by Kristina Hooper, Chief Global Market Strategist, Invesco

Key takeaways

Bank concernsOn Jan. 30, concerns about regional banks were reignited when New York Community Bank (NYCB) revealed that its earnings were well below expectations. |

Sector impactWhile we’re seeing an impact on regional bank stock prices, we believe the problems remain contained to a small portion of smaller banks. |

Market reactionThe S&P 500 Index shrugged off the news and made gains despite bank headlines, topping the 5,000 mark for the first time ever last week. |

Last spring saw a sell-off in regional bank stocks as several smaller banks failed, starting with Silicon Valley Bank. The situation ultimately cooled down, but we always had a sense that, while the situation was contained, there could be flare ups in the form of one or a few individual banks that came under pressure. In late January, concerns about a regional bank crisis were reignited when New York Community Bank (NYCB) revealed that its earnings were well below expectations. While we’re seeing an impact on the stock prices of some regional banks in the US — and globally — we believe these problems remain isolated, contained to a small portion of the smaller banks.

What happened with New York Community Bank?

Most of New York Community Bank’s issues are rather unique. Its problems stem partly from its acquisition of Signature Bank’s assets last spring when that bank failed; that put NYCB into a different bank category — Category IV (assets over $100 billion) — which means greater regulation in general, including higher capital, liquidity, and loan loss requirements.

NYCB’s decision to strengthen its balance sheet liquidity in line with its peer group was an important contributor to the earnings miss and the dividend cut. Also, the bank, which has a relatively high exposure to commercial real estate, wrote off some distressed loans in the fourth quarter — although two loans with special circumstances accounted for much of the charge-offs in the period.

Investors are clearly worried about NYCB, sending its stock price down dramatically since the earnings announcement, although it has stabilized in the last several trading days. NYCB does have a relatively low Tier 1 capital ratio; it is under 10% versus 12.3% on average for US banks.1 On the positive side, NYCB has a relatively higher percentage of insured deposits, which means less flight risk for deposits, and its underlying operating performance was strong. Finally, the departure of senior executives may point to issues that could be specific to NYCB.

What’s the impact on US regional banks?

Because of NYCB’s woes, a reverse halo effect, not dissimilar to last spring, has started to impact regional banks in the US — and globally. The S&P 500 Regional Banks Index has fallen 8.9% year-to-date.2 US regional bank bonds have experienced widening spreads, indicating that markets view them as riskier. But in our view, there is only a small subset of US regional banks that have material vulnerabilities. It is their stocks that are being most punished by investors.

The reality is that, in general, US banks are well-capitalized. Based on the latest aggregate sector balance sheet data by the US Federal Reserve (Fed), there is enough cash to cover commercial real estate loans in their entirety.3 The issue is that, generally speaking, the smaller banks have more of the loans and the larger banks have more of the cash, which explains the recent weakness in some regional bank stocks.

In fact, in the last six months, the percentage of total assets that are high quality liquid assets has increased for large banks and decreased for smaller banks.4 However, many of the issues that have created stress for New York Community Bank are unique to that bank.

Some global banks have come under pressure

In the last week, concerns have spread outside the US. However, this again appears to be limited to a small group of banks that have substantial exposure to US commercial real estate — for which their stock prices may be getting unfairly punished. The European Central Bank is nevertheless on alert with regard to commercial real estate and has reportedly warned banks about managing commercial real estate risks and bolstering their capital.

Three key points about US commercial real estate

But what about US commercial real estate itself? There are three key points to keep in mind:

- US office utilization is slowly improving. The Kastle Back to Work Barometer, which measures return-to-office conditions in 10 major US cities, has shown a marked improvement in recent weeks. The current level is 53%, up from 48.5% for the week of Jan. 10.5 And while occupancy rates for non-office property types have softened for the industrial and apartment sectors to just below pre-COVID levels, they remain materially higher than occupancy rate troughs of the global financial crisis period. Also, US non-mall retail centre occupancy rates are at a two-decade high.6

- A large portion of US commercial real estate loans won’t come due and be ready to refinance until 2025 and beyond, It’s true that 2024 is a significant year for maturities — with 17% of all US commercial real estate loans coming due this year.7 However, that means the vast majority of commercial real estate loans won’t come due until later. In fact, 17% of commercial real estate loans come due in 2025, and 58% won’t come due until 2026 and beyond when US interest rates could be significantly lower than where they are now.7

- Yes, delinquencies in the office sector have increased; the US office delinquency rate rose 48 basis points to 6.30%.8 However, other areas of commercial real estate have actually fallen. For example, the industrial delinquency rate fell 17 basis points to 0.40%.8 And we must keep in mind that office is only one component of overall commercial real estate.

Bank problems appear contained

In short, we believe bank problems remain isolated, contained to a small portion of smaller banks. We could see issues arising for a few individual banks periodically as long as we remain in a higher interest rate environment, even if the sector is profitable and stable in aggregate. Also, our base case of a “bumpy landing” followed by a reacceleration of economic growth in the US could imply higher loan growth and an improving ability of borrowers to service debts. And the eventual start of easing in monetary policy could also support growth, while reducing the pressure in net interest margins, by reducing the need to increase deposit rates.

Perhaps the strongest signal that the overall market isn’t worried about commercial real estate is that the recent headlines didn’t stop the S&P 500 Index from closing above 5,000 for the first time ever on Feb. 9.9 You may recall that the S&P 500 only hit 2,500 in September 2017.10 Given all the challenges between then and now, it’s clear stocks really climbed a “wall of worry.”

