by Russ Koesterich, CFA, JD, Portfolio Manager, BlackRock

Key takeaways:

- The late summer equity market selloff was driven by a melt-up in real (“inflation adjusted”) rates.

- While the relationship between stocks and bonds has varied over time, it becomes more significant when rates jump.

- Albeit painful, the silver lining to the recent spike in yields is that the Fed may now be less motivated to hike again, which could stabilize bond markets and support stocks through year-end.

While it appears that the typical fall performance swoon may have passed, the stock market is still nervously looking over its shoulder at the bond market. The S&P 500 fell more than 8% from its July peak. More volatile parts of the market, notably small and emerging market stocks, where down 10 to 15%.

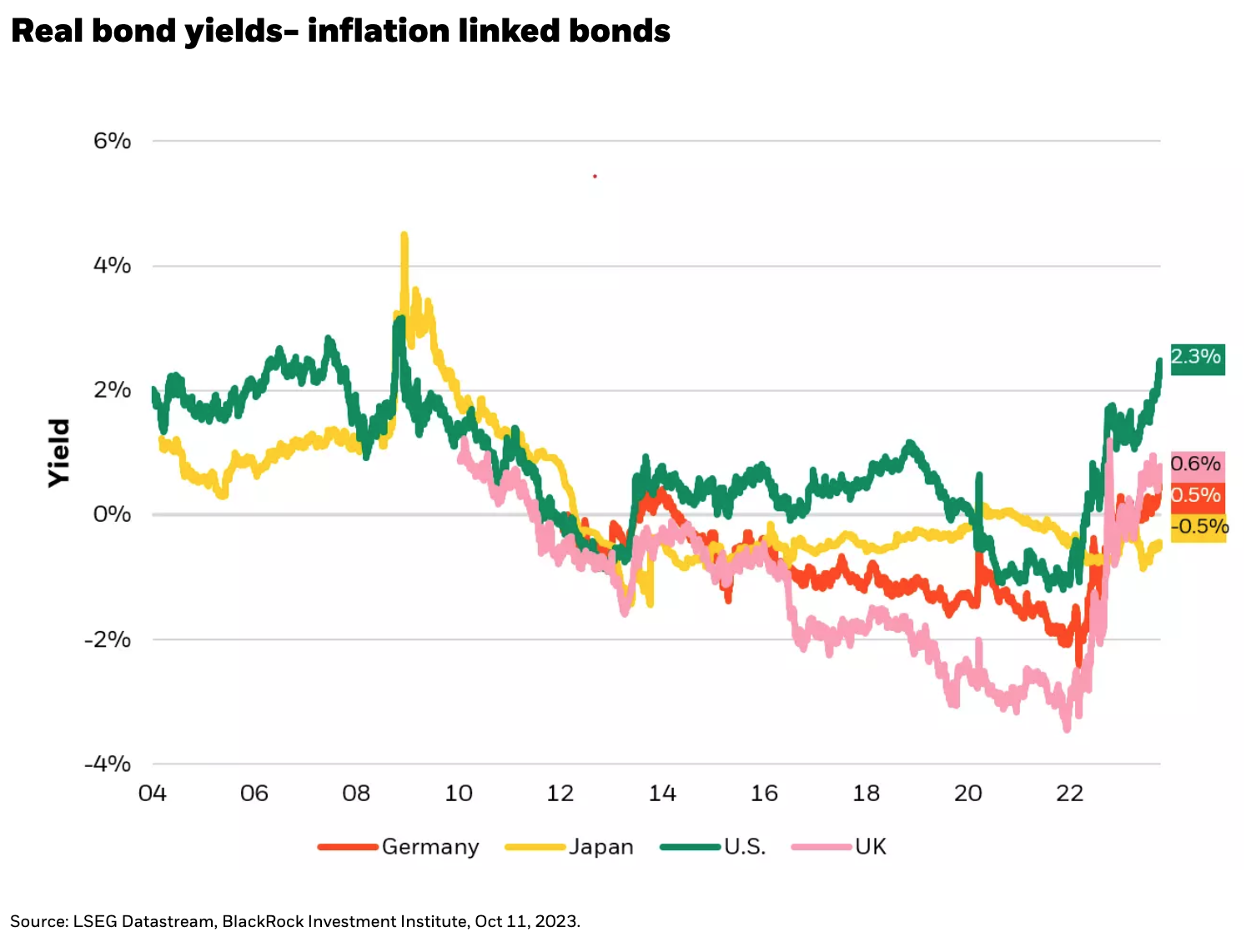

While a late summer sell-off is a common seasonal occurrence in equity markets, this was a particularly large one given the momentum going into August. The key catalyst this year was a melt-up in bond yields, driven by an increase in real or inflation adjusted rates. From the July low through the October high, U.S. 10-year real yields, derived from the TIPS market, rose roughly 1.2% to more than 2.3%, the highest level in 15 years (see Chart 1).

It's Complicated

The textbook relationship between stocks and bonds is one where a higher discount rate leads to lower stock valuations. That said, when looking at historical data, it’s clear the relationship is more complicated. Going back to the late 1990’s, higher real rates are associated with weaker stock returns, but the relationship is not particularly strong.

This is not as surprising as it seems. No single factor explains a significant portion of stock returns. And in the case of bond yields, there are circumstances when real rates and stocks rise together. When the economy is emerging from a recession, investors typically upgrade their estimates for both economic and earnings growth. During these periods, such as late 2020, it is not uncommon for both stocks and real rates to move in tandem.

However, while the relationship is not particularly strong for small moves, it becomes more significant when rates jump. In periods when real rates spike, defined here as a monthly move of 20 bps or more, the average S&P 500 monthly return is nearly -1%. Returns become even worse during months like September, when real yields rose roughly 40 bps. In the past, moves of this magnitude have seen average market returns of -4.5%.

Spiking Yields, Tighter Financial Conditions

Given this dynamic, to some extent stocks remain hostage to big moves in the bond market. If you view a further melt up in real rates as likely, it may be best to remain light on equities as there is arguably more pain ahead. However, I would view this outcome as less likely as the spike in bond yields arguably did some of the Federal Reserve’s work for them.

Higher real rates have historically tightened financial conditions and act as a drag on growth. While the impact is not immediate, higher real rates will help the Fed in slowing the economy and inflation. This suggests that while sticky inflation still makes a near-term rate cut unlikely, the Fed may now be less motivated to hike again, as they seem to be implicitly acknowledging in their recent public comments. If this in turn helps stabilize bond markets and real rates, stocks may still get to enjoy their typical Q4 rally.