by Lei Qiu, Portfolio Manager—Disruptive Innovation Equities, AllianceBernstein

Technological turning points in the past have taught important lessons about how to identify long-term winners from transformative innovation.

The market reaction to generative artificial intelligence (GAI) over the past year implies that investors already know how this revolution will play out. But not so fast. While we may be on the cusp of a dramatic technology paradigm shift, its outcomes are far from obvious and will take time to discern.

For much of 2023, US equity markets were defined by excitement over AI. Returns were concentrated in a very small group of stocks seen to be AI winners. The market appears to be assigning a high probability to the assumption that these companies will be the long-term leaders of the AI revolution with the greatest profitability gains. Wall Street analysts are already projecting how much revenue and profit the incumbents will see from AI. There’s a frenzy of forecasts for how many initial users Microsoft will attract for Copilot, its GAI tool expected in November. Some even predict the end of internet search as we know it.

The Race Is on for the GAI Operating System

We think it’s too early to make such bold predictions—particularly on profitability. Yes, GAI marks a paradigm shift with the potential to deliver massive productivity gains by lowering barriers to entry and stimulating new business models. Yet during technological turning points in the past, investors also learned important lessons about evaluating the true long-term impact of transformational innovation.

Today, the spotlight is on the technology mega-caps. Each wants to build their own unique large language model that will become the future GAI operating system. In aggregate, the spending on AI-dedicated graphics processing units (GPUs) will reach at least $25 billion in 2023 alone. Disruptive innovation creates a window of opportunity for the incumbents to enter each other’s playing field.

Lessons from the iPhone and Internet

But will all the mega-caps be the biggest long-term AI winners? And more importantly, how can investors determine which companies have the right business models to profit in an AI future?

