by Carl Tannenbaum, Vaibhav Tandon, Ryan James Boyle, Northern Trust

The economics teams looks back at the most significant stories we covered during 2023.

Editor’s Note: In our last full issue of the year, we look back at the most significant stories we covered during 2023.

Ducking Punches

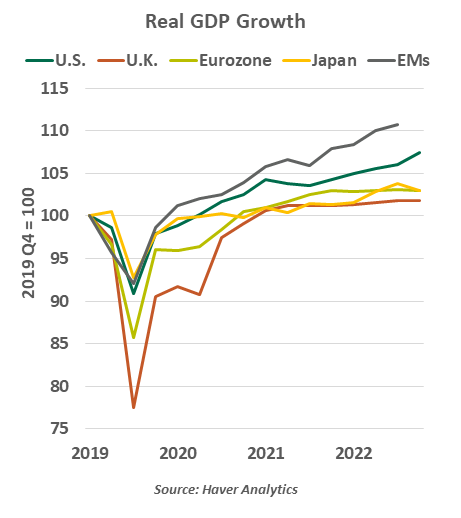

If we were to describe in one word the state of the global economy over the course of 2023, it would be “resilience.”

At the start of the year, a global recession felt assured. But despite aggressive interest rate increases, a banking crisis and adverse geopolitical developments, the global economic expansion has continued. The U.S. economy actually seemed to gain strength in the middle of the year; while European economies are more sluggish, the bloc has been able to avoid an outright recession. The Japanese economy grew robustly enough to end decades of deflation. Healthy consumer finances amid tight labor markets and excess pandemic savings have been the key supports in the developed world.

Emerging markets (EMs) have also displayed surprising resilience to the very challenges that have often proven detrimental to their economic health. Most EMs have been able to withstand higher energy and food costs, aggressive monetary policy tightening in developed countries and increasing supply chain realignment. The early response of emerging economy central banks to the threat of rising inflation, coupled with improved external and fiscal buffers, have prevented them from slipping into financial turmoil. China is struggling, but has thus far managed to limit spillovers from the real estate downturn to the broader financial sector.

The global economy has been weakened by a series of crises, so the dangers of a downturn have not passed. Growth is poised to slow as positive shocks fade, while tighter credit conditions bite. A soft landing is our base case, but the possibility of an unpleasant surprise in 2024 cannot be ruled out completely. If that surprise comes, the resilience seen this year should limit the damage.

What, Me Worry?

In his magnum opus Thinking, Fast and Slow, behavioral economist Daniel Kahneman described the two systems of thought. System 1 is fast and instinctive; System 2 is slower but more reasoned and logical. Both systems are valuable and are always working in parallel. But sometimes, the two do not come to the same conclusion.

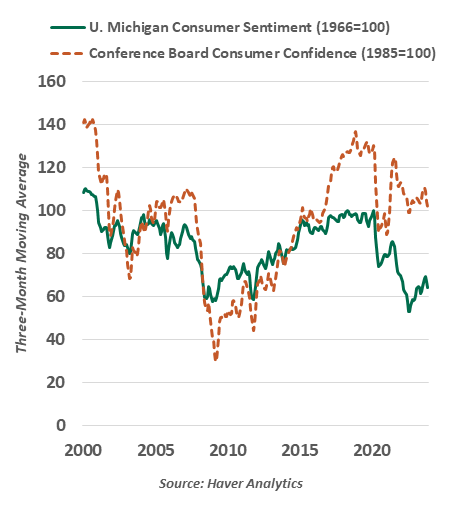

Our System 2 analysis of U.S. domestic economic data concludes that we are living in a thriving economy. But System 1 says something just isn't right. Why is the perception of the economy so much worse than reality?

Today's economic outcomes have surpassed expectations: strong growth, historically low unemployment and falling inflation. We have learned to live with COVID-19, supply chains have healed and wages are rising.

But reasons for gloom aren’t hard to find. While prices have stopped rising at the breakneck pace of 2022, most have not declined, either. Everything feels expensive relative to a pre-pandemic anchor; today's costs do not yet feel normal. While layoffs have been limited, those who lose jobs are having a harder time finding their next opportunity. First-time homebuyers and young parents (two overlapping categories) are reckoning with high costs and limited availability of both housing and childcare.

Opinion polls have been dour and deteriorating for much of the year. Across surveys, a preponderance of consumers rate the economy poorly. The University of Michigan's widely-cited Index of Consumer Sentiment has held at levels seen during the Global Financial Crisis: a prolonged interval of high unemployment, home foreclosures and wealth destruction. Today's circumstances do not compare empirically, but the national mood is similarly bleak. Opinion polling is often done in a political context, and dysfunction in Washington has offered no cause for cheer.

