by Carl Tannenbaum, Chief Economist, Northern Trust

The potency of monetary policy will weigh more heavily on activity in 2024.

I learned an important life lesson during a canoe trip through Canada as a teenager. Periodically, our group of voyageurs would have to execute a portage: taking our vessels and gear overland from one body of water to another. Those days weren’t a lot of fun: you had to place your pack and a 100 pound canoe on your shoulders, and then march for a mile or two. Upon finishing the journey, you were expected to double back to carry tents and provisions.

Being the calculating person that I am, I realized that if I took my time carrying the canoe, others would return for the tents, saving me a second trip. Unfortunately, my counselors and fellow campers had little patience for my slow-play. “If you’re a laggard, you will never be a leader!” I was told. I’ve never forgotten that advice.

In my profession, it is very important to distinguish laggards from leaders. Some indicators are the result of economic change, while others presage it. Some policy moves have an instant impact, while others take time to reach full effect.

Central bank strategy falls into the latter category. The famed economist Milton Friedman observed that monetary policy “works with long and variable lags.” Understanding the delay between action and reaction will be critical to sticking the soft landing in 2024.

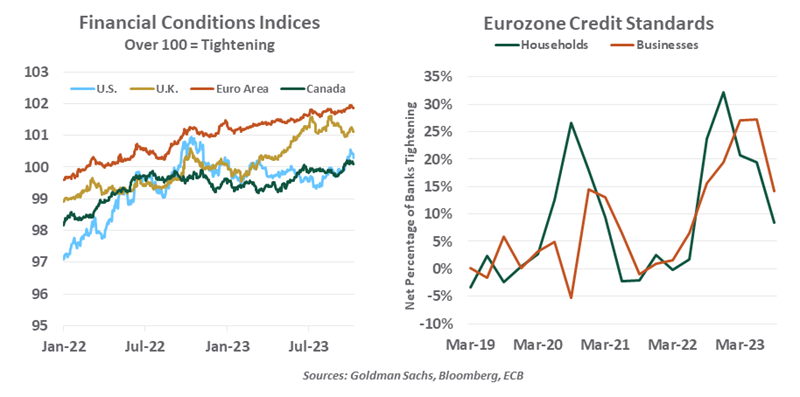

Two factors have a heavy influence on the timelines associated with monetary policy. The first of these is the state of financial conditions, which gauge how easy is it to access capital, and its cost. Central banks only have indirect influence on these elements.

For decades, financial conditions were determined almost exclusively by bank lending practices. Banks provided almost all of the credit used by households and businesses, so their standards and pricing had a material influence on economic activity. It took time for financial institutions to adjust their rates and terms to what central banks were doing; competitors would sometimes hold loan rates lower for longer, blunting the intent of policy.

In the modern era, financial markets play a much larger role in allocating capital. Credit is commonly accessed directly from investors, through their purchases of corporate bonds and securities backed by consumer loans. Firms can also raise commercial paper to meet their short-term needs for cash and equity to support long-term growth.

Bond and equity prices react quickly to monetary policy changes and interactively absorb guidance provided by central bank officials. But that doesn’t necessarily mean that monetary policy lags are shorter. Asset prices respond to a range of influences; as investor demand intersects with supply, financial conditions can sometimes move in a manner opposed to what the central bank intended. Indeed, measures of financial conditions in the United States today are still not that tight, in spite of the most rapid interest rate increases in forty years.

American bank lending standards are very restrictive, in spite of strong economic performance and healthy household and corporate balance sheets. Bank deposits have declined this year, thanks to the combination of a falling money supply, rising interest rates and concern generated by the bank failures of early 2023. With reduced liquidity, banks have curtailed their appetites for lending. A rising tide of new regulations is adding to the conservatism.

The opposite has been true outside of the banking sector. Private capital pools have expanded their activities, and capital markets have remained receptive to new issues. Equity markets have gained, and corporate bond spreads have remained narrow.

As a result, U.S. financial conditions are relatively neutral. In Europe, where banks still provide about 80% of the financing used in the economy, financial conditions have tightened significantly this year. This variance is one of the reasons why growth in the United States has exceeded growth in the U.K. and the euro area.

The second factor that bears on the timing of monetary policy transmission is the reliance the economy has on borrowing. The pandemic produced significant changes on this front.

COVID-era support programs allowed households to reduce debt and accumulate excess saving. Under these conditions, higher interest rates increase the income earned by savers, adding support for spending. Recently, however, the use of consumer credit has exceeded pre-pandemic levels. Default risks are not a major concern, but the debt servicing costs paid by households will curtail consumption in the months ahead.

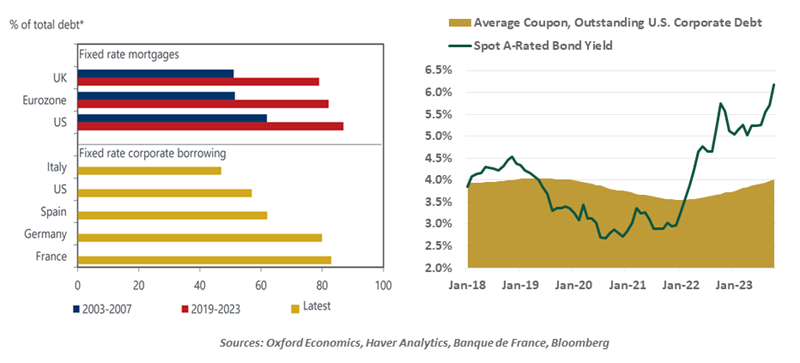

In addition, the very low interest rates that prevailed in 2020 and 2021 allowed households and firms to insulate themselves against prospective interest rate increases by locking in long-term debt at favorable terms. Homeowners extended their loans for as long as possible: up to five years in Great Britain and up to 30 years in the United States.

Corporations also took the opportunity to lock in low rates in 2020 and 2021, and have managed their cash positions so that they don’t have to re-enter the market anytime soon. While spot rates on corporate debt have risen sharply this year, debt service costs have barely budged. The need to roll over those borrowings won’t become substantial for at least another year.

In sum, the liquidity poured into economies by central banks three years ago reduced the need to borrow and increased investor demand for assets. The combination of these forces has extended the lags involved with monetary policy.

That said, economies have not become immune to high interest rates. The potency of policy will weigh more heavily on activity in 2024, prompting central banks to hold off on further interest rate increases. If activity sags, monetary policy will have to release the brakes.

After being admonished for my lack of industry during our canoe trips, I made it a point to make extra trips during the next portage. I restored my reputation, but nearly collapsed from exhaustion. Canoersand economies can bear burdens for only so long before requiring ease.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions. © 2023 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.

Carl R. Tannenbaum

Executive Vice President and Chief Economist

Carl Tannenbaum is the Chief Economist for Northern Trust. In this role, he briefs clients and colleagues on the economy and business conditions, prepares the bank's official economic outlook and participates in forecast surveys. He is a member of Northern Trust's investment policy committee, its capital committee, and its asset/liability management committee.