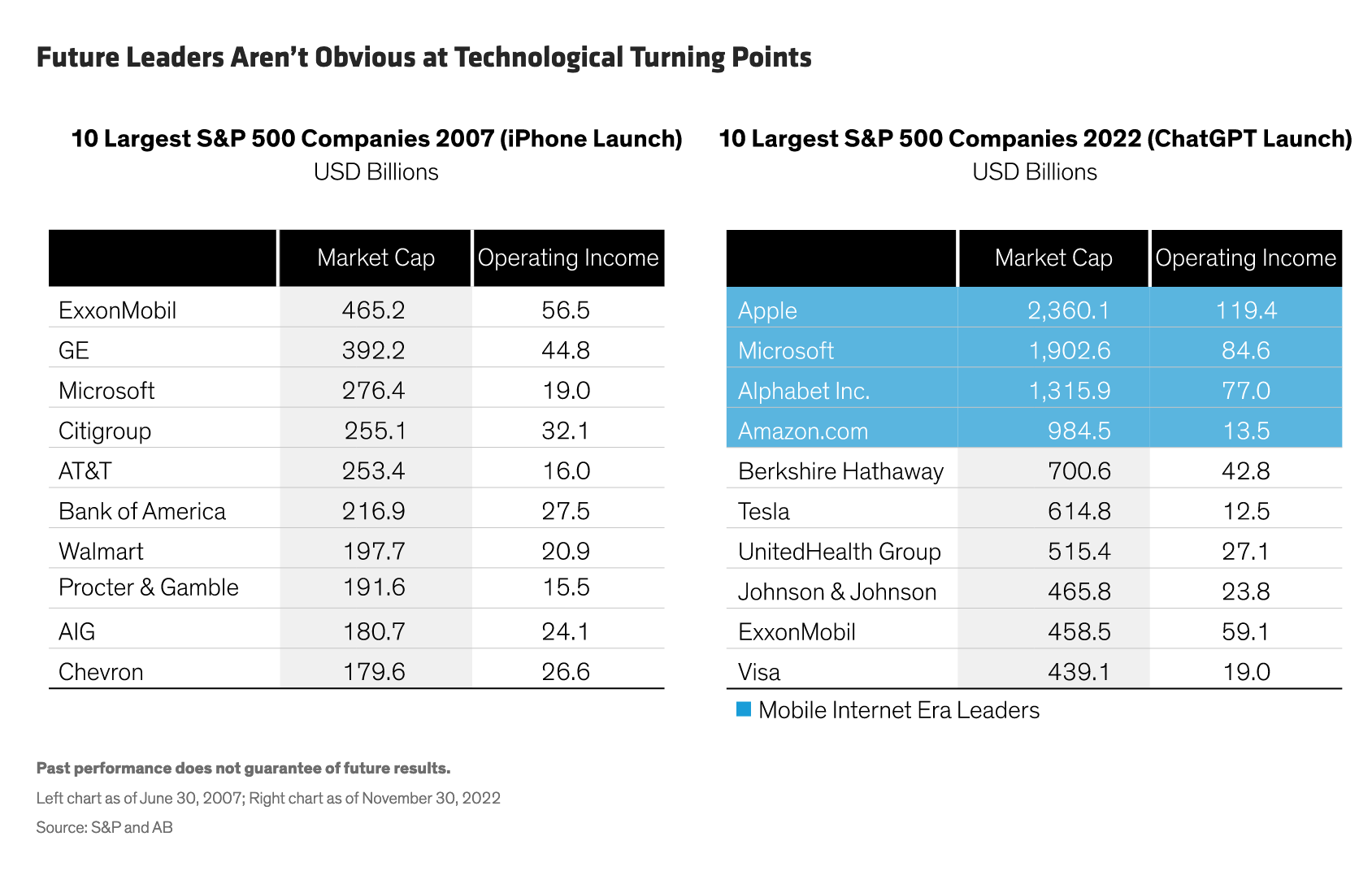

Some historical context can help answer these questions. AI itself isn’t new, but GAI, which took the world by storm in November 2022 with ChatGPT, has been dubbed an iPhone moment for innovation. The iPhone combined the internet, mobile broadband and smartphone in a single package that unlocked access to vast amounts of information and created efficiencies across industries.

Yet when the iPhone was launched in 2007, the long-term winners and losers weren’t immediately apparent. In fact, the largest companies—by market cap and by operating profit—were very different in 2007 than they are today. Over time, new leaders emerged with much larger profit pools. Some, like Apple, may have been more obvious. But the smartphone spawned a whole new mobile ecosystem. Only then did household names including Meta, Spotify, YouTube and Venmo really began to take off (Display). In our view, the iPhone moment has yet to arrive for AI.

Capital Intensity Needed for AI Infrastructure

However, we’re already seeing a big change from the mobile internet era, when investors valued capital-light business models that supported the tech giants’ profitability. Now, GAI’s compute-intensity training and inferencing infrastructure requires massive investment in data centers and power systems. This could shake up the investing calculus for future profits—particularly in a world where capital is scarce and expensive.

To produce a single unit of output in an AI-focused data center, thousands of GPUs interconnect and behave as one, much like the highly automated production lines at Tesla’s gigafactories. At this stage of the AI revolution—the infrastructure build-out—innovation has shifted from customer-facing industries to capital-intensive manufacturing and development.

But these are early days for the AI revolution, and big spending doesn’t necessarily guarantee big profits. At the dawn of the internet, telecom and cable providers poured billions of dollars into web infrastructure. Yet it was the emerging tech titans that rode on those rails by creating new business models that captured most of the upside (Display).

Market Landscape Is Poised to Change

The mobile internet was a classic example of how a shifting technology paradigm changed the market landscape. The winners weren’t only dominant companies with a first-mover advantage. While some of today’s mega-caps may indeed consolidate their positions through AI, we believe new leaders will emerge and the largest benchmark names will change over time as we saw in the mobile internet era (Display).

Finding future leaders isn’t easy. Investors often anchor their outlooks to what has worked in the past and is working in the present, while overlooking the transformational potential of innovators. Consider Amazon.com, which was seen in its early days as an expensive bookseller and evolved into an e-tailer. Back then, investors couldn’t imagine the company would transform itself into a logistics provider for vast commercial networks with a cloud-based infrastructure. Over time, Amazon’s market cap surpassed all US retailers combined because it disrupted the entire industry and gobbled up their profits, while creating a whole new business called Amazon Web Services.

Disruption will also destabilize some companies. If GAI is as powerful as we expect, we will have yet another iPhone moment that redefines productivity and behavior. New business models will emerge that will challenge the status quo in many industries. But in our view, we aren’t there yet.

Identifying Innovation Requires Imagination—and Patience

Innovation is about the power of imagination. Instead of rushing to the presumed winners at this early stage, investors must be patient and open minded.

Focusing on near-term profitability may be misleading. Equity investors should conduct prudent analysis of returns on capital and develop an informed outlook on future returns. In other words, companies shouldn’t necessarily be penalized for spending on AI to bolster competitive moats or to create growth opportunities. Yet they shouldn’t be automatically rewarded based on their level of capital spending alone. Companies must also be scrutinized to ensure that their current competitive moats aren’t threatened by new AI applications.

AI winners might not be the first companies to monetize the new technology. If GAI knocks down entry barriers in different industries, new players will emerge. Thematically oriented active investors with a long-term horizon should search beyond the tech giants to pinpoint companies with truly distinctive business models and competitive advantages that are poised to benefit from the AI disruption at our doorstep.