Behavioral economics offers both insight and hope. Kahneman contributed to Prospect Theory, the idea that most people are loss averse. Our pain from losses exceeds our satisfaction from gains. Wages are up, which is nice, but the burden of higher prices is felt more keenly. But Kahneman also concluded that humans are fundamentally confident and optimistic when approaching problems. We have been through worse times and persevered, and we will do so again. The economic recovery from the pandemic was fast; the psychological recovery is slow, but ongoing.

Settling Debts

Most nations regained their footing after the pandemic in relatively short order. Around the world, output and employment are at or beyond the levels they held in early 2020. Government support through the crisis played an important role in achieving these outcomes.

As 2023 concludes, fiscal policy is moving from tailwind to headwind. During 2023, the U.S. withdrew expanded Medicaid eligibility, broader access to nutritional assistance and the student loan payment moratorium. The U.K. ended government backstops of loans to support businesses through the pandemic, while a challenge to Germany’s pandemic fund allocation has caused a minor fiscal panic. The end of China’s zero-COVID policy has been a complicated story throughout the year, but the state is certainly not offering the same degree of support that it once did.

Though COVID-era programs are sunsetting, their impact on government balance sheets will be felt for years to come. Caution about spending was thrown to the wind throughout the crisis—and, some may argue, remained too generous after the worst had passed. The International Monetary Fund’s 2023 Global Debt Monitor found that half the pandemic surge in fiscal imbalances had retreated in 2022. But despite recent declines, global debt remains nine percentage points of gross domestic product (GDP) above its pre-pandemic level, and is on an upward trend.

Government obligations have grown in both quantity and cost. Markets across the world witnessed a run-up in sovereign bond yields this year. Nations running a deficit must roll over their maturing instruments, and every new bond is issued at a higher interest rate than the one it replaces.

Higher rates have only one upside: ensuring that government debt still finds buyers. Savers are enjoying high, risk-free returns, and they will be needed to maintain the flow of debt. Central banks funded much of the debt run-up; they are now winding down their holdings and limiting their reinvestments.

We do not look back on this spending with regret. COVID-19 had the potential to do permanent economic damage; large and decisive interventions prevented a great deal of worst-case outcomes. But the support was not free, and the costs will become clearer in the year ahead.

Roller Reversal

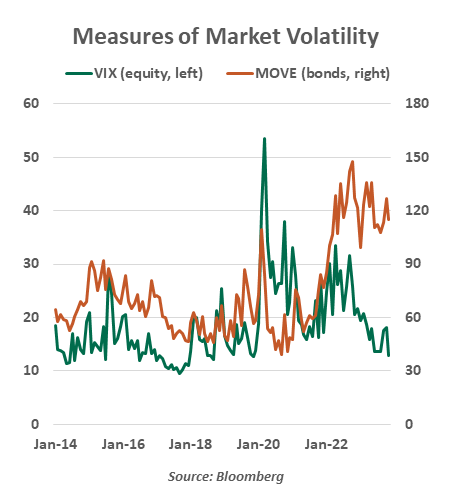

Stocks are typically thought to be among the riskier components of a portfolio. Over time, equity returns are better than other asset classes, but investors must be willing to endure some ups and downs along the way. Fixed income assets help to bring stability to a portfolio.

2023 will be viewed as an exception to that general rule. Stock returns in most major countries have been excellent this year, and stock market volatility receded. By contrast, bond markets experienced a roller coaster ride.

Uncertainty surrounding monetary policy has been the root cause of this development. Until summer’s end, speculation centered on when central banks would stop raising rates; since then, intense focus has been on when rates would begin receding. Expectations have gone back and forth and back again this year; long-term yields in major countries have traded in ranges that are more than 150 basis points wide.

Another factor has been increased anxiety over government borrowing. Increased costs to service debt have made budgeting more challenging, and an increasing degree of political polarization has complicated the conduct of fiscal policy in some regions. Investors have, at times, strained under the weight of the bond issuance they have been asked to absorb, adding further to the challenge of balancing demand and supply in debt markets.

As a result, implied volatility in the bond market has been much higher than volatility in the equity market since the beginning of last year. This condition could persist well into 2024. Budget stress is unlikely to recede; the United States could still experience a government shutdown early in the new year, and the euro area is still trying to settle on updated budget rules. Bond markets have been anxious to declare victory on inflation, only to be scolded by central banks for being too presumptuous. The tussle between the two is likely to persist.

And we have elections next year that will cover more than 40% of the world’s population. The twists and turns that may be on the horizon will require us to keep our seatbelts fastened.

From Hare to Tortoise

The lunar year that began last January was the year of the rabbit. That seemed an appropriate symbol for the Chinese economy, which was expected to outsprint its global rivals. Unfortunately, actual performance has been sluggish.

In many western countries, the post-pandemic reopening unleashed a powerful wave of economic energy. Consumers spent pent-up saving and indulged in “revenge travel.” Expansions gathered steam, despite rate hikes. Inflation concerns shifted from goods to services.

