projections based on beliefs and assumptions made by author. These statements involve risks and uncertainties and are not guarantees of future performance or results and no assurance can be given that these estimates and expectations will prove to have been correct, and actual outcomes and results may differ materially from what is expressed, implied or projected in such forward-looking statements. Assumptions, opinions and estimates constitute the author’s judgment as of the date of this material and are subject to change without notice. Neither Purpose Investments nor Richardson Wealth warrant the completeness or accuracy of this material, and it should not be relied upon as such. Before acting on any recommendation, you should consider whether it is suitable for your particular circumstances and, if necessary, seek professional advice. Past performance is not indicative of future results. These estimates and expectations involve risks and uncertainties and are not guarantees of future performance or results and no assurance can be given that these estimates and expectations will prove to have been correct, and actual outcomes and results may differ materially from what is expressed, implied or projected in such forward-looking statements. Unless required by applicable law, it is not undertaken, and specifically disclaimed, that there is any intention or obligation to update or revise the forward-looking statements, whether as a result of new information, future events or otherwise.

Before acting on any recommendation, you should consider whether it is suitable for your particular circumstances and, if necessary, seek professional advice.

The particulars contained herein were obtained from sources which we believe are reliable but are not guaranteed by us and may be incomplete. This is not an official publication or research report of either Richardson Wealth or Purpose Investments, and this is not to be used as a solicitation in any jurisdiction.

This document is not for public distribution, is for informational purposes only, and is not being delivered to you in the context of an offering of any securities, nor is it a recommendation or solicitation to buy, hold or sell any security.

Richardson Wealth Limited, Member Canadian Investor Protection Fund.

Richardson Wealth is a trademark of James Richardson & Sons, Limited used under license.

Copyright © Purpose Investments Inc.