This serves as a reminder of the importance of remaining invested (and well-diversified) for the long run, rather than getting unnerved by headlines. (And the S&P 500 wasn’t the only milestone last week. The Nikkei 225 benchmark index breached 37,000 intra-day for the first time in 34 years.11)

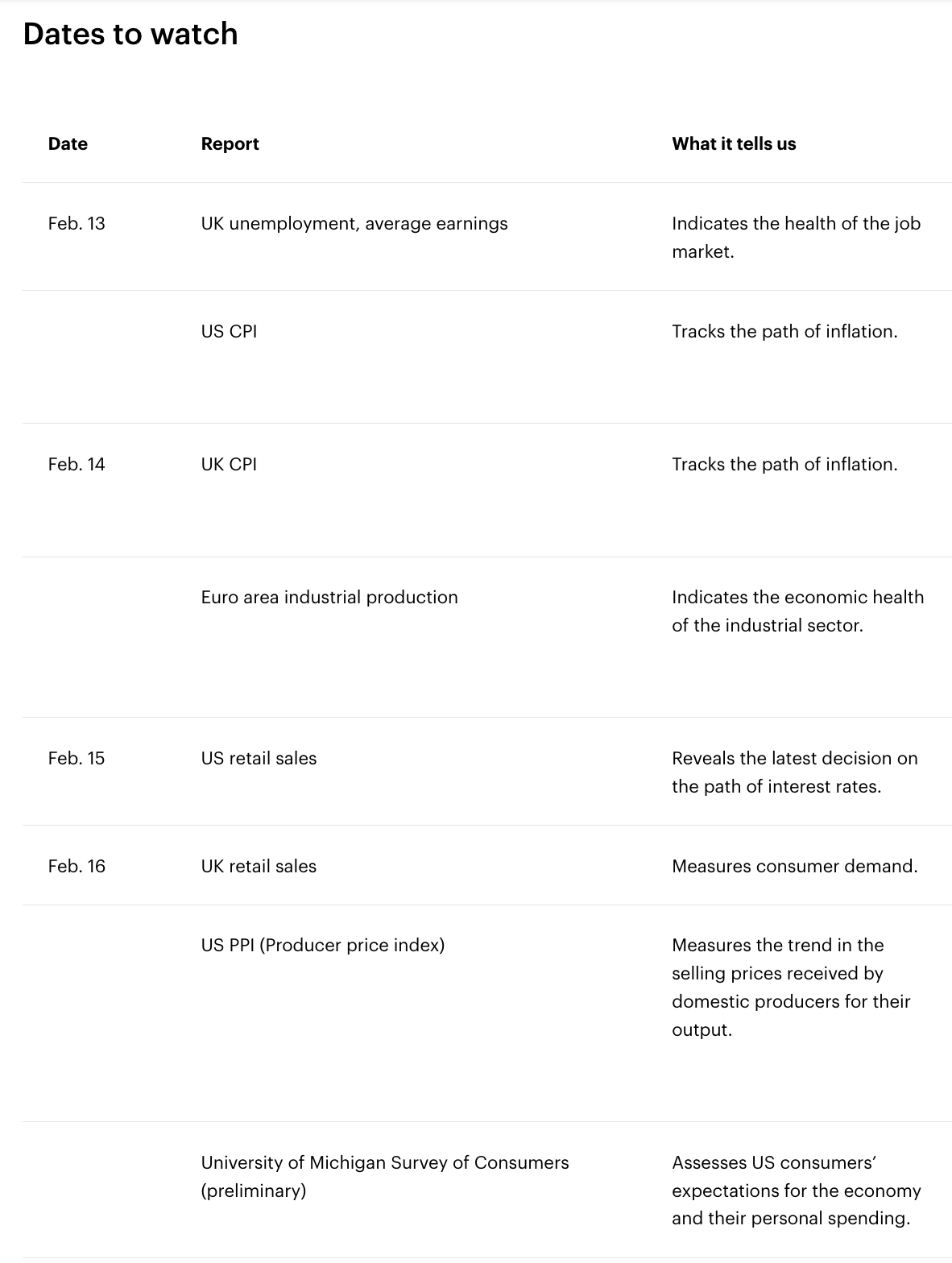

Dates to watch

Looking ahead, this week’s US Consumer Price Index print will be closely watched. The Fed is looking for more confirmation about the strong disinflationary trend; this print could help provide that confirmation — or not — and is likely to move markets.

With contributions from Andras Vig, Mike Sobolik, and Nicholas Buss

Explore what we expect from markets and the economy in 2024: Read our 2024 Investment Outlook and listen to our podcast.

And follow me on LinkedIn and X for more insights.

Footnotes

1 Source: United States Banks Index, Datastream, Dec. 31, 2023.

2 Source: Bloomberg, L.P., as of Feb. 9, 2024

3 Source: “Assets and liabilities of commercial banks in the United States,” Federal Reserve, Feb. 9, 2024.

4 Source: “Assets and liabilities of commercial banks in the United States,” Federal Reserve Bank of New York, as of Feb. 8, 2024.

5 Source: Kastle Back to Work Barometer, as of Feb. 25, 2024

6 Source: CBRE-EA, as of Dec. 31, 2023

7 Source: MSCI Real Assets, as of Sept. 26, 2023

8 Source: Trepp CMBS Research, February 2024

9 Source: “S&P 500 closes above key 5,000 level for first time,” CNN Business, Feb. 9, 2024

10 Source: Bloomberg, L.P., as of September 2017

11 Source: “Japan’s Nikkei hits fresh 34-year highs; most Asian markets are closed for Lunar New Year holiday,” CNBC, Feb. 9, 2024

Copyright © Invesco