From the outset, China’s experience with COVID-19 was different. Isolation was rigidly enforced, disrupting lives and productive processes. Toward the end of 2022, the regime quietly recognized that its pandemic strategy was not as effective as it hoped. In short order, most restrictions on movement and congregation were relaxed, leading to a heavy wave of cases.

Chinese officials were hoping to put the pandemic into the past, paving the way for a reopening that would be powerful both commercially and societally. The global economy was counting on that outcome; the consensus outlook for 2023 called for recessions in the major western markets, while China was expected to carry growth forward.

Fortunately, developed markets outperformed expectations this year. China, by contrast, underwhelmed. As we covered in our View from China in May, the population emerged from COVID somewhat shell-shocked. The unfolding property crisis put a deep dent in both sentiment and household wealth.

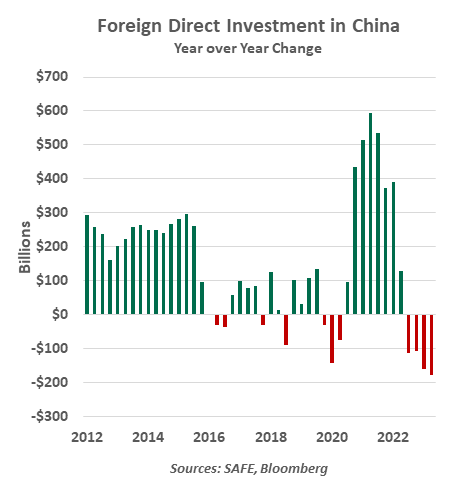

China’s exports struggled against the headwinds of de-globalization and reshoring. Deteriorating relations with the U.S. led to additional restrictions on technology transfers and raised risks for Western companies operating in China. Capital outflows from China have intensified: foreigners were first movers, but Chinese citizens have increasingly sought to transfer money out of the country. The Chinese currency has been under constant pressure this year, despite interventions that have depleted Chinese holdings of U.S. Treasury securities.

The outlook for China is modest, with significant down-side risks. Policy choices are challenging: deleveraging reduces the potency of rate cuts, and heavy government debts make major stimulus programs unlikely.

The next lunar new year is a year of the dragon, the most auspicious of all the zodiac signs. China is certainly hoping that this will foreshadow renewed good fortune.

Black Swans And Grey Rhinos

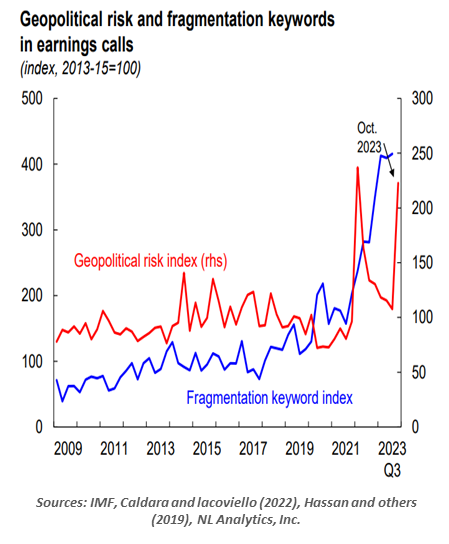

A supercycle is an extended period of economic expansion. But the concept is used to describe other periods of substantial advancement in fields such as regulation and astronomy. Unfortunately, the supercycle that was most prominent this year was the one surrounding geopolitical risks.

International conflicts are not a new phenomenon, but they are starting to have a more sizeable impact on markets and business decisions. War in Europe and the Middle East, as well as escalating tensions between China and the United States, are changing the playbook for economic relations and policy worldwide.

Uncertainty has advanced as globalization has retreated. The United States’ call for “friend-shoring,” the EU’s “de-risking” and China and India’s focus on “self-reliance” are fueling geopolitical rivalries. Technological decoupling, trade battles and capital dislocation have resulted. Globally, around 3,000 restrictive trade measures were put into place last year—nearly 3 times the number imposed in 2019. Manufacturing decisions are being guided by government policies more than efficiency considerations. Institutions like the International Monetary Fund and World Trade Organization are no longer as effective as they once were in mediating economic stress.

The emergence of the geopolitical risk supercycle runs counter to the long period of stability that allowed multilateralism to flourish amid greater integration. The current trend toward fragmentation is not only reducing global co-operation but also leading to the rise of more assertive nations.

Geopolitics are now featuring more often in company earnings’ calls and boardroom conversations. We’re seeing an increasing number of black swans (rare events that come as a surprise) and grey rhinos (rare events that occur after a series of warnings), hindering commerce and heightening risk aversion.

This is not the kind of supercycle that we would prefer. But policymakers, institutions and businesses will have to prepare for the risks that it presents.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions. © 2023 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.

Copyright © Northern Trust